Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

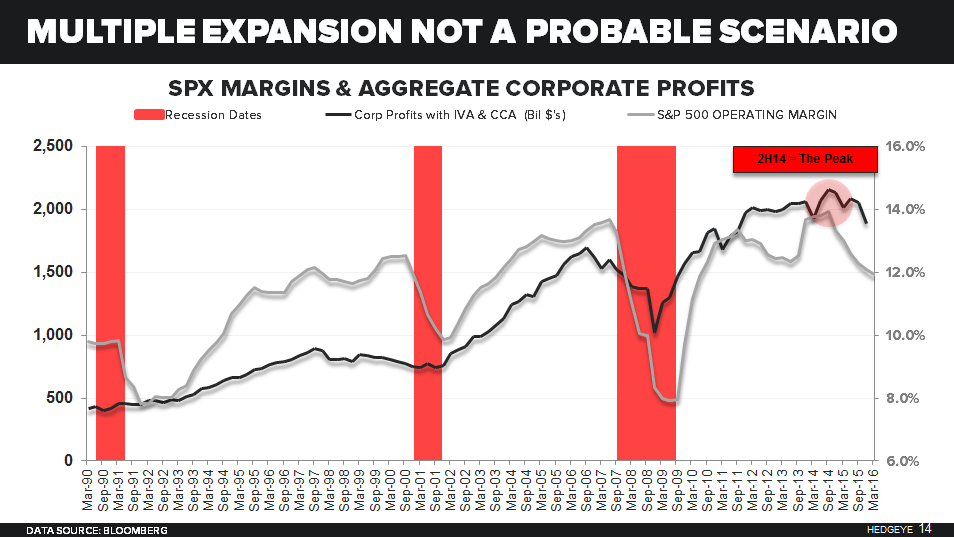

"... As you know, 100% of the time that US corporate profits slow to negative (year-over-year), the SP500 has had a draw-down (crash) of 20% or more. We’re about to see the 3rd consecutive quarter of a US #ProfitRecession. And Q3 of 2016 will probably be the 4th."