Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we removed Pimco 25+ Year Zero Coupon US Treasury ETF (ZROZ) and Utilities (XLU), and added Hologic (HOLX) to the short side of Investing Ideas. Please see below Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | GLD | JNK

To view our analyst's original report on Junk Bonds click here and here for Gold.

This week, we took off some exposure to #GrowthSlowing, as yield-chasing allocations with rate hike and yield curve risk were on the table. And no, we didn't do it because “growth is back” or “PMIs are bottoming.” It's simply that numerous Fed heads, including Janet herself have echoed a hawkish tone into the summer.

Last Friday (05/27), Yellen said that, based on her estimate of where the US economy is headed, the Federal Reserve will “probably” raise rates in June or July. Unfortunately, with the possibility of a major policy mistake, it’s a risk we have to respect.

That was the commentary that closed out a deflationary month of May – USD +3.1% with Gold -6.3% and the long end of the Treasury curve and the S&P roughly flat. Fast forward a week. Gold, the Treasury market, and Federal Fund futures don’t buy the hawkish rhetoric for a second.

We’ve shown our chart of the Y/Y% change in Non-Farm Payrolls numerous times, so Friday’s Jobs report was no surprise to us. Consumption and labor market strength are classic late-cycle indicators, but eventually these indicators peak and roll-over in rate-of change terms. Here's the Jobs Report breakdown:

- Non-Farm payroll additions totaled +38K in May vs. +160K est. and +160K prior. While the number was a bomb for those who follow the month-to-month sequential change (which is useless), we expected the weakness. To be clear, history paints a very clear picture. NFP additions peaked in Q1 of 2015 and have since rolled over. It’s part of #TheCycle.

Here's what that did for Investing Ideas subscribers' Macro positioning on the week:

- Long Bonds (TLT): +5.2%

- Gold (GLD): +2.0%

- Junk Bonds (JNK): -0.3%

Adding fuel to the TLT/GLD fire, Friday’s ISM Services (a typical late cycle indicator) fell to its lowest level since May 2013:

Friday’s jobs report represented a complete shift to any renewed expectations of a June/July hike. The yield spread ended the week pinned near the bottom of the cycle low at 92 basis points (10yr-2yr yield %). And, looking at real-time rate hike expectations, the bid-yield of December 2016 Federal Funds Futures Contracts dipped 8 basis points day-over-day, implying the market’s expectations for the first rate hike is now in 2017!:

MCD

To view our analyst's original report on McDonald's click here.

McDonald's (MCD) is testing fresh beef in 14 Dallas-area restaurants in an attempt to become a modern progressive burger company and better compete with smaller, premium chains. Part of the reason they haven’t done this in the past is because there hasn’t been enough supply of fresh beef for their demand.

The initiative will expand further to more markets over the course of the year to test both consumer perception and their supply chains ability. This could be a big move for MCD that will undoubtedly improve food quality and consumer perception of the company.

Also in the news over the last couple of weeks is MCD’s plan to move its HQ from Oak Brook to downtown Chicago. Although not important from an operational perspective immediately, it will help the company attract and retain top talent which will be beneficial overtime. MCD remains one of our top ideas in the Restaurant space.

HOLX

We had a great call with a former salesperson from Hologic (HOLX) who sold 3D mammography equipment. We learned a few things that confirmed our outlook and added to our confidence in the short call. It’s also been interesting to get so much interest from our buyside clients these days after we were largely alone on an island when we were on the long side.

This week, for one of those clients, we spent time critiquing a model from a major ranked analyst which, at the end of the day, wasn’t that hard to pick apart. Initially, when we opened the model, it looked detailed and comprehensive with a few hundred lines of data seemingly pointed at continued growth in 3D mammo. But it turned out the driver underneath the 3D revenue line item was hard coded, meaning the analyst had merely punched in a number. None of the hundreds of lines mattered! Meanwhile, in other parts of the model, we also found that the output appeared to be totally irrational.

Additionally, with non-farm payrolls coming in weak at +38K, we have another downside risk to work on. Medical consumers are insured consumers, and many of Hologic’s customers are employed, commercially insured women. If Non-farm payrolls slow (and possibly even decline) so too with Hologic’s revenue.

We still like the short here.

