Head-scratcher of the day via the Wall Street Journal:

"Brighter economic data raises specter of Fed rate increase; yield curve is flattest since 2007."

Huh?

Here's a better explanation as to why... ugly S&P 1Q16 earnings:

The bond market is signaling a precarious reality... a.k.a. #GrowthSlowing. Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

"Yield spread flattening = leading indicator of economic slowing – at 94bps wide this am (10yr minus 2yr) that’s a fresh YTD low and it’s driven by the 2yr popping to 0.84% on concern the Fed will hike on a rising CPI? If the Fed raises rates in June, they will make US Equity Beta Bears happy (reminder: rising inflation takes DOWN our Street low GDP forecast for Q2)."

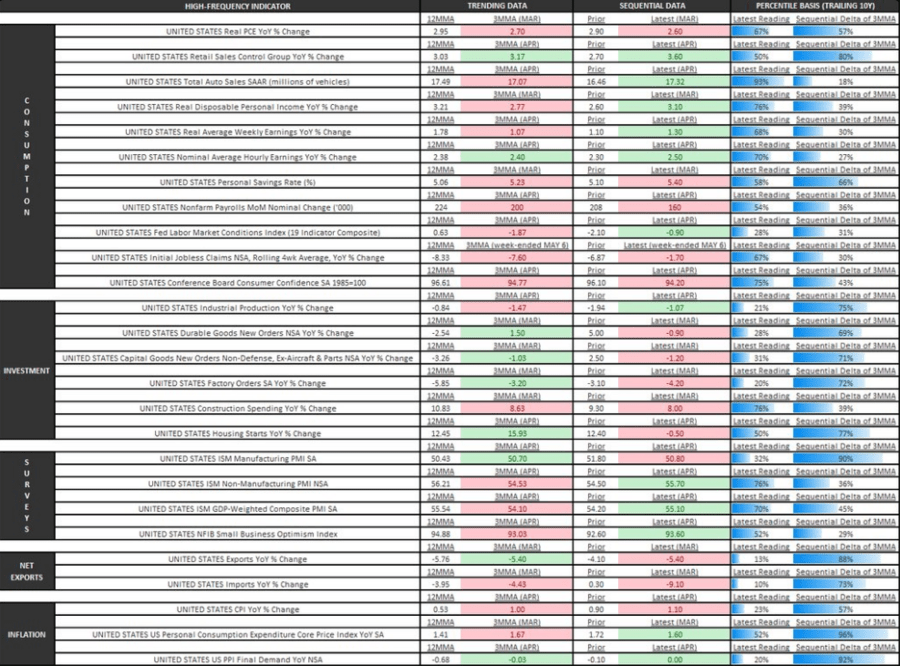

Addressing all the supposedly "brighter" data, Hedgeye Senior Macro analyst Darius Dale provides this chart of the recently reported key economic releases. Dale writes:

"U.S. Economic Summary: green shoots where the trend remains bearish; red shoots where the trend has likely bottomed."

Click image to enlarge

Dale continues:

"Not much to do with those [sequential green shoots] other than trust the forward-looking components of our process, such as Mr. Market himself."

... A.K.A. the 10s/2s spread. Here's the yield spread.

Click to enlarge

What do you do with that?

Dale's conclusion:

"This is our third or fourth short-term headfake in domestic economic data since the cycle peaked in 1H15. Elongate your memory. FYI, the TSY 10s-2s spread compressing to new cycle lows is not exactly a bullish indicator... See through the S/T headfake in the data."

In other words.. stick with your #GrowthSlowing positions... Long Bonds (TLT) and Utilities (XLU).