Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added Dunkin' Brands (DNKN) to the short side of Investing Ideas this week. Restaurants analyst Howard Penney will send out a full stock report on DNKN next week. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here and here for Gold.

It was an excellent week for our Macro team's #GrowthSlowing call. Long Bonds (TLT) led the charge up +6.4% with Gold (GLD) up +2.4% versus a flat week for the S&P 500.

No matter what side of the reflation/deflation trade you’re on, the growth in global demand continues to decelerate on a trending basis. The debate is no longer whether or not growth is slowing. The real debate centers on the policy response and the market reaction to that policy response. While that question presents us with “open the envelope” risk, #GrowthSlowing will continue to be the bull catalyst for U.S. Treasuries whatever the policy response as the slow march to zero yields globally goes on. Remember:

Central planners can’t print growth.

Only 35% of country and regional PMI figures across manufacturing, services and composite readings are both expanding (i.e. > 50) and accelerating sequentially as of last month. The rest are either expanding but decelerating or in outright contraction (i.e. < 50). The JPMorgan Global Composite PMI Index in the chart below is a good birds-eye-view on the deceleration in broad-base PMI measures:

Hitting the demand slowdown on the consumption side of the domestic economy, we highly suggest watching the clip below from earlier this week. Macro analyst Christian Drake breaks down credit’s role in the consumption cycle when consumer spending starts to slow. Credit has the ability to pull forward spending, but when it too begins to roll, 69% of the economy starts tumble downward:

Click the image below to watch.

With the aforementioned evidence of continued economic contraction, we’re confident sticking with growth-slowing allocations (TLT) while waiting and watching on deflation/reflation exposure. As Keith McCullough outlined in Thursday’s Early Look:

“It was an easier call to make that growth would slow than it was that being right on #GrowthSlowing would get people to chase Reflation Charts that have been blowing investors up for 3 years. I don’t think of this as a mistake yet (this “bull” only started in MAR/APR). I’m actually thinking of it as an opportunity. While I haven’t been short Energy this year (we were last year with our #StrongDollar Deflation call), I haven’t been long it either.”

To sum things up, stay away from the guessing game and stick to what is empirically evident. A stronger USD over the longer term is a probable scenario in our book. We expect the Fed, and all central banks for that matter, will try to combat deflation. That said, global currencies all burning at the same time makes a compelling case for GLD, as gold knows no currency. You can sell it in local currency all over the world. Scary but true.

MCD

To view our analyst's original report on McDonald's click here.

There have been rumblings in the news that McDonald's (MCD) 2Q comps have slowed due to the temporary replacement of the 2 for $5 value platform for Monopoly. This has clearly been reflected in the stock as of late, as MCD has underperformed the S&P 500 over the last month.

Despite this near term headwind, we still strongly believe in the long-term story for MCD and remain confident that once they get their value platform right nationally, they will be just fine. In the short to intermediate term, as we wait for a solidified value platform, this recent underperformance represents a great buying opportunity. We remain LONG MCD.

WAB

To view our analyst's original report on Wabtec click here.

No update on Wabtech (WAB) this week but Hedgeye Industrials analyst Jay Van Sciver reiterates his short call.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is an update on ZBH from Healthcare analyst Tom Tobin.

We got the latest update to our #ACATaper thesis this week with the JOLTS report. Despite a slight sequential uptick in the absolute number of Healthcare Job Openings (1,015 April / 957 March), on a trending basis, growth was the slowest in 7 quarters with the 3-month YoY growth rate at +12.2%. JOLTS as a % of Healthcare Employment remains extended at +2.1 standard deviations, suggesting there is a lot more downside to go as the #ACATaper takes hold and the U.S. Medical Economy mean reverts.

Of the thousands of macro and fundamental data series we track on a daily basis, Healthcare Job Openings (JOLTS), prove to have the most consistent and reliable relationship to utilization trends in the industry.

We think the ACA increased volume temporarily in 2014 and 2015 for a host of Healthcare companies including hospitals, physician offices and orthopedic manufacturers. As we enter the late part of the economic cycle broadly and the inflated Healthcare caused by the ACA, we think Zimmer Biomet (ZBH) and its peers will be struggling with declining volume and increasing price pressure.

The chart below shows pent-up demand for Knee Replacement Surgery among newly insured from a Society of Actuaries Analysis of claims data in Kansas.

