KATE shares ended the week down 5%, capped off by a -7% move over the final two trading days of the week. The catalyst for the move was negative commentary at investor meetings about traffic-induced headwinds in the US outlet channel. Before we say here ‘we go again’, let’s put that commentary into context.

For starters let’s remember the cardinal rule when it comes to corporate communication at KATE… watch what they do, not what they say. While the communication issues are much improved over the past 12 months – it’s still a risk to the story – which came to fruition last week. However, the proof has been in the pudding for this company as it has continued to print best in class/industry comp growth. Talking up outlet headwinds could be a strategy as simple as management trying to keep expectations grounded. Current Street estimates call for a 13.5% comp this quarter, or a 220bps deceleration on the 2yr trend. We think that’s beatable, and that KATE will put up a mid-teen comp and $0.16 in EPS.

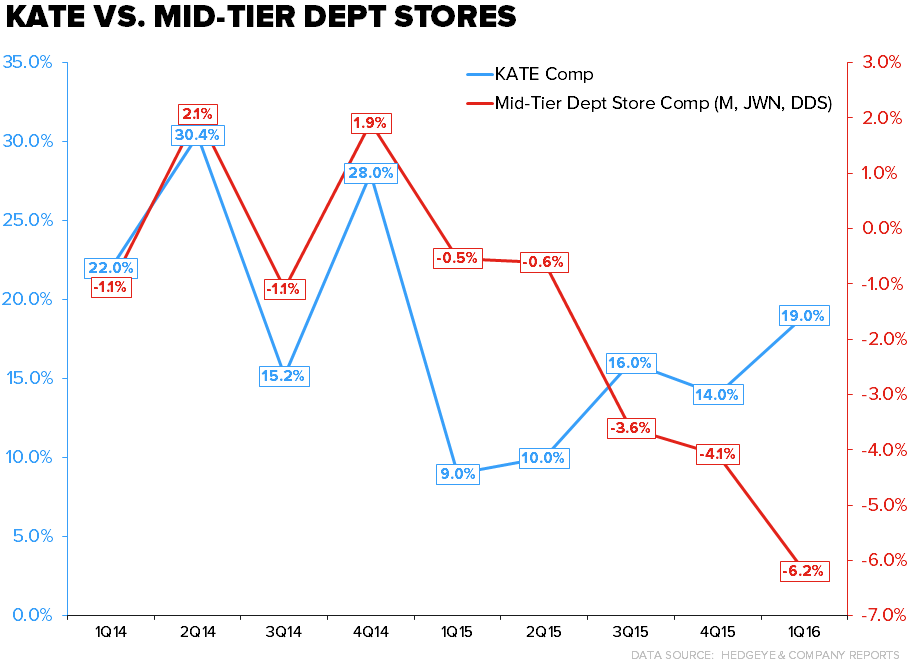

Let’s also remember that the company has been open about the traffic and ticket issues plaguing the outlet channels -- especially in tourist centric centers over the past two quarters. In other words, this is nothing new – and it put up a 19% comp last quarter alone. In addition, the continued softness in the outlet channel was baked into guidance for FY16, and b) conditions in this channel haven’t gotten material softer since the company communicated with the street a month ago. To those worried about softness across the rest of retail – we’d note that KATE has been the one name we can point to that has bucked the comp slowdown. And it hasn’t been about geographic diversification, mind you, as the company’s NA exposure has actually gone up 500bps over the past 2 years.

We think the reason for the pullback over the past week is losing the forest for the trees. More important to the KATE story, is the fact that this company has lost money every year since 2007. Despite having strong sales momentum over the past three years, it had no EPS, and only a convoluted non-GAAP Adjusted EBITDA number that was impossible to model. When the ‘handbag space’ melted down – KATE’s brand was fine, but its stock was annihilated because it had zero earnings/cash flow and valuation support. Well, that ends now. When all is said and done, we’re at $0.85 this year and a 3-year CAGR of 54% through 2018. Even if we’re wrong and KATE ‘only’ earns the consensus, we’re still looking at a 44% CAGR. We can count on one hand the number of companies that will put up that kind growth in US Retail.