Conclusion. We don’t like LULU one bit. In fact, we dislike it a lot. We’re mildly concerned that the company will pull all the stops this quarter in order to silence Chip Wilson, who recently reared his head again and more aggressive than ever about how the company is being mismanaged by both the C-Suite and the Board. But aside from near-term window dressing, we think that returns are headed squarely lower at LULU – by way of both weaker operating turns and eroding margins. Where we live, stocks don’t go up when returns are going down.

Chip Being Chip

It’s been two years since LULU CEO, Laurent Potdevin, said on a conference that “…our parents are fighting and it’s awkward.” 2yrs later there still has been no resolution. Yes, Chip has been on his best behavior – with only a few flare ups – since he sold half his stake to Advent in August 2014, but his recent public moves/statements raise a lot of question marks. A brief synopsis of the timeline: 1) 2/2/16 – Chip exercises his right to appoint an independent director to the BOD when he taps ex LULU CIO, Kathryn Henry, and 2) 6/1/16 – Chip releases a statement questioning the competency of the corporate governors/management of the company that he started.

We largely agree with Chip’s voiced sentiments around the lack of a long term strategic plan. Though we think it’s important to keep in mind that many of the ‘managerial flaws’ Chip is attacking were set up when he held the reins. Outside of the drama, we think the company is on red-alert after Chip went public with his discontent last week. Could it be that Chip was pressed into action after catching wind of an upcoming earnings disappointment? It’s possible. But, our sense is that the company will want to rub Chip’s nose in this earnings release. In other words, it will find any way imaginable not to miss.

Valuation/Sentiment

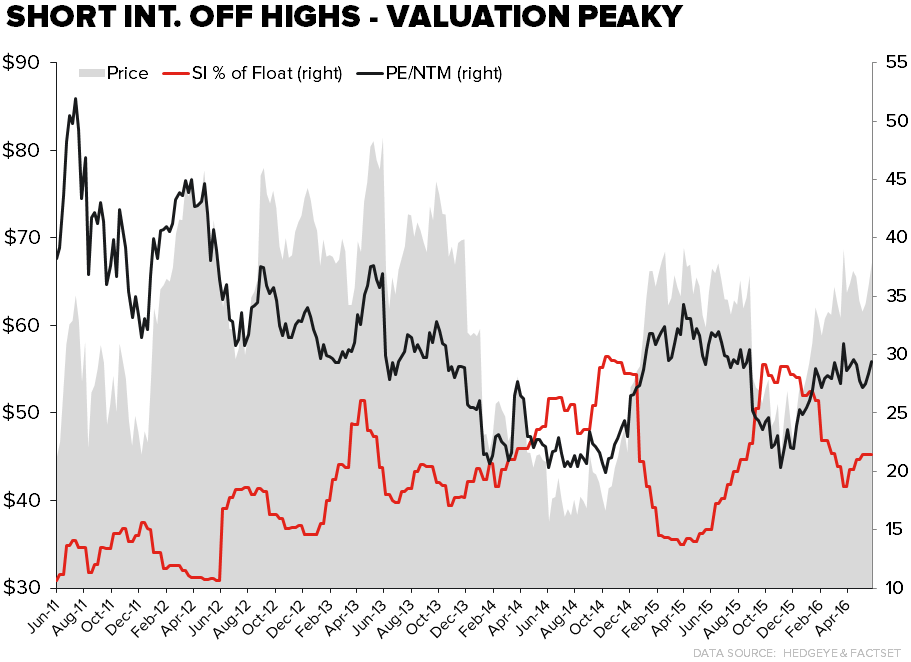

Since the positive holiday sales print ahead of the ICR conference in January, short interest has come off all-time highs to still elevated levels just north of 20%. Valuation is peaky at 30x P/E, and the company now trades at a premium to UA on both EV/EBITDA and EV/Sales. That’d be well and good if LULU’s presented 5yr financial targets were at all within the realm of possibility, but we have a very hard time with the idea that sales will double in 5 years at the same time op-margins recover despite the fact that LULU’s growth is coming from less profitable vehicles. We outlined this growth disconnect in our deck published on April 11th (click here to access LULU materials).

The point here is that in many of our conversations, most investors give LULU the benefit of the doubt on this Fiscal Year. Meaning that margins will begin to inflect, inventory will come back in line, and sales will continue to outperform the rest of US retail. We’d argue that at this price – those near-term benefits are more than priced in.

