Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added Gold (GLD) to the long side of Investing Ideas. Our Macro team will send out a full stock report on Gold next week. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

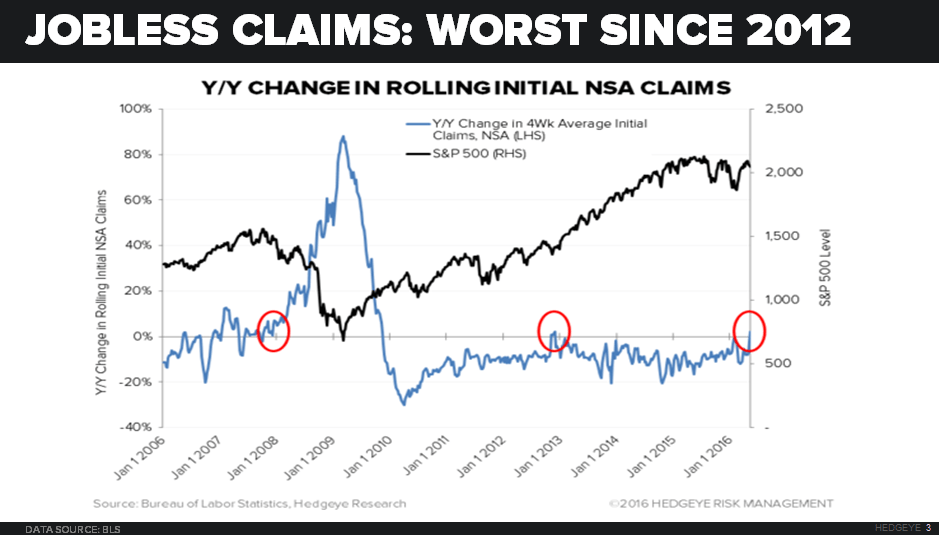

If you haven’t yet, you got another chance to buy long-term Treasuries at lower highs this week. (In Real-Time Alerts, Keith McCullough signaled a good buying opportunity in TLT on Wednesday for those who aren’t already long a continuation in growth slowing.)

If you’re already long of Long Bonds (TLT, ZROZ), stick with it. None of the relevant data released this past week suggests that growth could inflect and trend positive:

- Thursday’s Jobless Claims Report was the worst print, in Y/Y rate of change terms, since 2012, and it was the fourth consecutive week of increasing jobless claims

- Industrial Production declined -1.1% Y/Y for April, marking the 8th consecutive month of Y/Y contraction: #IndustrialRecession

Tying together a continued deceleration in growth with policy expectations, the most important callout is that our expectation for growth in Q2 is well below consensus and Fed expectations (which have been horribly inaccurate). When Janet does have to acknowledge deterioration, we expect the policy shift to be dollar bearish on the margin. And, to the contrary, if the Fed RAISES RATES (June) into this slow-down, they’ll be the catalyst for DEFLATION (down yields) again anyway.

And there’s nothing Gold (GLD) likes more than a falling dollar and falling interest rates which is why we added it to the long-side of Investing Ideas this week. Remember, this is the same week various Fed members were in public calling for a rate hike with the worst jobless claims print since 2012. #GoodLuck.

It's clear to us that U.S. growth continues to slow. For this reason, buy more of what’s working: Long Bonds (TLT, ZROZ), Utilities (XLU), Junk Bonds (JNK) and Gold (GLD).

MCD

To view our analyst's original report on McDonald's click here.

McDonald's (MCD) continues to evolve. The company's latest step is testing never frozen burgers at 14 units in the Dallas, TX area. This initiative could give them the ability to compete with better burger concepts such as Shake Shack, In-N-Out and Five Guys.

Meanwhile, there has been chatter about the lack of identity for their value platform in 2Q16. MCD is truly still in the testing phase as to what their national value message will be. We can appreciate the fact that they are testing multiple formats before fully committing.

In the meantime, the tailwind from all-day breakfast will continue to propel growth going forward, until lapping this initiative in 4Q16. We continue to favor MCD as one of the best LONGs in the market right now, due to actual growth and style factors that are friendly in volatile markets.

WAB

To view our analyst's original report on Wabtec click here.

When a bull story hinges on the acquisition of a French manufacturing company, we think investors should recognize a problem. Especially since that acquisition has been postponed to at least the fourth quarter due to further requests from the EU regulators. To make matters worse, the DOJ has not formally weighed in on the proposed acquisition. We think the Faiveley deal is unlikely to be completed in its current form.

So given weak rail volumes, poor railcar and locomotive orders, we continue to see Wabtech (WAB) as a promising short, and expect 2016 EPS ex-Faiveley below $4/share as the company’s core freight market enters a multi-year downturn.

HBI

To view our analyst's original report on Hanesbrands click here.

We’re hosting an institutional call on Monday, May 23rd to review our thesis on Hanesbrands (HBI).

