THE HEDGEYE EDGE

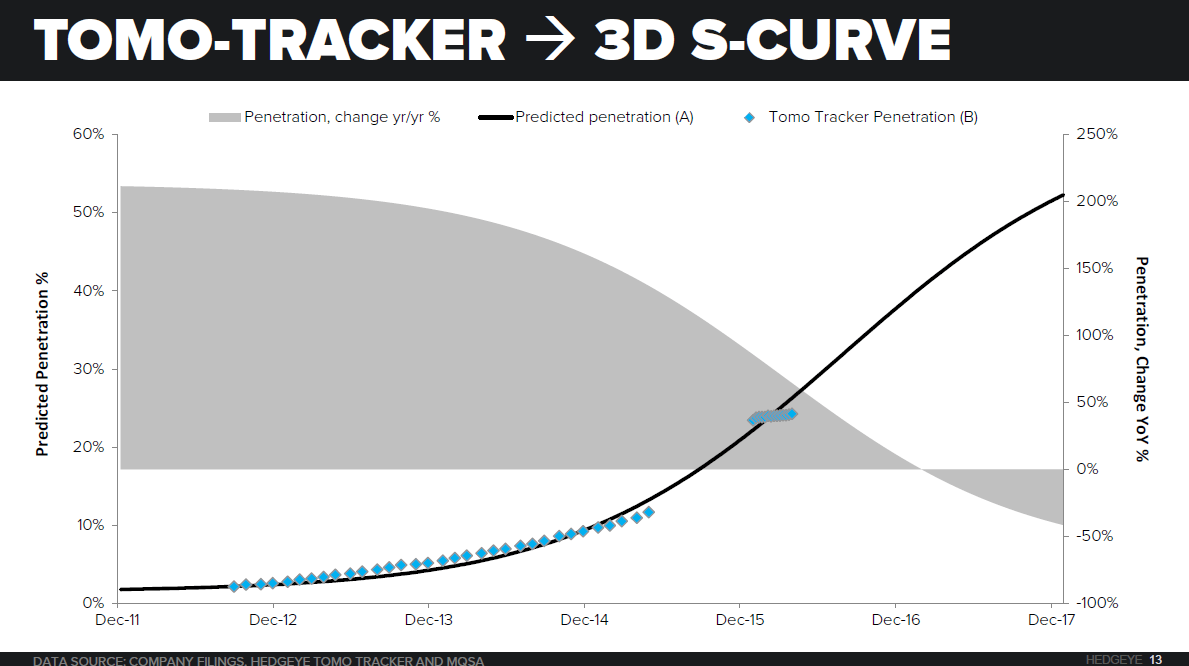

We have a long history with Hologic (HOLX). Our first major call on the stock was being long and “looking for a double” in April 2014 when the stock was in the low-$20s. At that time, our proprietary dataset that tracks the number of U.S. Facilities with a Hologic 3D Tomography machine and S-Curve adoption forecast model suggested a large acceleration in growth through 2015.

