Despite the irony of Treasury Secretary Jack Lew scolding Japan for devaluing the yen at the G7 meeting over the weekend (after years of Fed US Dollar devaluation), all the G7 bloviating didn’t change much in macro markets. The top correlation risk in macro markets remains the US Dollar.

As McCullough writes in a note to subscribers this morning, with the U.S. dollar index up for the third straight week, that's taking the hatchet to European equities:

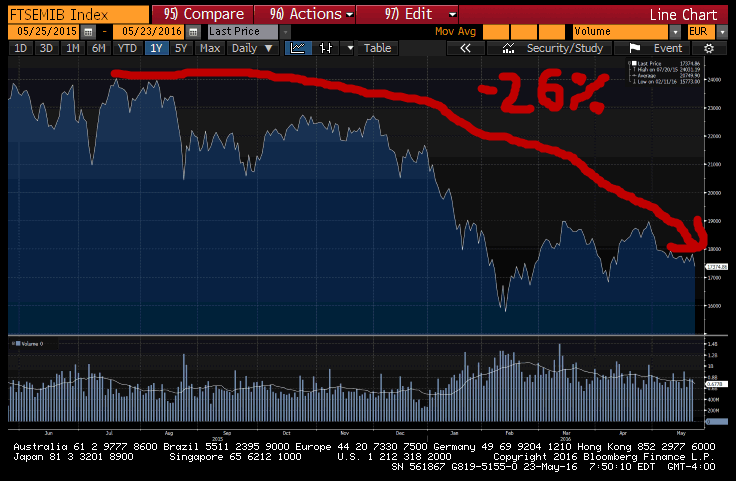

"Europe teetering on implosion (Equities) again as USD signals immediate-term TRADE overbought vs. Euro at $1.11-1.12; Italy’s stock market is a bloody mess, -1.5% (leading losers), taking its crash to -26% since this time last year; NIRP doesn’t work."

With ECB head Draghi struggling to arrest the crash, the continued implosion of European equities is yet more evidence of the central planning #BeliefSystem gone awry.