Here's a synopsis. This HBI short goes beyond the whole ‘peak margins, low cotton cost, in a weak category’ argument. HBI has a management team that was aggressive, but is now behaving in a borderline reckless manner. Management is aggressively selling stock while it uses shareholder capital to accelerate acquisition activity at increasingly high (and potentially deceptive) multiples at the tail-end of an economic cycle, as its own factories operate near peak utilization. These deals are supporting earnings, while the Street looks right through the special charges. Ultimately, we see 40% downside from here.

We’ll be back with updates following the call.

NUS

To view our analyst's original report on Nu Skin click here.

No update on Nu Skin (NUS) this week but Hedgeye Consumer Staples analysts Howard Penney and Shayne Laidlaw reiterate their short call.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Politico sponsored a webcast this week where Cliff Deveny of Catholic Health said that admissions to nursing homes for patients undergoing joint replacement has dropped -45% under the CCJR. That is an incredible result and points to success for Catholic Health not just in lowering the post-acute care costs (nursing homes are more expensive than home care) but also the other buckets of savings likely to occur under the program in the coming years.

Click here to view the webcast.

After the post acute savings on nursing home care, there will be savings from delaying surgery for potentially high-cost patients who have heart disease or obesity, and finally the cost of the implant. We continue to think the fundamentals for Zimmer-Biomet (ZBH) and the ortho sector are going to deteriorate over the coming quarters with the CCJR just one part of the thesis.

* * *

On a related note, earlier this week, our Healthcare analysts Tom Tobin and Andrew Freedman were on HedgeyeTV discussing their top ideas, including Allscripts (MDRX), Athenahealth (ATHN), Hologic (HOLX), Illumina (ILMN).

Tobin and Freedman also explained the latest trends in the Healthcare space like their #ACATaper thesis and provided an update on the JOLTS report with implications for HCA Holdings (HCA) and AMN Healthcare Services (AHS).

Click the image below to watch the replay.

Click here to access the associate slides.

MDRX

To view our analyst's original report on Allscripts click here. Below is an excerpt from a research note on Allscripts (MDRX) written by our Healthcare analysts Tom Tobin and Andrew Freedman.

FIELD NOTES (ATHN, MDRX, QSII, #GREENWAY) | WINNERS AND LOSERS

Takeaway: Competitive gap widens as vendors struggle to find their way amid a slowing EHR market; replacement activity driving share to the winners.

overview

We spoke with a former Greenway Salesperson to gauge the current state of the ambulatory market and for any read-through to public peers ATHN, MDRX and QSII. Greenway Health sells EHR and Practice Management solutions primarily to physician offices. Greenway was acquired by private equity firm, Vista Equity, in 2013 for $644 million and subsequently merged with Vista's other portfolio EHR company, Vitera Healthcare. Greenway's three main products are 1) Greenway 2) Sage-Success and 3) Intergy, and combined represent approximately 6% of the ambulatory practice management market today. Below are our key takeaways:

- Greenway had a very difficult bookings year in 2015, with only 20% of sales reps hitting quota and firm hitting 50% of their revenue target.... "Replacement market never happened". <- Compared to athenahealth who had strong 2015 bookings year, and came in 110% of quota in the comparable small and group segment.

- Three products are not integrated, and focus was on selling Greenway suite. <- Results in confusion among customers, salesforce and added support costs to vendor.

- Customer support and system downtime was a big problem, resulting in customer dissatisfaction and retention problems. <- Very hard to recover from, same problems with Allscripts and CareCloud.

- Contract structure and pricing not competitive, with 3-5 year terms and $700 per doc per month for combined EHR/PM system. <- athenahealth no contract, 90-day cancellation and % of collections model; flexibility is huge value to providers.

- Never won any business from athenahealth or eClinicalWorks. 10-15% of new business came from Allscripts customers. <- athenahealth's competitive position strengthening relative to MDRX and QSII.

- Entered RCM market 2-years ago and focus turned to selling RCM due to 3-4x contract size, but with modest success.

- Health system consolidation and hospital's acquiring independent practices remains a headwind to growth.

winners and losers

Anecdotes and data continue support our view that in a post-stimulus environment, market share will accrue to the top vendors (ATHN, CERN, eClinicalWorks and Epic) in a market that remains highly fragmented. Replacement purchase decisions will be driven by value, quality and performance, where initial decisions were made in haste to capture stimulus dollars. Additionally, provisions within MACRA support the adoption of open and interoperable systems, which athenahealth is the most favorably disposed, in our view.

- "Most formidable competitor for us was athena..." <- Integrated Offering, Better Sales Pitch "This is how much money we will make you" and 90-day cancellation policy

- "...we built that thing together with post-it notes and it is still held together with post-it notes" <- Referencing Allscripts

- "...no one took Allscripts seriously and they were easy to beat."