Category Considerations

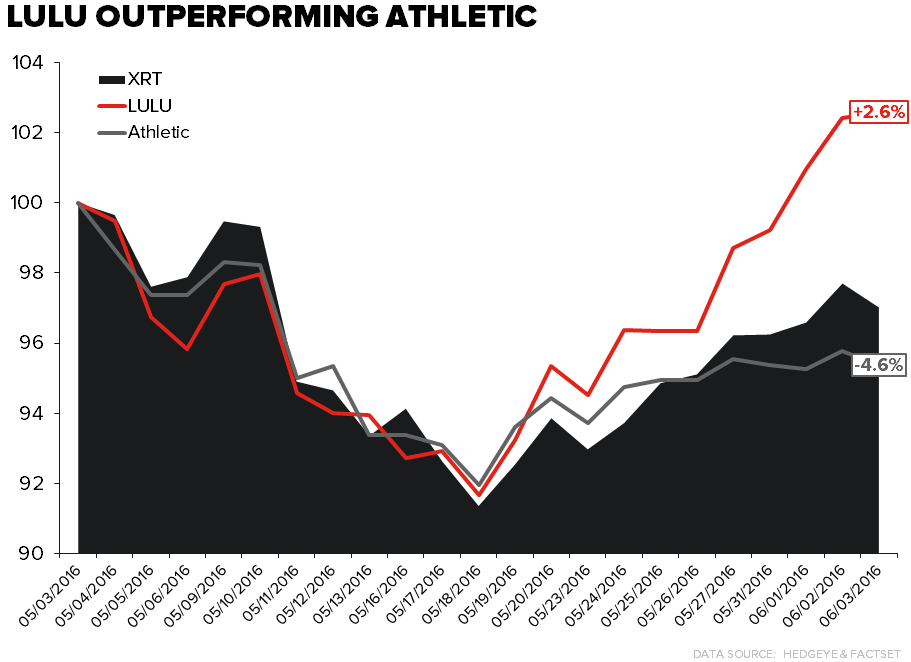

It’s been a noisy month for the athletic space. This is a loose definition including: NKE, UA, LULU, AdiBok, FL, and DKS. Each name has its own specific issues but it kicked off in the 3rd week of May with the FL earnings print, where the company was as negative on Nike as we’ve heard in 14 years. Then UA took down guidance at the end of May due to the TSA bankruptcy. Every name in the space, with the exception of AdiBok and LULU, has felt the pain ever since. And rightly so, in the case of LULU, as much of the pressure facing the rest of the brands/retailers in its competitive set is focused on footwear and the bankruptcy of a largely irrelevant competitor to LULU.

Based on the commentary during this earnings season, it appears that LULU is sitting in the sweet spot from a product standpoint, as FL noted that it’s SIX:02 concept experienced negative apparel comps as taste shifted away from athletic performance towards athletic lifestyle. That’s LULU’s core offering. But, it’s what happens below the line that’s more important with this print as the company has added and incremental $470mm in revenue over the past two years but EBIT dollars have declined by $22mm for an incremental margin of -5%. This has to matter to the ‘perennially bullish on LULU’ investment community at some point.

Inventory

It’s been a long time since we can remember this much attention focused on the balance sheet for a company with a growthy multiple like LULU. To be clear - at 30x earnings and 17x EBITDA – LULU has no margin of error when it comes to its inventory position. That’s largely due to the fact that much of this year’s promised inflection in profitability is hinged on increased efficiency in the supply chain.

After pushing expectations for a cleaner inventory position from the end of FY15 into the first quarter this year, current guidance promises that inventories will be in line with forward sales expectations. Compares are easy as the sales to inventory spread hit 40% through the midpoint of FY15, but we want to be explicitly clear that LULU has no margin for error as the inventory balance is one of the only benchmarks the company has pointed to in order for the street to gauge the progress in the company’s supply chain initiatives.

For a company with a big growth multiple and eroding returns, we think the emphasis on improved efficiency proves how hairy this story is. There is certainly a lot of wood this company needs to chop to improve the back of house, but will ultimately make LULU a multi-year growth story is investment across all buckets of the P&L, especially those that will drive outsized market share growth. Those aren’t a point of emphasis today in Vancouver.