The good news is that we think that WSM will grow earnings by 10%, which seems decent enough in this tape at face value. The bad news is that we’re talking 10% growth from last year through fiscal 2019 – and that’s not a CAGR, it’s total EPS growth over four-years. And if you were to ask us the over/under, we’d say that there’s a much better chance of earnings starting with a $2 than a $4 in any year therein. That’s our way of saying we absolutely do not like this company, its structure, its management team or its prospects. We think we have some compelling analysis to show how growth is coming from more price-sensitive consumers, at a point where brand growth is weighted towards the wrong end of the portfolio.

Duration Matters. We really really don’t like this company or stock long term (what we’d call a TAIL duration – 3-years or less). We also don’t like it over the Intermediate term (TREND – 3-months or more). But…and it’s a big but…our model does not point to a meaningful miss this quarter. Could the company guide down? Yes. It’s possible. But we wouldn’t call this a TRADE (3 weeks or less) into tomorrow’s print. Based on what we know today, we’d get heavy on the short side after the event – potentially even if we miss this one and it trades down. If you have the luxury of ignoring a print with 14% of the float short, then by all means, short away. Over a medium to long-term duration it should prove to be the right call.

HERE ARE SOME KEY FACTORS DRIVING OUR NEGATIVE VIEW

Management: We’ve gotta start with our strong view that this management team simply doesn’t have the chops, the vision, and perhaps even the authority to do what it takes to turn this company from Good to Great in what is going to be the most dynamic retail climate in a generation.

What’s even more troubling than the choppiness on the top line we’ve seen reported over the past 6 months is management’s inability to articulate the root causes of the slowdown across all banners or identify clear and definable investments that need to be made in order to reignite the top line.

The WSM plan going forward is a patchwork investment plan centered around infrastructure additions, SKU reduction, store portfolio rationalization/improvement, and employment cuts. That screams defense to us. It’d be a different story if the company were going to take the additional cash flow saved after streamlining the back-end and reinvested that back into the value equation to stop sales from sliding. That’s not the case. The punchline is that a company in any industry rarely can cut costs and manufacture growth at the same time. Making minor strategic changes after a negative event – and not knowing why – is a recipe for disaster in this business.

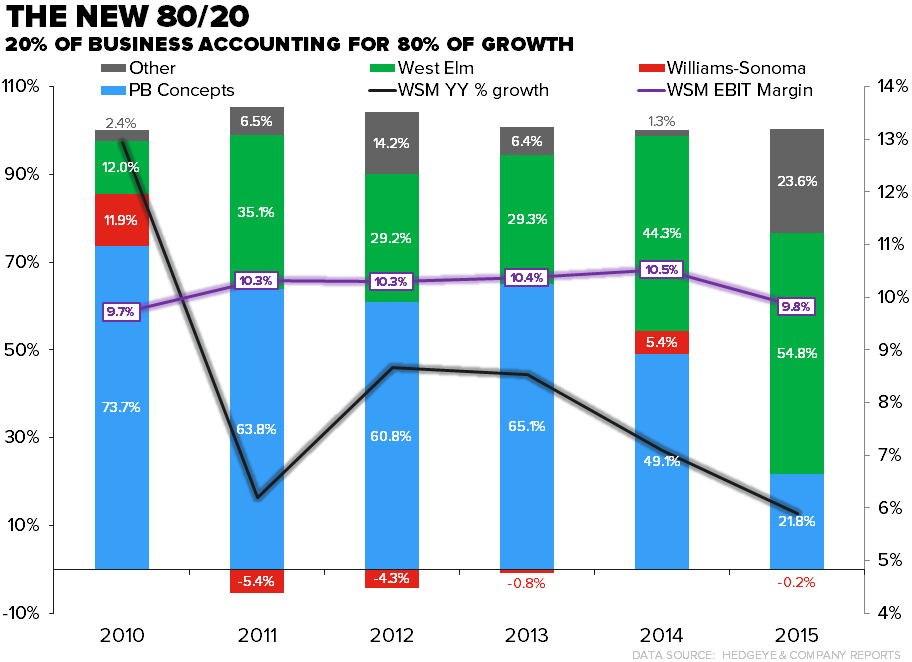

The New 80/20: For the better part of this economic cycle, the gravy train for WSM has been sustained market share gains in Pottery Barn on essentially flat square footage. Prior to 2015, PB (inclusive of Kids and Teen) amounted for the lion’s share of growth. That manifested itself in high-single digit comps taking operating margins from the recession trough of 2% into the double digits. That growth appears to have hit a wall, as the company looks to realign the brand once again to attract of lower demographic. Never a multiple inducing event.