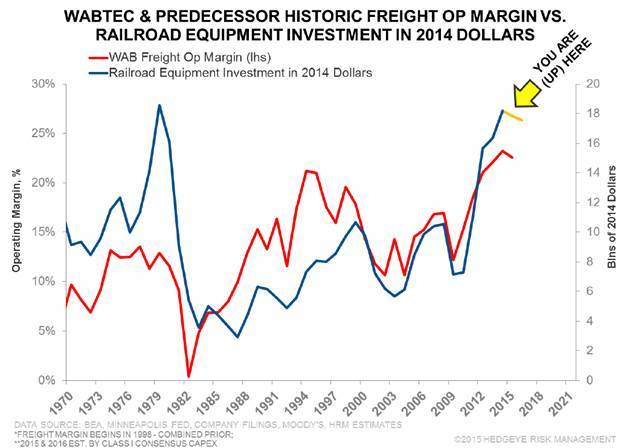

WAB

To view our analyst's original report on Wabtec click here.

We'll say it again. When a bull story hinges on the acquisition of a French manufacturing company, we think investors should recognize a serious problem. A few additional acquisition-related things to think about:

- The Faiveley acquisition has been postponed to at least the fourth quarter due to further requests from the EU regulators;

- To make matters worse, the DOJ has not formally weighed in on the proposed acquisition;

Taken together, we think the Faiveley deal is unlikely to be completed in its current form.

Bottom Line: Given weak rail volumes, poor railcar and locomotive orders, we continue to see Wabtech (WAB) as a promising short, and expect 2016 EPS ex-Faiveley below $4/share as the company’s core freight market enters a multi-year downturn.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is an update on ZBH from Healthcare analyst Tom Tobin.

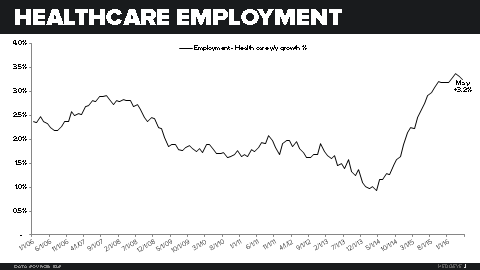

The weak (+38K) non-farm payroll update this morning does a couple of things to our opinion of the Zimmer Biomet (ZBH) short. (Note: We initiated our call last year at $115 and it had been in positive territory when it touched $90 in October 2015 and then again in February 2016, but acknowledge we've been on the wrong side of it in the last few months.)

We think the ACA increased volume temporarily in 2014 and 2015 for a host of Healthcare companies including hospitals, physician offices and orthopedic manufacturers. As we enter the late part of the economic cycle broadly and the inflated Healthcare caused by the ACA, we think ZBH and its peers will be struggling with declining volume and increasing price pressure.

For May, Healthcare employment continues to show it is in stall mode, coming in at +3.2% year over year and +0.7% on a rate of change basis. The JOLTS report for Healthcare job openings set to report next week will be the next update. If ACA is rolling over and medical consumption with it, we think ZBH will as well.

HBI

To view our analyst's original report on Hanesbrands click here.

The acquisitions Hanesbrands (HBI) has been making have become more and more expensive, and amount to ever higher risk. Here's why:

- One should wonder why management would make these deals at the tail end of an economic upcycle;

- The HBI incentive structure is part of the problem. 60% of management’s performance criteria is sales and EPS excluding actions (meaning after non-gaap charges). So management can increase its performance simply by acquiring brands, and taking charges at the highest rate possible;

- Meanwhile, shareholders are left owning weak assets that HBI paid too much for, presenting a risk to long term growth and earnings;

Case in point, when HBI updated its guidance this week, to include expected results for its pending acquisitions of Champion Europe and Pacific Brands, the company raised 2016 revenue by $350mm, and raised adjusted EPS by just 4 cents, which could be entirely explained by a lower tax rate.

We understand that HBI plans to make the grow the businesses and make them more profitable, but there is a lot of execution risk in cleaning up the combined businesses for which it paid 12x EBITDA.

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin's (NUS) CFO Ritch Wood spoke at the RBC Capital Markets Consumer and Retail Conference in Boston on June 2, 2016. The conversation did not provide us with any reason to be concerned about our short call. He openly said that the only way NUS can drive the top line is to increase the number of sales leaders. This implies what we have been arguing is a major negative for the company, that the revenue per sales leader is not growing and the company doesn’t predict that it will either.