Quick Thoughts on LDR Acquisition

Earlier this week, Zimmer-Biomet announced the purchase of LDR (LDRH) for a total consideration of ~$1.0 billion, or 5.5x 2016 Sales. The transaction will be indirectly funded through issuance of $750 million of unsecured bonds expected to be priced and issued in 2H16. The LDR deal increases ZBH's market share in spine from 5% to 7%, but it will remain well behind competitors Medtronic at 31% and DePuy at 16%.

Spine is more favorably disposed from a demographic and payer mix perspective, but is also likely the next target for bundled payments. While ZBH needed to improve their Spine portfolio, we were surprised by the timing of the announcement so soon after closing Biomet and taking on ~$10 billion in debt to fund the deal. We also have a hard time understanding how the LDR is going to be neutral/accretive to earnings in 2017/2018 given the high price tag and management having no intention of reducing forecasted levels of investment.

HBI

To view our analyst's original report on Hanesbrands click here.

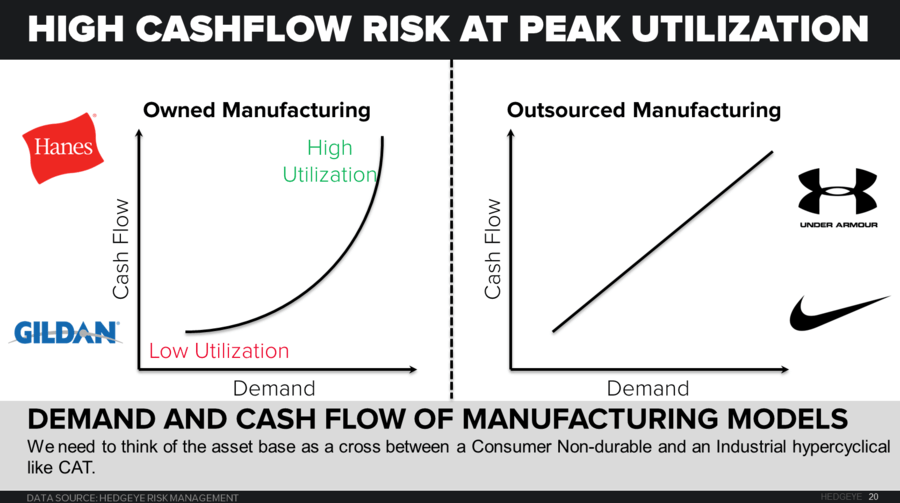

One piece of the Hanesbrands (HBI) business model that is commonly misunderstood is how utilization impacts their margins, since they own about 2/3 of their own production. The chart below outlines the difference between owned manufacturing and outsourced manufacturing. The graph on the right shows your typical apparel/footwear company set-up, where goods are made by a third party. For every unit of demand, the increase in cash flow or profits is the same.

However, with owned manufacturing each incremental unit of demand comes with accelerated profits and cash flow because it can scale up units and leverage the fixed manufacturing costs. Right now HBI is operating at over 90% utilization, and therefore has peak profitability per demand unit.

The problem now is that the leverage works both ways, so as demand drops, profits and cash flow decline at an accelerating rate. We believe demand is slowing and will continue to slow driven both by competition and macro factors. As this happens utilization will drop and margin and cash flow will decline rapidly. On that note, organic growth has been negative for 3 of the last 4 quarters.

NUS

To view our analyst's original report on Nu Skin click here.

No update on Nu Skin (NUS) this week but Hedgeye Consumer Staples analysts Howard Penney and Shayne Laidlaw reiterate their short call.

MDRX

To view our analyst's original report on Allscripts click here. Below is an excerpt from an institional research note on Allscripts (MDRX) written by our Healthcare team.