Incremental growth is now coming from two sources, West Elm and Intl/New Brands, which collectively amount to 20% of the revenue base, but in the past year accounted for 80% of the growth. Those will continue to be the growth vehicle’s going forward, as the company continues to prune its fixed assets in the PB and Williams-Sonoma banners. We’d argue that those are the two most important assets to the long term health and profitability of the company. And, the numbers speak for themselves…as the core business slows so too does the profitability of the parent company. Organic growth from non-core parts of the business is perfectly healthy, but to have 80% of the business headed into the tank for a company that needs mid-to-high single digit comp growth in order to keep operating margins steady strikes us as particularly bearish.

The Wayfair Disruption: The home furnishings market in the US is highly fragmented, with no player in the space in excess of 6% share of its respective market in the brick and mortar channel (Wayfair is tops at over 10% of the online channel). So, this isn’t necessarily a market share battle pitting WSM vs. W, when over 80% of the market is still comprised of mom and pop operators. Is W pulling some dollars out of WSM’s pocket? We think the answer is most definitely yes, but what might even more troubling to the WSM management team is the need to compete with a company with an operating margin in the red. That defines deflationary environment, and the company has all but confirmed that it would play the game as it talked to the need to emphasize lower cost items in its Pottery Barn brands on its most recent call in March. “We'll strategically expand our mix of opening price points across key areas of the business and highlight these price points to attract a broader customer base”.

The numbers speak for themselves, as Wayfair has taken a disproportionate share of the online furnishing spend, with over 1/3rd of the incremental online furnishing spend over the past year. If we pull back the timeline an additional 12 months, the numbers stack up like this: WSM $400mm added online over the past 24 months and Wayfair 3x that at $1.3bn. With 75% of WSM’s growth coming from online over the past 5 years, the addition of competent (yet unprofitable) competitor with no bottom line to protect makes things much more difficult going forward.

Not only have we seen the pressure in the reported numbers, but when we dig a little deeper into the customer visitation behavior online, we can see a high overlap in visitation between the two sites. That number is trending up, with the customers visiting both sites (Wayfair and WSM’s family of brands) in the first quarter months of Feb-Apr up ~350bps.

