Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

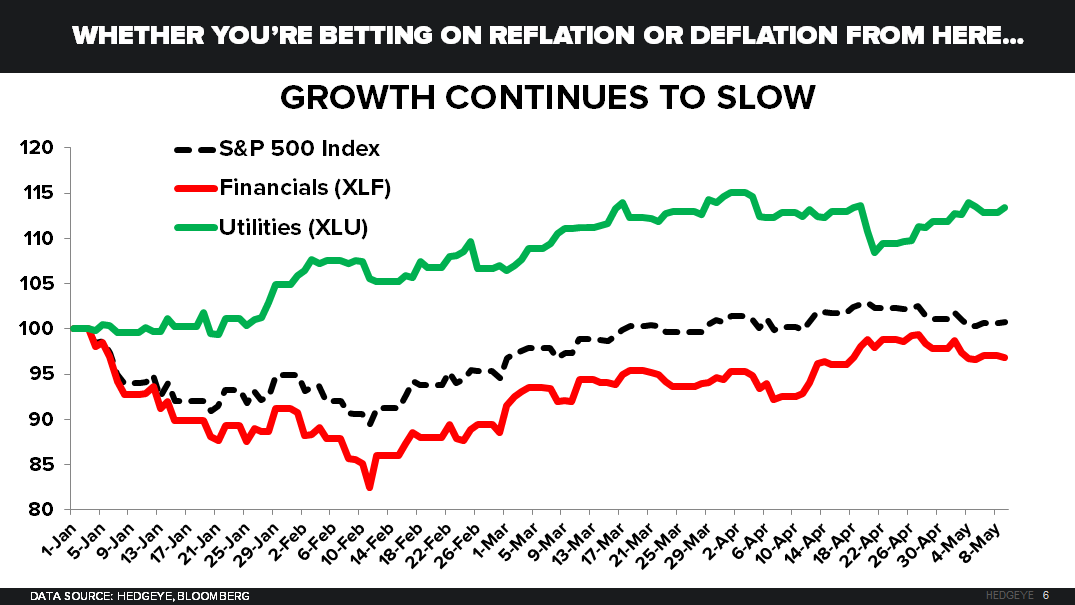

"... Back to REITS, in stark contrast to what they did vs. Utilities when #Deflation dominated in JAN-FEB 2016 (REITS got crushed), they’ve really started to rip higher post the ugly 0.5% GDP report and another rate-of-change slow-down in non-farm payroll (NFP) growth:

- The Vanguard REIT ETF is pulverizing the Financials (XLF -1% in May) and is now +8.5% YTD

- Vs. Utilities (XLU) which continues its impressive, but steady, march higher to +13.5% YTD"