We continue to love this on the short side, and feel that the recent run up in the stock, whether it be from short covering or share buy backs, represents a great opportunity to short NUS.

MDRX

To view our analyst's original report on Allscripts click here.

No update on Allscripts (MDRX) this week but Hedgeye Healthcare analysts Tom Tobin and Andrew Freedman reiterate their short call.

TIF

To view our analyst's original report on Tiffany click here.

The update on Tiffany (TIF) e-commerce traffic through the first month of the 2nd quarter reveals a poor trend with no improvement in the negative traffic rank change. Management is planning an underlying improvement in the business for the back half of the year, even as each recent quarter has been getting worse on the margin. Needless to say, we do not see this improvement happening, but we will keep a close eye on the data for any positive inflections.

Expectations for earnings for 2016 remain too high as the market seems to believe management guidance, which has been wrong for 18 months straight.

LAZ

To view our analyst's original report on Lazard click here.

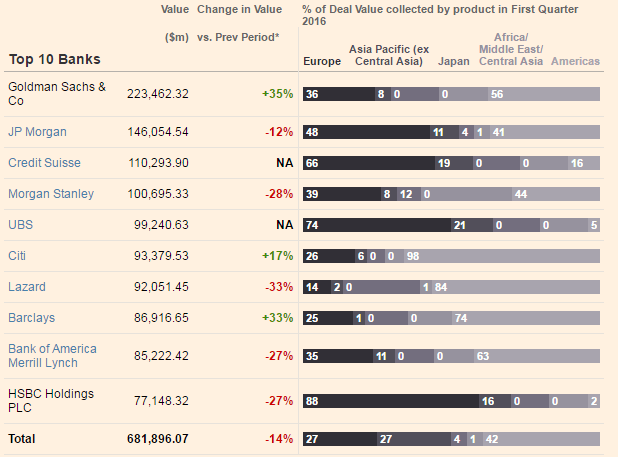

The warning signs of an even tougher year for M&A activity came by way of the industry leader Goldman Sachs this week. Despite having already announced a -5% reduction in its overall workforce at the beginning of the year, Goldman announced further headcount reductions this week specifically in M&A and also parts of its trading operations.

While the midweek announcement didn’t specify numbers, the industry leader in announced volume undergoing a cost rationalization exercise means that M&A pipelines are drying up and that secondary players are also struggling. Goldman, at the #1 spot in year-to-date M&A activity, even has announced volume up +35% year-over-year versus the substantial slack in the -33% decline in YTD volume at Lazard (LAZ).

Thus, the prospective environment is so challenging in the eyes of Goldman that proactive cost reductions are warranted. We continue to outline a $3 per share earnings estimate for Lazard, -15% below consensus, with a Bear case outcome of $2.20 per share, some ~40% below the Street in a dire market environment. Our fair value range continues at $22-30 per share for LAZ shares.

FL

To view our analyst's original report on Foot Locker click here.

On their recent 1Q conference call, Foot Locker (FL) management was as bearish on Nike as they have been in roughly 56 quarters. At first, it was the discussion about how Basketball was down mid-single digits in the quarter. Mind you, basketball is 40% of the revenue, and Nike has a 95%+ share of FL basketball. That’s about 38% of FL's revenue base that was under pressure.

But then we heard CEO Johnson talk of the ‘big turn’ at Adidas, and how he would like more product from both Adidas and UnderArmour. This type of commentary could be very dangerous for FL. FL earnings grew immensely over the last 10 years aided by the driving force of increasing Nike penetration in its store from 50% up to 73%. In 2015, it seems that Nike at FL hit a ceiling.

Now, if FL is going to move away from Nike, in spirit or in actual product orders, it could lead Nike to move its best product elsewhere. This would mean reduced traffic, and margin pressure for FL. So, whether Nike product is struggling, or Nike decides to take down the FL product allocations, it's bad for Foot Locker in either case.

DE

To view our analyst's original report on Deere & Company click here.

Deere & Company (DE) is and will remain a value trap. We expect the P/E ratio, which was <9x on peak FY13 in early 2014, to steadily expand as the shares underperform and earnings drop faster than the share price. While there is often an urge to call the cycle turn, particularly in a larger index weight, those bottom callers typically become bag holders.

Given the large used equipment overhang, excess capacity, competitive pressure, and deteriorating farm credit, we don’t think the risk of missing the next Ag upturn should be a concern, even for very long-term investors.