PRA Group (PRAA) reported 1Q 2016 earnings after the close last night. The company missed revenue expectations by -6%, reporting $225 million versus expectations for $240 million, and adjusted EPS of $0.85 fell -11% short of expectations for $0.96. GAAP EPS, meanwhile, was $0.69, 28% below expectations.

Not only did 1Q16 fall short of expectations, but the company is faced with challenges on a number of fronts, which we detail in the note below:

- Across the Board Deterioration — Most of the company’s major metrics are deteriorating year-over-year.

- The Rising Cost of Doing Business — Management pointed out on the conference call that due to new regulation and scrutiny of legal representation in debt collection cases, the amount of documentation PRA’s lawyers require before they will sign off on and pursue litigation is driving up the cost and decreasing the efficiency of legal collections.

- Wishful Thinking — Allowance charges, which management previously dismissed as a non-issue, continue to occur.

- It’s Always Something — GAAP Earnings are consistently worse than the Non-GAAP numbers management wants investors to focus on. The company consistently adjusts earnings upward for “one time” items. The catch is that the adjustment for nonrecurring items consistently reccurs. Interestingly, in the last 9 quarters, not once have Non-GAAP numbers been lower than GAAP numbers.

- Tax Troubles Swept Under the Rug — Although the matter is little discussed, PRAA will stand trial on September 19, 2016 for a $252 million tax payment deficiency plus $91 million in interest. A ruling against PRA could significantly affect the firm’s liquidity

- TCPA — A recent catalyst to PRAA stock’s downward movement was the FCC’s notice of proposed rulemaking (“NPR”) to formally amend the TCPA for restrictions on autodialers. While the FCC proceeded with its exemption of government debt collectors, the NPR did not include a similar provision for non-government debt collectors, as the industry had hoped.

Across the Board Deterioration

- Cash collections of $384 million are -4% lower than 1Q15’s $400 million.

- $225 million in 1Q16 revenue is -8% lower than $245 million in 1Q15.

- Operating expenses of $154 million are up +3% from $149 million in 1Q15.

- Net income was nearly cut in half. 1Q16 came in at $32 million, -45% lower than $58 million in 1Q15.

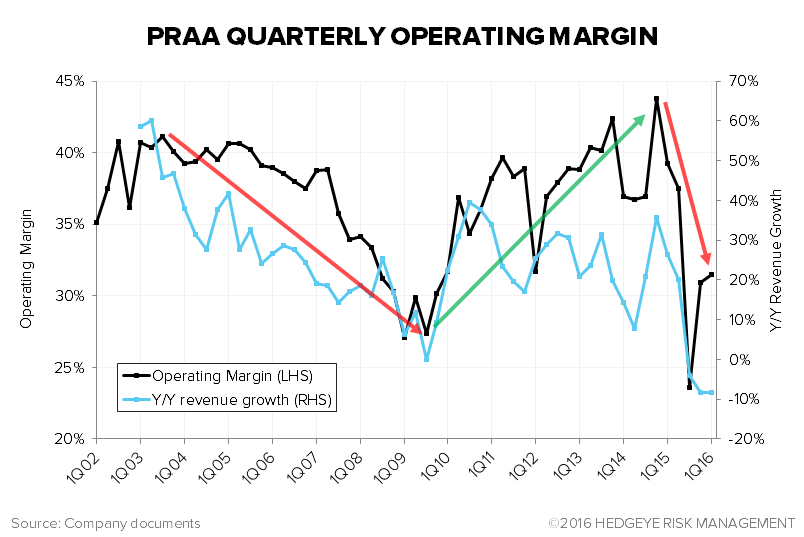

The following chart shows that PRA built up a good deal of operating leverage from 2009 to 2014; its revenues were growing, and its operating margins were expanding. However, now that revenues are falling, the company’s fixed costs are not unwinding so easily. In fact, operating expenses have risen (+$5mn Y/Y), and operating margin has fallen by a massive -770 bps from 39.2% in 1Q15 to 31.5% in 1Q16. We expect this deterioration to continue as limited supply continues to impede the company’s ability to replace liquidations, newer, lower-performing vintages increasingly dominate the portfolio, cash collections continue to fall, and revenue follows suit while fixed costs remain.

Meanwhile, the company continues to lever up. As of 1Q16, PRAA holds $1,817 in net debt, $165 million higher than 4Q15 and $378 million higher than 1Q15. Additionally, debt to equity now sits at 2.09x, up from 2.05x as of 4Q15 and 1.81x as of 1Q15. Bear in mind that most of that equity is from intangible assets (Goodwill).

