Growth Bears have been getting paid. this may is no exception.

Here's analysis from Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

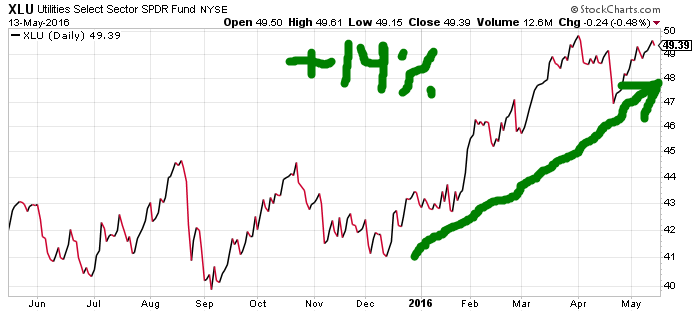

"The Yield Spread smashed to fresh YTD lows last week (10yr minus 2yr = 95bps) keeping the Financials (XLF -4.0% YTD) our fav sector on the short side vs. Utes (XLU +14.1% YTD) our fav on the long side."

(We've been the unabashed bulls on the Long Bond via TLT which is up 9% YTD versus flat for the S&P 500.)

In other words, Utilities (XLU) is the top performing sector year-to-date. We've been recommending it to our subscribers since January.

As growth has continued to slow, there's been an unequivocal bull market in Gold (GLD).

Meawhile, there are plenty of global #GrowthSlowing barometers out there...

Take a look at Italy:

... And China:

Here's the global equity drawdown map:

Click image to enlarge

While global growth slows we're sticking with what's worked all year...

- Utilities (XLU)

- Gold (GLD)

- Long Bonds (TLT)