Editor's Note: Below is a brief excerpt and charts from an institutional research note written by Materials analysts Jay Van Sciver and Ben Ryan with critical insights for the Ag industry and specifically companies like Agrium (AGU), CF Industries (CF), Mosaic (MOS) and Potash (POT). To read our Materials team's institutional research email sales@hedgeye.com.

The big question that will be answered in the intermediate-term is the effect of credit contraction, repayment rates, and land values on farmer input consumption trends. As we’ve highlighted with our recent calls in the Ag. space, we believe a deterioration in these metrics will prove meaningful:

- The Chicago Farm Loan Repayment Index contracted from 43 at the end of Q4 to 32 through Q1 (-44% Y/Y) while the Chicago Fed Farm Loan Demand Index increased to 156 from 134 through Q4 (+11% Y/Y) – The Chicago Fed Fund Loan Availability Index was flat Y/Y.

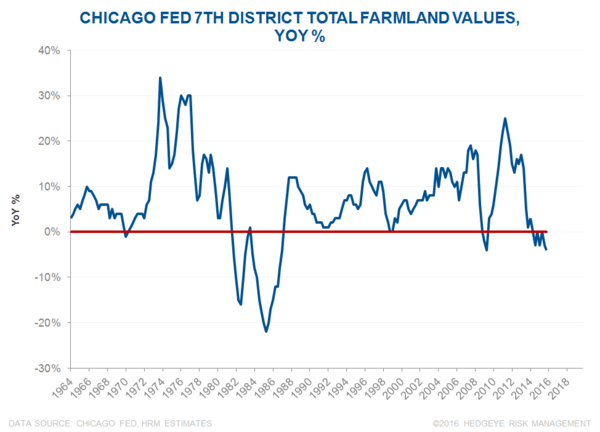

- The Federal Reserve Bank of Chicago 7th District measurement of farmland values shows that farmland values are down -4% Y/Y, the largest rate of deceleration since Q3 of 2009. Cash rental rates for the 7th district are down -10% Y/Y.