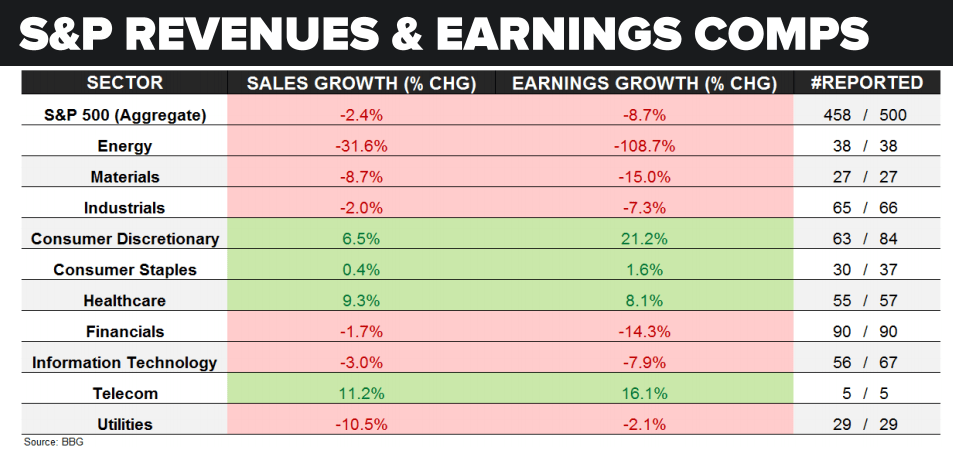

A total of 458/500 S&P 500 companies have reported aggregate sales and earnings growth down -2.4% and -8.7% respectively.

Here's the breakdown by sector:

- So far, 6 of 10 sectors have reported negative sales and earnings growth;

- Our favorite sector short, Financials (XLF), reported sales and earnings growth down -1.7% and -14.3%;

- Energy (XLE) sales and earnings growth down -31.6% and -108.7% respectively;

Click image to enlarge