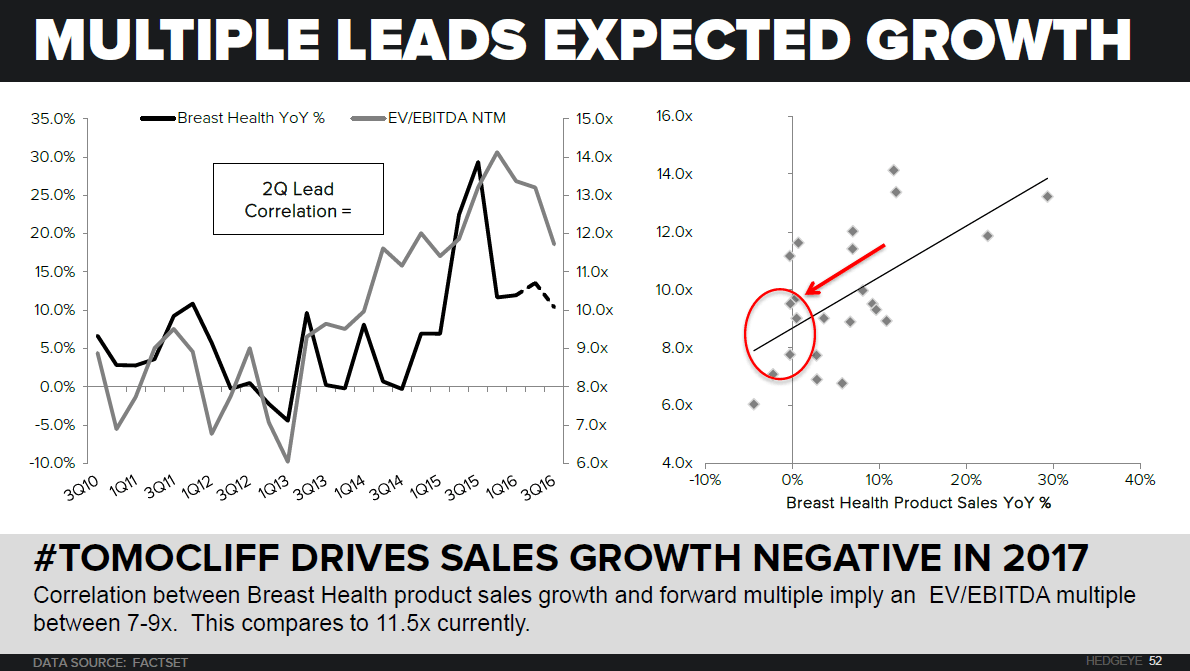

While there are other elements of Hologic’s business, historical regression analysis shows that forward multiple is most dependent on the growth rate in the Breast Health (42% of sales) business or 3D Tomography sales. Simply put, get Breast Health growth right and get the stock right.

Fortunately, our initial long calls was correct, but now we are on the other side and the same forecast methodology suggests growth has peaked, and new facility placements will likely turn negative into 2H17.

We will continue to provide updates to our proprietary #TOMOTRACKER that will inform us where we are on the adoption curve and act as a benchmark to test our thesis against.

INTERMEDIATE TERM (TREND)

Over the intermediate term, we see little that can drive further upside to the stock, outside of an acquisition (which is a risk to our thesis). While we expect growth to continue to come under pressure, our call for -30% downside is likely to play out over the next 12-18 months.

There are two key drivers that we expect will drive shares of Hologic (HOLX) back into the low-$20s.

1. Slowing 3D Tomo Adoption – Hologic stopped disclosing penetration for 3D mammography, providing the last unit counts and market share in September 2015. For the September 2015 period, the company disclosed 28% penetration into their installed base. Our s-curve for 3D indicates share was 32.4% as of 9/27/2015, which agrees with HOLX management statements.