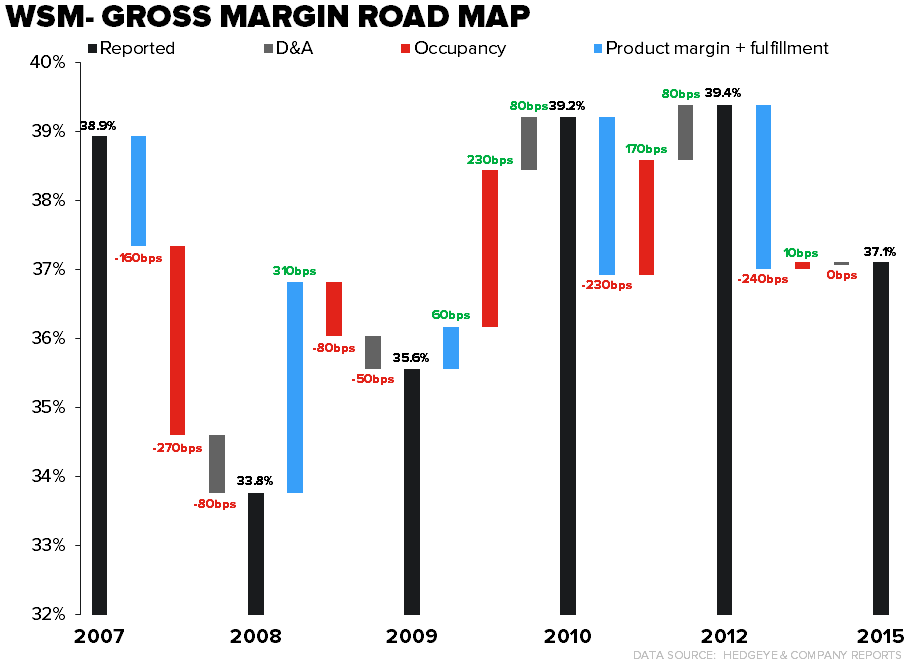

Few Levers Left To Pull: Since the dark-days of 08-09 we’ve seen gross margins recover from recession lows to just shy of 40%. What’s more important is the composition of that expansion. Primarily a) 410bps of occupancy leverage as the company culled its portfolio and renegotiated lease terms with landlords through and out of the recession, and b) 470 bps of product margin/fulfillment deleverage as the online penetration went from 41% in 2010 to 51% in 2015. The occupancy lever has dried up over the past 3 years as the company pushes into more expensive international wholly owned stores – the offset to that is closing stores, but that will impact the e-commerce channel. Product margins will continue to drift lower as e-commerce and international (lower gross margin) carry the bulk of the growth, with an additional whack coming from fulfillment expense (see 2nd chart below).

Some of that will be made back on the SG&A side, but it’s difficult to see where additional cost savings will come from that are needed to offset the decline in gross margins. Corporate G&A is as lean as its been during this economic cycle at 6.3% of sale and is headed lower after the 5% workforce reduction announced on the 4Q call. Distribution expenses continue to creep higher, and the company is investing heavily in a new DC at the tail end of an economic cycle. Add on the lower profitability push into international, and it paints a bearish picture for margin health over the near and long term.

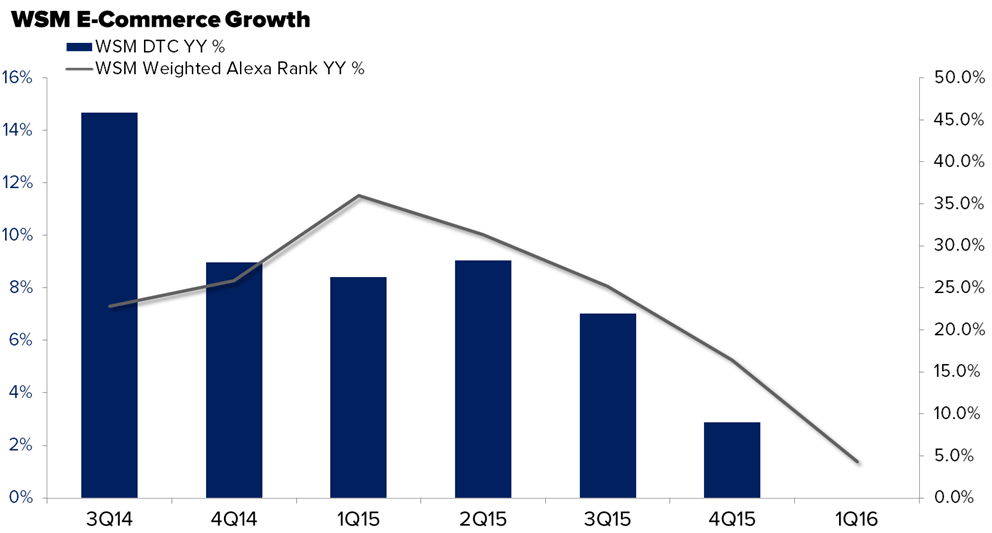

Quarter Considerations: We think the quarter the company is set to report on Wednesday looks fine. The company has never missed a 1st quarter print during this economic cycle and given the short window between guidance and the end of the quarter (just 6 weeks) we think the bar at flat to HSD EPS growth is hittable. Though the one thing that stood out to us is the decelerating e-commerce metrics being posted by the entire portfolio of brands. That’s been evidently clear in the reported DTC growth numbers coming down from 14% in the back half of ’14 to just 3% in 4Q15. Visitation metrics have continued to decelerate through 1Q16.