Are department stores an endangered species?

Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe discusses why department stores are slowly fading away. "The downward arc started well over a decade ago—long before the Great Recession," Howe writes. "In fact, you need to go back to the Clinton ‘90s to find a really healthy growth year for department stores... Those days are long gone."

WHAT’S HAPPENING?

Department store executives were hoping ahead of earnings season that they wouldn’t have to break more bad news to the investors who remain onboard.

No such luck.

Top players like Dillard’s, Macy’s, and Nordstrom reported their worst YOY same-store sales results since the Great Recession, with some seeing drops in the 5 percent range (or more, in Macy’s case). Forecasters at Green Street Advisors estimate that it would take closing one-fifth of the industry’s total mall floor space to get department stores back to their pre-recession sales per square foot.

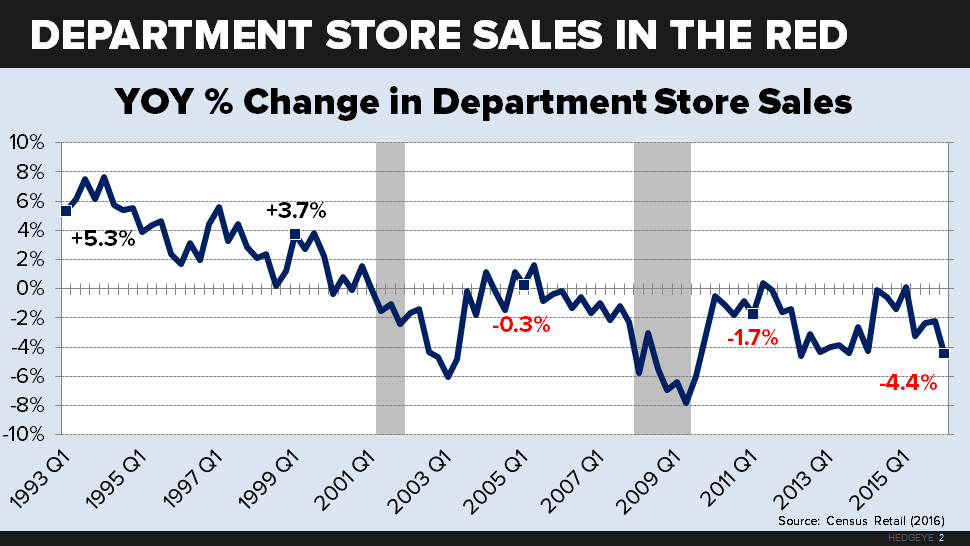

The downward arc started well over a decade ago—long before the Great Recession. In fact, you need to go back to the Clinton ‘90s to find a really healthy growth year for department stores. That was back when we were still building malls and when malls were still cool in the eyes of teen “mall rats” (all Gen-Xers) who wandered around in movies like Clueless.

Those days are long gone. As a whole, department stores have only had a handful of quarters of positive sales growth since the dot-com bubble burst. Millennials, unlike Xers, equate department stores with slow extinction and think of malls as places to go not be seen (see deadmalls.com).