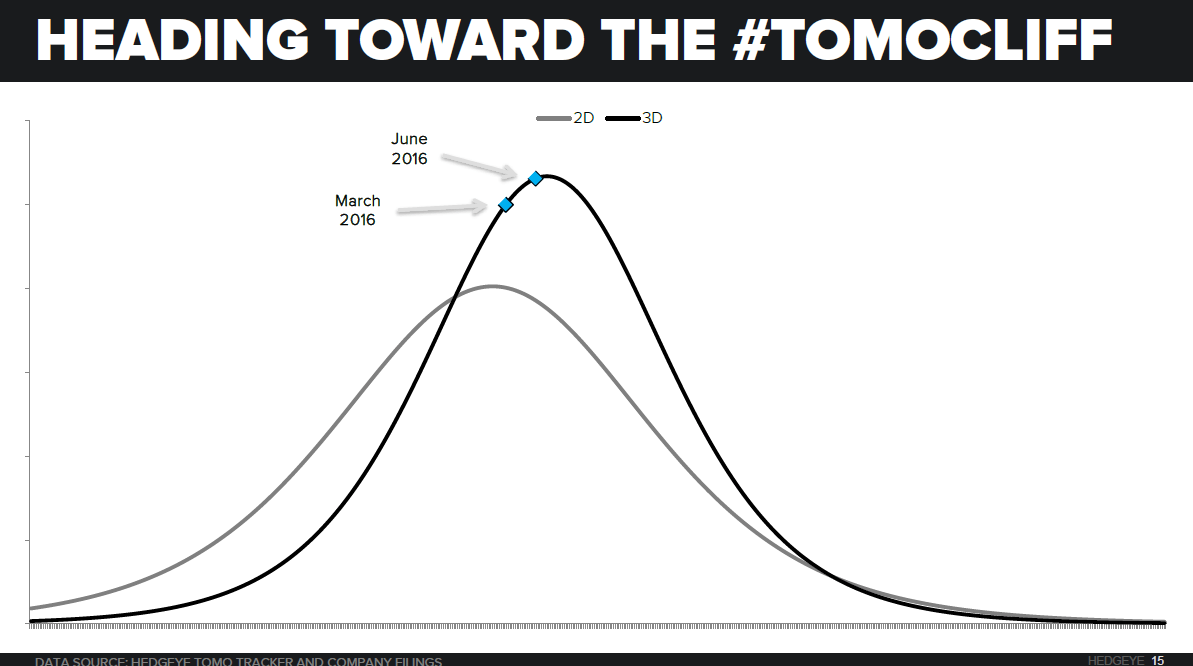

However, based on our Tomo Tracker data, we believe HOLX has added to their 3D installed base and now sits at 40%. While the rapid pace of 3D conversion led to upside relative to consensus estimates and company guidance for much of 2014 and 2015, we expect facility conversion to turn negative now that we have passed 40%. The arithmetic of s-curves is straight forward and has precedent in the 2D adoption curve.

It is also worth noting that the gross margin on the 3D system is materially higher (65-70%) than the 2D system (50%) and the corporate average, which prior to the 3D ramp averaged around 52%. Accelerated adoption of 3D systems has driven corporate gross margin up an impressive 1,000 bps to 60% in 2Q16. As 3D growth slows, and eventually goes negative, we expect to see the opposite effect take hold.

2. #ACATaper – While more difficult to quantify, we believe the Affordable Care Act was a tailwind to HOLX’s diagnostic business. After years of being uninsured, new enrollees were top consumers of diagnostic tests that Hologic offers, such as HPV and PAP. This segment had been in decline prior to 2014, as a result of lengthening of the recommended interval for PAP testing, but reverted back to mid-single digit growth just as the newly insured under ACA hit the market. We are looking to several data series to track the utilization impact of the ACA, including Healthcare Employment Job Openings (JOLTS), which we will update on a monthly basis.

LONG TERM (TAIL)

We expect most of our downside to be realized over a 12-18 month time period, as the gap between our Breast Health estimates and consensus widens over the course of 2017. Specifically, consensus is calling for mid-single digit Breast Health growth in 2H17 compared to our estimate for mid-to-high single digit declines. Based on the correlation with Breast Health Product Sales growth and our forecast, we can comfortably model a return back to 6-8x EV/EBITDA multiple and a stock in the low-$20s (~12x EV/EBITDA Currently).

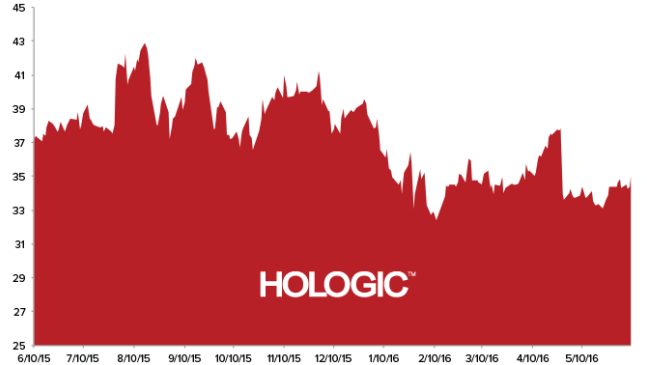

ONE-YEAR TRAILING CHART