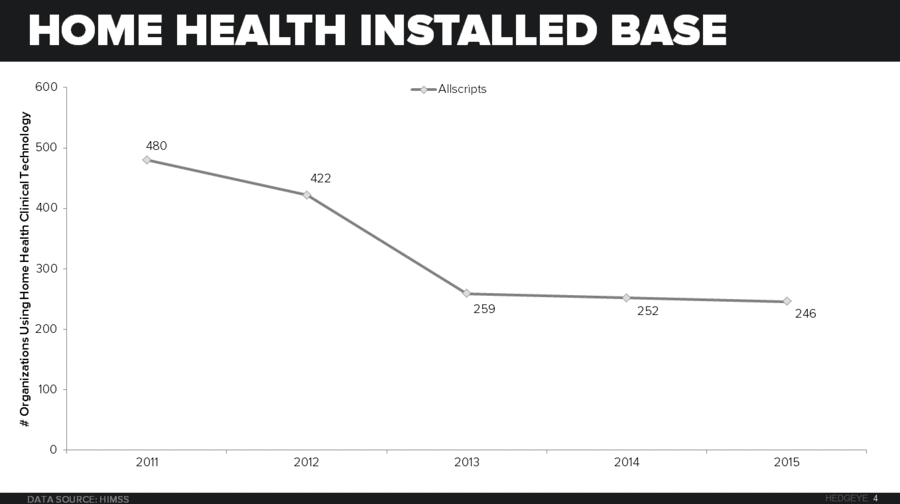

MDRX | HOME HEALTH BUSINESS

Takeaway: Allscripts did not invest resources into the Homecare product, which was old to begin with and resulted in competitive losses.

overview

We spoke with a former Allscripts Homecare Salesperson, who also spent many years working for Eclipsys as a Sunrise Rep prior to the merger. The purpose was to get a better understanding of Allscripts position in the Home Health market and rationale behind the Netsmart deal. Given chronic underinvestment and weak market prospects, we can see how the divestiture makes sense from a P&L perspective for core Allscripts. However, anecdotes suggest that current clients were not pleased with the news and we have a hard time grasping (absent additional investment) how the Homecare business is going to do much better under Netsmart's control.

"Last shoe has dropped and Netsmart has run away with the dish and the spoon... any sense of stability is now gone." - Large Allscripts Home Health Client

key takeaways

- Allscripts did not invest resources into the Homecare product, which was old to begin with and resulted in competitive losses.

- Homecare Homebase entered the market 5-years ago and began to take share from legacy vendors, especially Allscripts whose market share shrank from 13% in 2011 to 7% in 2015.

- Allscripts is currently doing whatever it takes to win new Sunrise business... Cutting maintenance from 18-20% of system sale to 8-10%, maintenance holidays, excluding or limiting CPI adjustment.

- Operational focus under Paul Black's leadership has come at the cost of product development and the sales organization.

TIF

To view our analyst's original report on Tiffany click here.

We're nearly to the end of retail earnings season and it appears that Tiffany (TIF) will post the 2nd worst comparable store sales gain in all of retail at -9%. The only worse comp we have seen is Lumber Liquidators, which is still feeling the hangover from national news stories noting its product is full of carcinogenic Formaldehyde.

We find it hard to believe that Tiffany is trading at 17x earnings considering the following factors:

- It put up one of the worst growth rates in the industry.

- It is tracking to 2 consecutive years of high single-digit earnings declines with no clear plan to reverse the business trend.

- We are still in the early stages of a consumer and economic slowdown, as global GDP estimates are being constantly revised downwards.

Ultimately, we believe the multiple will come down when the market realizes that the consensus expectation for a reacceleration in earnings growth to double digits in 2017 is not very likely to happen.

We remain short TIF stock.

LAZ

To view our analyst's original report on Lazard click here.

No update on Lazard (LAZ) this week but Hedgeye Financials analyst Jonathan Casteleyn reiterates their short call.

FL

To view our analyst's original report on Foot Locker click here.

The biggest near term threat to Foot Locker (FL) earnings and the stock is slowing comparable store sales. In 1Q16 comps slowed to 2.9% from 7.9% the prior quarter. At the same time, main banner e-commerce held relatively steady at about 20% after slowing from 40%+ in 1H15. Our traffic tracking showed a similar trend over the last year. The 2Q to date is showing a clear slowing from 1Q.

The company noted on their conference call three weeks ago that total comps were running negative in the quarter-to-date, saying it was from a shifted Nike shoe launch. But since then we have not seen an improvement in online traffic, which has actually weakened slightly. This could mean more negative pressure on the Footlocker comps over the near term.

DE

To view our analyst's original report on Deere & Company click here.

Is the agricultural economy at trough?

If credit and debt trends are any indication, the answer is no. Farm debt is expanding, which is not a characteristic of an industry at trough. The reversal in farm credit metrics portends lower farmland values, higher credit losses, and lower farm spending.

For Deere & Company (DE), credit trends are a critical valuation point since many investors place a high ‘trough’ multiple on the ~40% of net income from the captive finance subsidiary. We think investors are inappropriately extrapolating the benefits of a robust farm economy and gains in farmland values when evaluating DE’s finance subsidiary. Despite a recent flurry of optimism, we continue to see 30%-50% relative downside for shares of DE, with tightening credit as a key catalyst.

HOLX

Click here to view our analyst's stock report on Hologic (HOLX).