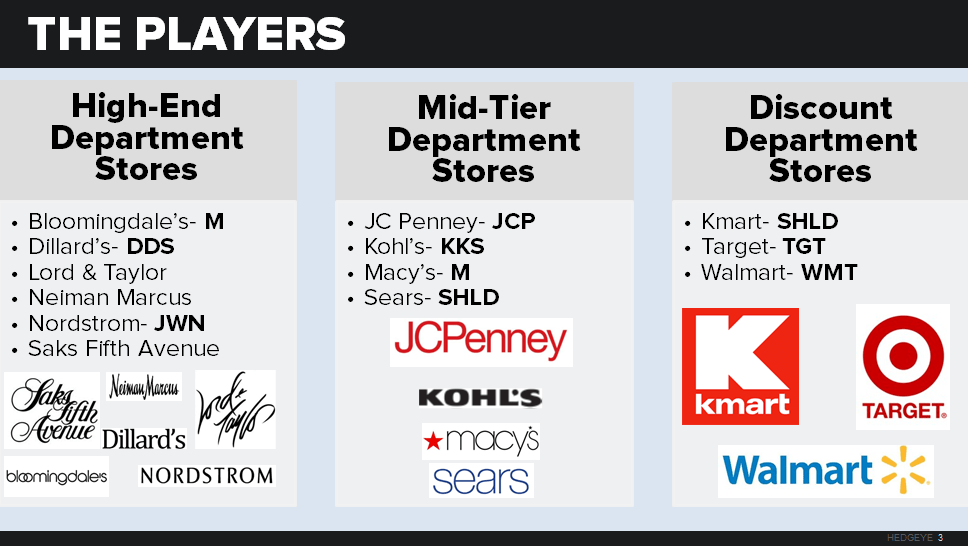

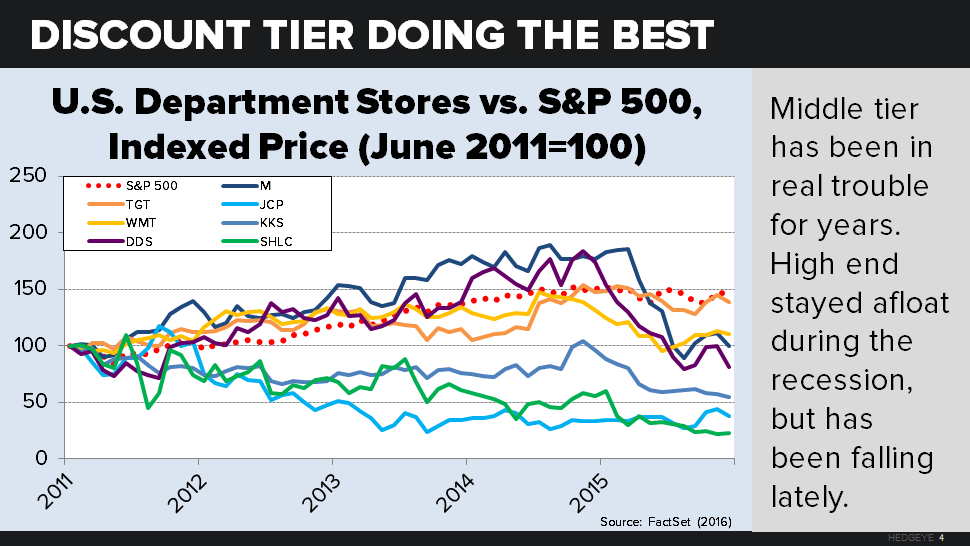

It’s useful to divide department stores into three basic tiers: upscale, middle, and discount. All tiers have performed poorly over the last 15 fifteen years, but some have done better than others. Overall, the discount tier—including Target and Walmart—has done the best. These stores kept their value better during the recession, and they have dropped less since last spring.

The upscale firms like Saks Fifth Avenue, Nordstrom, and Neiman Marcus have done less well. And as for middle tier stores like JC Penney, Macy’s, Sears, and Kohl’s, well, by all accounts they’ve been getting hammered. Problem for the middle tier: they can’t beat the upper tier on quality, and they can’t beat the lower tier on price.

Share prices tell the story. JC Penney sits below $8, nearly the lowest price in the company’s 30-plus year history. Upper-skewing firms like Dillard’s and Macy’s (which owns Bloomingdale’s) fared better than most until the middle of last year—at which point they too tumbled down to earth. In fact, all department stores not named Walmart or Target have actually lost value since 2011, making the benchmark S&P 500 look like a star performer by comparison.

WHY IT’S HAPPENING: DRIVERS

Product lines: In April, when total retail sales posted a YOY gain of +3.0%—a good-news surprise to most analysts—department stores shared none of the bounty. Their YOY gain was -0.3%. One obvious drag is that department stores happen to be dominated by precisely those product categories where sales growth throughout the economy has been weakest in recent years: clothing and accessories (+1.3% YOY in April), electronics and appliances (-2.0%), and food and beverages (+1.9%). Quite simply, department store sales are harnessed to the weakest horses.

