Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

On The Macro Show Friday, we provided an update on one of our three Q2 Macro Themes: #TheCycle. In summary, credit markets are one of the major beneficiaries (maybe the largest) of the reflation trade since February. While yield spread compression has been a positive for Long Bonds (TLT, ZROZ), a perceived monetary policy shift and a collapse in bond market volatility expectations have been a positive for Junk Bonds (JNK), but we don’t expect it to continue:

Current global macro positioning is squarely behind a continuation in the reflation trade as evidenced by commodity leveraged credit spreads, global macro futures and options positioning, and forward-looking volatility expectations. Below we show global macro futures and options positioning, which shows a market that is leaning long of commodities and short of U.S. dollars (yellow box):

Where do we go from here?

Corporate credit as a % of GDP remains at cycle highs, capital markets activity has dried up significantly, and credit extension is tightening nationwide according the most recent Fed Senior Loan Officer survey:

With growth continuing to slow alongside consensus positioning broadly, downside deflation risk is on the table. As we’ve highlighted on a daily basis, consumption growth and labor market growth peaked in Q1 2015 and both are slowing alongside a continued corporate profits slowdown. This mix:

- Smells like incremental deflation on the margin;

- Is a huge risk for high yield credit (JNK);

Did we mention TLT and ZROZ were up 4.4% and 2.1% respectively last week? Not bad with U.S. #GrowthSlowing.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Zimmer-Biomet (ZBH) presented at the BofA Healthcare Conference this week. Below are some select questions and answers from the presentation. On the one hand, it seems the analyst is asking ZBH to admit growth is going to be better than they are forecasting, both from volume and improving price trends. But the CFO doesn’t bite. We would note that 2017 expectations have been rising in the last couple of months and assume 3% growth year-over-year, exactly at the mid point of management's 2-4% market expectation. On the CJR, they still don’t see it as a negative, but we are fairly convinced it will be.

Q: "Can you give us your best sense as to why things [the market in 1Q16] got a little bit better? Do you think it's sustainable? Just your view on recent volume trends would be very helpful."

A: “Our model continues to reflect a 2% to 4% type growth out over time.”

Q: In 1Q16 “pricing trends were a little bit better”

A: “I'd say that our view on that is, one, that it's probably a temporary phenomenon”

Q: Are these “growth rates … sustainable? Away from price and mix in the U.S., volumes are up 6%, 7%”

A: “Our view of the market continues to be in that low to mid single-digit range”

Q: “CJR, obviously, it's something that people have been talking an awful lot about, but I'll just make it a broad question. The fear for medical device investors is that this program could lead to could have a negative impact on volumes, sort of the cherry-picking aspects of it.”

A: “We do not have a view that says volumes will suffer as a result of CJR”

MCD

To view our analyst's original report on McDonald's click here.

For some perspective on the Macro environment and why we favor companies like McDonald's (MCD), here's an excerpt from the Early Look written by Hedgeye CEO Keith McCullough earlier this week:

"While it should surprise no one who has been on the right side of the US economic, profit, and credit cycle call that the #LateCycle Sectors of the US Economy (Financials, Consumer Discretionary, Tech, Healthcare) are the biggest dogs for the YTD, the pace of the decline in the US Retail (XRT) sub-sector of consumer has caught many off-side this week.

Taking a step back, don’t forget where US Consumers (70% of GDP) were at this time last year:

- US Employment Growth (NFP) was putting in a cycle peak

- US Consumer Confidence was putting in a cycle peak

- US Consumption Growth was putting in a cycle peak

Peak. Peak. #Peak!

And what happens when you start to lap the cycle peak? Well, instead of crappy Baby Boom capacity putting up mediocre (barely positive) same store sales at the peak, they look even crappier on the back side of the cycle."

That's why we like large-cap, low-beta, liquid companies like McDonald's in this tumultuous market environment. Case in point, earlier in the week, MCD hit an all-time high. Since we added the company to Investing Ideas, it is up almost 30%.

Stick with it. Restaurants analyst Howard Penney reiterates his "road to $150" call, implyling more than 15% upside from here.

HBI | TIF | FL

To view our analyst's original report on Hanesbrands click here, here for Tiffany, and here for Foot Locker.

On The Macro Show this morning, Hedgeye Retail analyst Brian McGough gave a sweeping overview of the many earnings misses in the sector this week. In addition to highlighting recent developments at companies on Investing Ideas, like Hanesbrands (HBI), Tiffany (TIF) and Foot Locker (FL), Brian discussed other high-conviction names he covers. Among them, his short Kohl's (KSS) thesis following it's lackluster earnings release and the subsequent -10% tumble shares.

Additional topics of discussion included: why we’ve already seen more retail bankruptcies this year than in any full year in the last six; department store sales versus overall retail sales; and an update on e-commerce traffic.

Below is McGough's full presentation and the live Q&A with subscribers that followed.

Click here to access the associated slides.

NUS

To view our analyst's original report on Nu Skin click here.

