Below are sovereign bond yields for select countries with negative interest rate policies. The graphs show the yield curves for those sovereign bonds today (green line) versus where they were last year (yellow line).

German 10yr:

6/9/15: 0.949%

Today: 0.037%

Click images to enlarge.

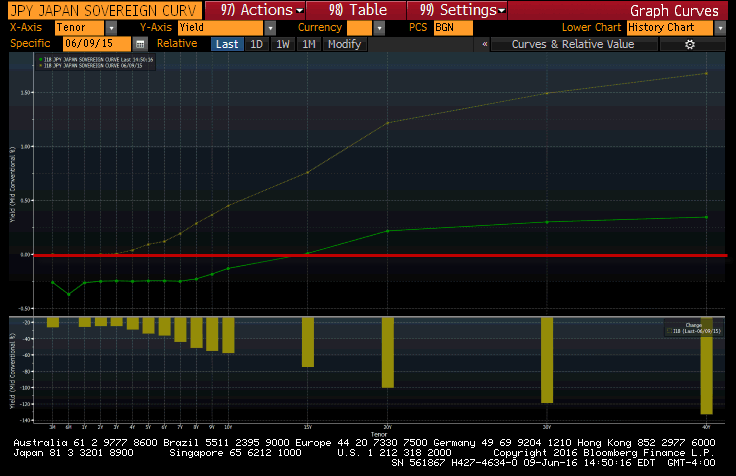

Japanese 10yr:

6/9/15: 0.448%

Today: -0.131%

Swiss 10yr:

6/9/15: 0.211%

Today: -0.48%