The product-line picture isn’t totally bleak. Many stores sell furniture and home furnishings (+3.6% YOY in April) or sporting goods, hobby, books, and music (+4.2%). Yet most of this growth has been captured by specialty stores. Department stores tend to target the nonspecialized mainstream. And here, the sharing economy rules. Shoppers who might otherwise spend hundreds on a brand-new average-looking couch at Walmart or Macy’s can now buy a slightly used one on Craigslist for a sliver of the price.

An ever-shrinking middle class. Pew Research reported that in 2015, for the first time ever, fewer consumers lived in households earning between two-thirds and double the median income (120.8 million) than in lower- and higher-earning households (121.3 million). Another Pew study found that, between 2000 and 2014, the middle class lost ground in nearly nine out of ten U.S. metro areas.

This new “hourglass economy,” where most spending takes place at the high and low ends, threatens department stores that always relied upon middle-earning households.

Generational change. It’s not just the “middle class” as an income bracket that’s waning—but also the “middle class” as a collective self-image.

From their very origins in the late-19th century, department stores have always targeted the “middle-of -the-road” consumer with standard fare at standard prices. (Thanks to the economies of scale provided by catalogues and railroad delivery, Sears, Roebuck, and Company was the amazon-like behemoth of its day.)

After World War II, these firms enjoyed a new growth spurt with the G.I. and Silent generations, who embodied Middle America in every sense. These “Great Society” architects saw department stores as a way to infuse order and efficiency into the wild west of Mom-and-Pop retail. As consumers, they craved uniformity and mass-produced goods—stuff that would allow you to fit in happily with your suburban neighbors on a “Pleasant Valley Sunday.”

But this all changed with Boomers, who wanted authentic products made just for them, as unique individuals. Today, Boomer and Gen-X shoppers are either “trading up” for better quality or “trading down” for better price. Department stores check neither box.

In response to Boomers and Xers, department stores have been gradually ramping up on the diversity of its style and brand selection—until all the diversity practically pours out of the shelves onto the floors. But here’s the irony. Most Millennials no longer want what department stores have lately been emphasizing: more choice. Plenty would rather shop at a specialty store that effectively chooses the right product for them than at a sprawling department store that offers forty different brands of handbags scattered down three separate aisles.

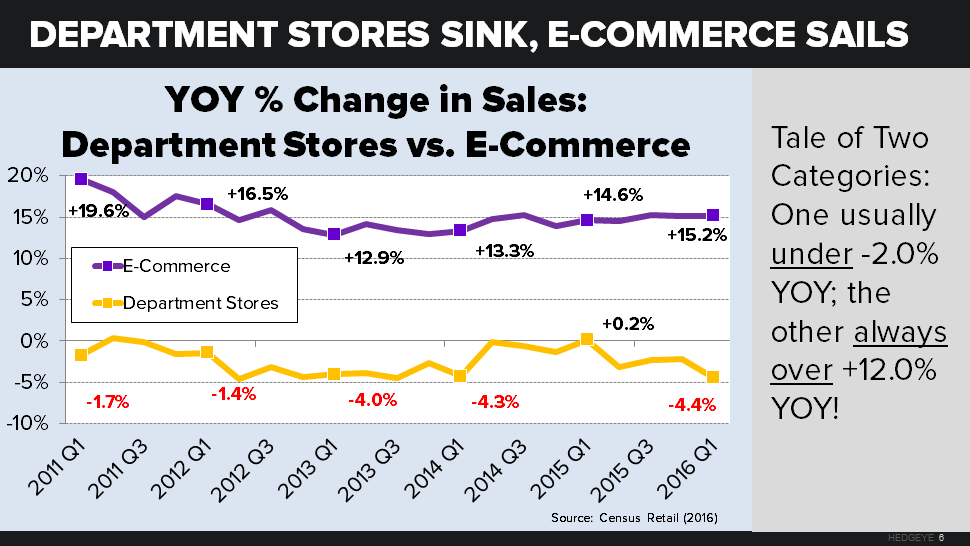

The rise of e-commerce. Online platforms allow consumers to get exactly what they want without ever leaving the couch. E-commerce sales now make up nearly 70 cents for every dollar spent at brick-and-mortar stores, up from around 30 cents per dollar back in 2000. The gap between e-tail revenue growth and department store revenue growth is on the order of 15 to 20 percentage points annually. It’s not even close.