Based on 1Q16 numbers, we remain cautious on Nu Skin (NUS) for the following reasons:

- For the second quarter in a row VitaMeal sales were down

- The company is now seeing a decline in distributors across the world

- The increase in revenue guidance was due to the change in FX

- Increased earnings projections, but did not put cohesive story together on how they would achieve these results

- At the same time the company guided down 2Q16 revenue growth from double digit growth on the last earnings call

- Operating margin compression is staggering

- Inventory growth was +3.7% versus sales declining of -8.7%

- On 10/29/15 the company announced an aggressive repurchase authorization and increased it to $500 million. The balance now stands at $427, barely buying any stock given the low price over the past six months.

- The company compared the potential for ageLOC Me to Keurig Coffee Makers (lol)

MDRX

To view our analyst's original report on Allscripts click here. Below is an excerpt from an institutional research note written on Allscripts (MDRX) by Healthcare analysts Tom Tobin and Andrew Freedman.

we remain short mdrx in the position monitor

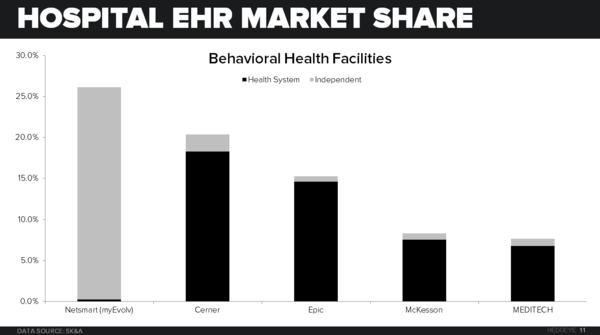

OVERVIEW

We spoke to a former Netsmart Salesperson to get a better understanding of the business and market opportunity, but also to see how great of a deal this really was for Allscripts. We finished the conversation more positive about the quality of Netsmart's products, but more negative on the market opportunity. It also reinforced our initial view that the deal makes little strategic sense given core market overlap and lack of a clear end game.

We also view this as further evidence that Allscripts has all but given up on the ambulatory market, given that the Netsmart myEvolv EHR is technically a competing solution to Allscripts Professional in Behavioral Health. Netsmart has three core products 1) Tier EHR for Substance Abuse 2) myEvolv EHR for Behavioral Health and 3) myAvatar EHR for Behavioral Health w/Inpatient.

key takeaways

- Substance abuse market saturated for Tier EHR; having a tough time selling those systems. Targeting mostly public and small independent facilities that are budget constrained and price sensitive.

- Products too expensive and priced themselves out of the market; high-end of market saturated and had to diversify product portfolio and lower price to move downstream.

- myEvolv was the best selling product, but cannibalized sales from higher price point myAvatar system; myEvolv can perform same functions, but doesn't have inpatient component.

- Netsmart was looking for a buyer for some time; "...already reached the height of their potential" and the reason why they were diversifying the business model, to make themselves more attractive.

- Internal organization problems with a lot of employee turnover and lack of proper training for new sales employees.

- Hit their revenue target for 2015, but missed bookings goal; most of the growth came from private equity funded acquisitions.

- CareManager and CareConnect are vendor agnostic population health and care coordination solutions that compete directly with Allscripts dbMotion in smaller ambulatory facilities.

- Weak revenue cycle offering that they have struggled to sell internally; competes with Allscripts Payerpath.

WAB

To view our analyst's original report on Wabtec click here. Below is an update on Wabtech (WAB) from a recent institutional research note written by Hedgeye Industrials Jay Van Sciver.

Should Have Been Discussed:

Given reports of DoJ concern that the Faiveley merger would reduce the number of passenger-train brake systems manufacturers from three to two, some management commentary was due on the call. It is now increasingly clear that divestitures may be needed for LEY FP & WAB US to close. Faiveley’s Braking & Safety Systems – the area most likely to generate overlap concern as we understand it – is about a quarter of LEY sales. Divestitures would almost certainly undermine at least part of the strategic rationale for the transaction."

LAZ

To view our analyst's original report on Lazard click here. Below is an update from Financials analyst Jonathan Casteleyn.

It official. 2016 has surpassed 2014 as the worst year on record for withdrawn pending M&A transactions. With the Staples and Office Depot transaction nullified by the Department of Justice (DOJ) on Monday, another mid-size $6 billion was lost by the investment banking community. Only four months into the New Year, 2016 will likely finish by a wide margin as the worst period on record for lost M&A.

While the Department of Justice (DOJ) has kicked up its overview recently by blocking Halliburton/Baker Hughes as well, the recent 3rd iteration of the Treasury rules is making it harder for foreign and U.S. companies to redomicile into lower international tax jurisdictions. That's hurt as well. Both an active DOJ and the latest Treasury rules have brought announced M&A activity down by -20% year-over-year in 1Q16 decreasing pending pipelines throughout most of the industry including for our short idea, Lazard (LAZ).

DE

To view our analyst's original report on Deere & Company click here.

No update on Deere & Company (DE) ahead of the company's earnings next week but Hedgeye Industrials analyst Jay Van Sciver reiterates his short call. Stay tuned.