- "Allscripts may have a more pissed off customer base than Greenway."

- "...hospitals were just gobbling up practices and putting them on Epic."

We would emphasize that athenahealth's core competency, value-prop and competitive advantage remains their revenue cycle management capabilities as part of an integrated clinical solution. RCM is a market that struggling EHR-centric companies have turned too for growth as the core EHR market slows, but have found little success due to their limited track-record. We are seeing this play out across the space based on our checks with PracticeFusion, CareCloud, Greenway, McKesson, GE, NextGen and Allscripts over the last 6-months.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) reports 1Q earnings on Wednesday, May 25th. Looking at recent data points, it seems that this event is more likely to be negative than positive.

- Last week Macy's reported declining 2 year comp trends. Over the last year, comps for TIF Americas have moved relatively in line with Macy's, and both companies have discussed the negative impact of reduced foreign tourist traffic.

- Ralph Lauren Corp also noted that sales to foreign tourists were down 25% in the quarter, even working against easier compares from tourism weakness in the quarter last year.

- TIF CFO Ralph Nicoletti notified the company on May 10th that he would leave on May 20th to take a job with a different company. This comes just 1 month after he stood up in front of analysts at their investor day to lay out the companys financial goals. Generally, executives don’t leave when the team is executing and business is accelerating.

This quarter may not reveal a headline miss. 1Q EPS expectations are low, as they should be, since management guided the quarter to be down 15-20% y/y, and sales trends have not shown a bottom. But we believe that the back half acceleration management is hoping for is becoming less and less likely to happen. Translation…earnings expectations need to come down again.

LAZ

To view our analyst's original report on Lazard click here.

No update on Lazard (LAZ) this week but Financials analyst Jonathan Casteleyn reiterates his short call.

FL

To view our analyst's original report on Foot Locker click here.

Yesterday’s Foot Locker (FL) earnings call marked the most bearish that management has been on Nike in roughly 56 quarters.

Yes, that’s 14 years…but who’s counting?

No, this is not a clash of the two 800lb gorillas like in 2002 arguing over FL’s order cuts in the wake of the Vince Carter Shox appealing to virtually nobody except Carter himself (not even in the Raptor’s home market of Toronto). But, at least to us, FL management was super cautious on Nike. At first it was the discussion about how Basketball was down mid-single digits in the quarter. And mind you, basketball is 40% of the revenue, and Nike has a 95%+ share of FL basketball. That’s about 38% of FL revenue base that was under pressure. But then we heard CEO Johnson talk of the ‘big turn’ at Adidas, and how he would like more product from both Adidas and UnderArmour.

Then one thing became abundantly clear to us…

As FL took its ‘Nike Ratio’ (the % of product it sells that is Nike) from 40% to 73% over this economic cycle, it lost the ability to think and act on its own. You heard it in management’s tone “we WANT more Adidas and UnderArmour, but Nike won’t let us.” Our sense is that FL wants maybe 50% of its store to be Nike, but unfortunately it has to take a lot of Nike’s junky product (yes, Nike makes some junk) and excess inventory in order to be assured premium allocation of the good stuff.

But, Nike stuffing FL with swooshes is absolutely NOT ok, when comps decelerate, FL’s most profitable business is down, it’s missing out on hot product from other brands that are gaining momentum, expenses pick up – causing FL to delever SG&A in a 1Q for the first time since the Great Recession – and EPS growth slows to the lowest rate since 4Q09.

Even though we think FL is a solid short, we absolutely believe that the company has a good management team. A good management team, however, will look at its brand portfolio, and take action when 72% of its business belongs to a brand that is changing up the footwear distribution paradigm. It’s got to be clear to FL management that this dependence on a single brand is no longer working – at least if it wants to accelerate growth and returns. The risk there is that FL cuts 2-3% of expected sales, and then Nike responds by cutting 10% – and giving the increment to DKS in order to stabilize that part of the wholesale channel.

All in, we give FL all the credit in the world for its comments. But the reality is that it sticks with 70%+ Nike and faces an eroding earnings algorithm, or it diversifies away from Nike and faces potential business risk. Sure, FL is down today in an up tape. But this short call is far from over. Estimates remain too high, and we think we’ll see multiple compression repeatedly over the next year.

DE

To view our analyst's original report on Deere & Company click here.

We will let others summarize Deere & Company's (DE) quarter, but we want to lay out what we think longs are missing in Deere. DE is and will remain a value trap. We expect the P/E ratio, which was <9x on peak FY13 in early 2014, to steadily expand as the shares underperform and earnings drop faster than the share price.

While there is often an urge to call the cycle turn, particularly in a larger index weight, those bottom callers typically become bag holders. Given the large used equipment overhang, excess capacity, competitive pressure, and deteriorating farm credit, we don’t think the risk of missing the next Ag upturn should be a concern, even for very long-term investors.