E-commerce transactions are not just convenient, but fast: Why trek out to the mall when Amazon Prime will deliver what you need within the day—or even the hour?

HOW DEPARTMENT STORES ARE RESPONDING

Upper- and middle-tier firms are going cheap. In a grab for consumers with less purchasing power, Macy’s is experimenting with “Backstage,” an outlet store built into a handful of its existing retail locations. (Macy’s experiment with no sales and no promotions was a disaster, which should have told them something about who their customers are.)

Luxury firms are no strangers to this strategy, either. At Saks Off 5th, shoppers can get Saks quality for a modest price. As for Nordstrom, the company’s Nordstrom Rack discount outposts now outnumber its legacy stores. Who can blame them? While Nordstrom’s full-priced sales recently dropped 4.3 percent YOY, its discount business grew 4.6 percent.

Goodbye, soft goods. Department stores are branching out into hard goods to escape the doldrums of apparel sales. JC Penney announced earlier this year that it would start selling appliances again for the first time in decades. Macy’s recently added consumer electronics in some of its stores through a partnership with Best Buy.

Sears is taking it one step further: The firm has opened a 10,000-square-foot outpost in Colorado packed only with appliances.

Investing in private labels. At a time when bestsellers are hard to come by, department stores are hanging onto their homegrown cash cows for dear life.

Kohl’s offers 20 exclusive private labels, three of which generate more than $1 billion annually—including its star-performing Sonoma brand.

Under new CEO Marvin Ellison, JC Penney has gotten back into in-house labels as well—a strategy that has provided a 6.6 percentage-point boost to the company’s gross margins over the past three years.

Emulating e-commerce giants. Macy’s, Bloomingdale’s, and Nordstrom have taken a page out of Amazon’s playbook by rolling out same-day delivery in select locations.

That’s a good start, sure, but these firms should go a step further by exploiting things that brock-and-mortar does better than e-commerce: high-touch customer service, perhaps, or maybe specializing in large, complex purchases that beg for a knowledgeable salesperson. With in-store analytics married to Big Data, physical retail can at last know as much about its customers as digital retail.

IS IT WORKING?

Not yet—but the industry still has hope. Despite the runaway success of e-commerce, there may be room for one or two traditional department stores that play their cards right. As for the rest, some will disappear (receivership, merger) and others will exit the genre by becoming high-end specialty stores or big-box category killers.

So which firms have the best shot of surviving and prospering?

It’s hard to say for certain, of course. But I would bet heavily against today’s middle-tier firms. It will be tough for any of them to turn the tide without completely reinventing themselves to compete with either the Nordstroms of the world on quality or the Walmarts on price. High- and low-end firms are better positioned to exploit what they do best and maybe, just maybe, stop the bleeding.

Many of the high-end stores will survive by specializing in fewer product lines. Most discount stores don’t have that option—and will be hardest pressed by e-tailers. Yet precisely because they have no alternative, these discount stores will be most likely to figure out how to grow their bottom line while still maintaining their department store identity.

They will do so in part on the strength of their brand connection with the fast-growing share of Americans (40% in 2014, up from only 25% in 2008 according to Pew Research) who self-identify as “lower” or “lower-middle” class. The generation most responsible for this shift is today’s Millennials, who also happen to be tomorrow’s middle class. Hip young Gen-Xers flocked to edgy boutiques. Hip young Millennials flock to one-size-fits-all thrift shops.

Already, a couple of the big discount brands are aligning themselves well. Just look at Target, one of the few firms investors haven’t yet given up on. It has combined a bright, upmarket atmosphere with basics-first selection and downmarket prices—in other words, Target offers what Millennials want. Walmart, meanwhile, beats everyone on price, an identity in itself. That’s why the two companies rank among the top ten favorite Millennial brands.

TAKEAWAYS

- Department stores are hurting. Their once-reliable middle-class customer base is dwindling, and today’s consumers are either splurging for better goods or going elsewhere for lower prices.

- Companies are trying everything to turn the tide, from offering lower-priced goods to investing in private labels. But in the end, middle-tier firms may be too far behind already to make up the distance. Bet on the discount tier to become the future core of this retail category.