“A bad anchor can easily produce a bad estimate.”

-Phil Tetlock

On Friday @Harvard, Janet Yellen said that, based on her estimate of where the US economy is at, the Federal Reserve will “probably” raise rates in June or July… Ok. What if she raises and her estimates are wrong (again)?

As Phil Tetlock explains in Superforecasting: “When we make estimates we tend to start with some number and adjust. The number we start with is called the anchor. It’s important because we typically underadjust, which means a bad anchor can easily produce a bad estimate. And it’s astonishingly easy to settle on a bad anchor.” (pg 120)

Like they did when they raised rates into the Q1 slow-down (DEC), the Fed is anchoring on a +2-3% GDP scenario for Q2. They’re also anchoring on a #LateCycle view of US Labor, which has clearly slowed since their bad anchor led to bad estimates in Q1. Since the Fed’s forecast has always been one of the biggest risks to macro markets, I don’t see why consensus is complacent about that now.

Back to the Global Macro Grind…

Complacent? “Keith, everyone is bearish – this is why markets are gonna rip.”

Let me get this straight – the only reason why markets didn’t keep crashing in FEB-MAR is that Janet Yellen went dovish as the data did, the US Dollar careened to the downside, and reflation ripped…

And now, markets are “gonna rip” based on a low-probability scenario that the Fed’s forecast for growth to magically re-accelerate (into peak of #TheCycle compares in Q2) is accurate? #Cool. Good luck with that.

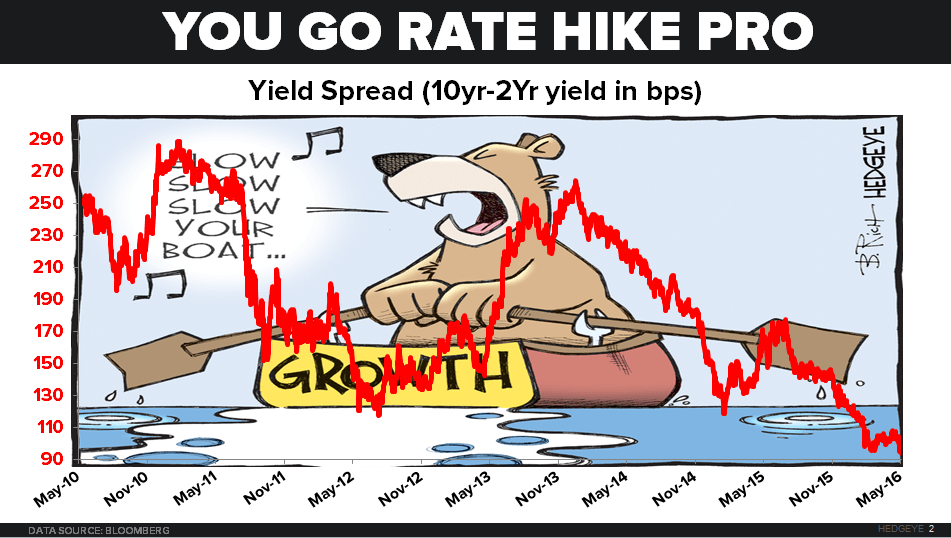

We’re sticking with our forecast of GDP sub 1% for Q2 and the worst profits of #TheCycle in Q2 and Q3. Alongside #EmploymentSlowing, we remain The Bears on #EarningsSlowing. We expect The Financials (XLF) to lead on the downside of earnings with the Yield Spread (10yr minus 2yr) not budging last week (still at YTD lows of 94 basis points wide).

Back to the complacency factor, on last week’s slow-volume-month-end-markup (Total US Equity Volume including dark pool down over 20% vs. the 1-month average), here’s what CFTC futures & options net positioning did:

- SP500 (Index + E-mini) moved to its largest net LONG position of 2016 at +95,251 contracts

- 10YR Treasury net SHORT position came in small to -93,475 contracts

- Gold net LONG position came in bigger than small to +169,491 contracts

To put that net LONG position in US Equity Beta in context, that’s 2.73x its 1-year z-score!

*anything plus or minus 2.0x is usually a fade signal, from a sentiment perspective

Since I didn’t think the Fed would be stubborn enough to stay with a pseudo “mid-cycle” economic view, I didn’t think they’d pivot from hawkish (DEC) to dovish (MAR-APR) back to hawkish (MAY)… but I guess I thought wrong (I thought she was data dependent!).

That’s why I sent out SELL signals (i.e. take down exposures) to my favorite intermediate to long-term LONG ideas after listening to Janet on Friday. After having such a great start to the year by simply staying with #TheCycle call, why would I just let the Fed making a policy mistake eat into my family’s hard earned absolute returns?

In the end, I think the Fed will be proven wrong (again) and the curve will continue to flatten as the rate of change in US economic growth slows in Q2 and Q3. But in between now and the end, I have to deal with the risk these bad Fed estimates impose on my portfolio’s preferred asset allocation. So this is what the Hedgeye Asset Allocation Model’s key moves look like, in context:

- CASH going to 77% (from 49% when US Equities hit their May lows)

- Taking US Equities from 6% back to 0% (like I did in late DEC)

- Taking Fixed Income 31% to 11% (i.e. from 91% of my max exposure to 33%)

I’ve also cut my net asset allocation (I’m a former Hedge Fund PM so I think of all my positions on a net longs vs. shorts basis) to commodities from 10% net long to 6%. Yeah, I know – maybe I should cut that to 0% too (Gold, which I like, was -3.1% last week).

After writing this letter to many of you for going on 8 years now, I realize that how I think about my personal asset allocation isn’t for most Institutional Investors. That said, I’m ok with that because instead of some marketing message, it’s the transparent truth. I’m not an institutional investor anymore and many of you who are can still go to 77% cash in your own accounts anyway!

Since there are no rules against the Fed flip-flopping from hawkish-to-dovish-to-hawkish, why shouldn’t I operate with the same short-termism? Rates can easily rise from 1.70% (where they went to post the recent rate of change #EmploymentSlowing report) to 2.00% on Fed rhetoric, only to crash right back to 1.70% again.

That’s what we call moving the MOVE Index (Bond Market Volatility). And there’s no historical precedent for that being a short-term bullish catalyst for either high beta stocks or junk bonds. You’ll be able to thank the Fed’s bad estimates for that. I know I will. That’s when I get to buy-back everything I sold higher, lower (again), by having a better estimate of intermediate-term growth.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.75-1.91%

SPX 2040-2110

RUT 1105-1160

VIX 12.74-17.18

USD 94.58-95.95

Oil (WTI) 46.53-50.14

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer