Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye U.S. Macro analyst Christian Drake. Click here to learn more.

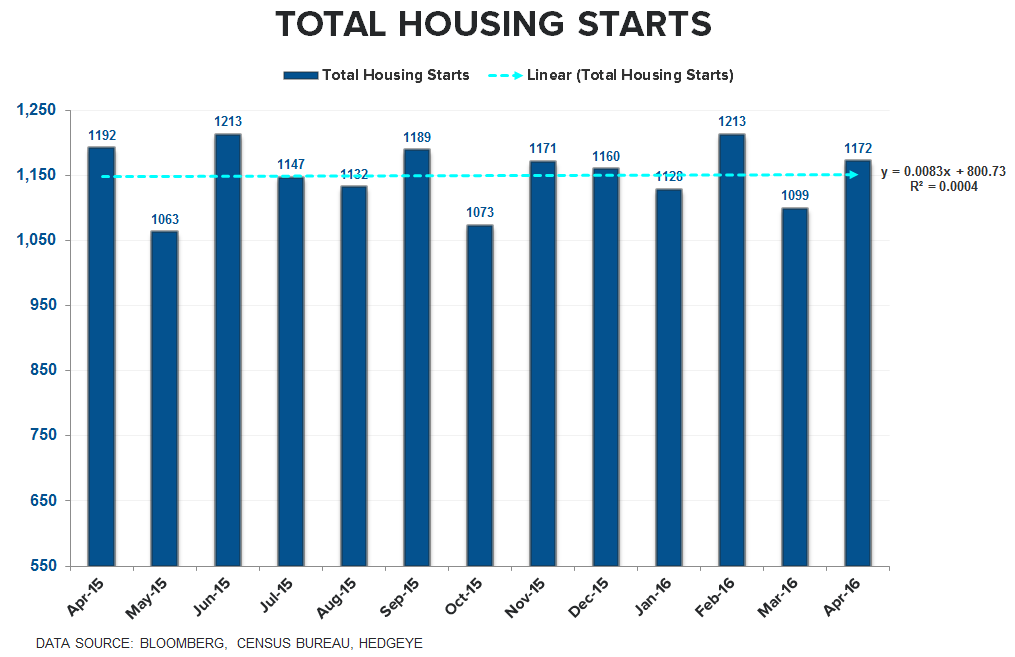

"... I’m going to give you a TTM slope and you tell me what macro series it belongs to:

- Slope = 0.00

- Slope = -0.00

- Slope = 0.02

- Last 4 Months Change: +0.0, +0.0, +0.0, +0.0

Answers:

- Housing Starts

- Pending Home Sales

- New Home Sales

- Builder Confidence"