The Rising Cost of Doing Business

In our February note, Encore Capital (ECPG) | The Pressures Are Both Cyclical and Secular, we pointed out the case of Psaros v. Green Tree which exemplifies the heightened liability placed on law firms litigating to collect debts. Lawyers are now responsible for verifying the legality, accuracy and legitimacy of the debts they attempt to collect on behalf of clients, and they can be sued for damages caused by attempting to collect illegitimate debts. In February, we predicted that this development in the legal collection environment would increase the amount of time collectors spend checking the accuracy of information before proceeding in the legal channel and may also decrease the amount of ECPG’s and PRAA’s collectible debt as legal representation refuses to litigate on debt that the collectors previously thought to be collectible. Sure enough, PRA management directly commented on this issue during the 1Q16 conference call, making the following statement

"The changes that are of note, if there are any, are the lawyers and them desperately wanting to be perfectly comfortable with how these tweaks and changes in practices have affected the paperwork that they're signing off on each and every day, and they're not going to do it until they have perfect clarity and confidence, so the amount of angst around all of that, that's been different."

Additionally:

"Legal collection performance has suffered delays and some loss of inventory related to regulatory and legislative events including state law changes, jurisdictional rule changes, and our consent order, all of which are directing us to obtain different or incremental documents than were required historically."

While management also attempted to ease concerns by pointing out that legal representation is getting to a place where they’re comfortable with the changes PRAA has made, we caution that while the lawyers may now be comfortable and willing to process cases, the elevated legal costs are here to stay. Specifically, management indicated that legal collection costs would be flat sequentially in 2Q16 ($17mn), but would be higher by 20% in the back half of 2016. To put that in context, that works out to +$3.4mn in legal costs/quarter, or roughly 7% of pre-tax income this quarter.

Wishful Thinking

The future is not as bright as management would have us think. PRAA management has argued in recent quarters that, per GAAP, it is being unjustly forced to record allowance charges due to short-term changes in collection patterns while they are increasing longer term collection projections. They claim that the net present value of the upward revision to expected remaining collections (“ERC”) for better performing vintages outweighs the shortfall of the vintages taking the allowances. However, we see this commentary as a distraction from the fact that significant allowances continue to occur. While management may be increasing projections, the shortfalls that force them to book losses continued in 1Q16 to the tune of a $9.9 million revenue hit, roughly in-line with the trend over the last few quarters.

Furthermore, management highlighted a $7 million Italian portfolio that it is performing so poorly that it is not even booking revenue anymore. In other words, any collections that the company makes on that portfolio incur a cost to collect, reducing earnings, but accruing no revenue. This is not a good sign for the overall health of the debt collection business.

It’s Always Something

To make a quick point about the usefulness of the information that PRA’s management feeds investors, there always seems to be different “one-time” items that they use to adjust earnings. The problem is that when one-time occurrences occur every time, they’re not so “one-timeish”, are they? Our point is that PRAA earnings truly are lower than what management attempts to dangle in front of investors. In fact, since 1Q14, one-time adjustments have averaged $7 million per quarter. Even excluding 3Q15, when PRAA booked most of its CFPB expense, the average is $4.7 million. To put this in better perspective, add-backs of one-time items averaged just six cents per quarter from 1Q14 through 2Q15, but in the last three quarters they've averaged $0.32/quarter. The last 9 months have seen GAAP earnings of $1.91, while non-GAAP earnings have been $2.87 (50% higher!). We think the buyside and sell-side may be slowly waking up to the fact that GAAP numbers are the better gauge of how PRA is performing. It's also remarkable how in the last 9 quarters, not once have Non-GAAP earnings been lower than GAAP earnings.

Tax Trouble Swept Under the Rug

Although it’s seldom discussed, hidden away in the 10-k is a disclosure that the IRS reviewed the company’s tax revenue recognition methods and determined that PRA is alleged to have shorted the tax man by $252 million. Also, as of 12/31/15, that tax bill carried an estimated $91 million in interest. PRA is set to stand trial for this tax liability on September 19, 2016. If it loses the case, the $300+ million tax charge would likely significantly affect PRAA’s liquidity.

TCPA

Since July 2015, the FCC’s ruling to ban the use of autodialers to contact debtors on their cell phones has been a hot issue. The Association of Credit and Collection Professionals appealed the FCC’s ruling shortly after it was issued. However, on January 15, 2016 the FCC released a defense of its original decision and showed no sign of budging. Even still, there remained hope that the FCC’s formal notice of proposed rulemaking (“NPR”) might provide some exemptions to non-government debt collectors. However, last Friday, May 6, the FCC released its NPR without guiding towards such provisions. As it stands, private debt collectors will continue to experience higher cost to collect due to the decreased efficiency of manually dialing cell phones to make collection calls.

Plenty of Downside

Given the numerous aforementioned headwinds, we believe this quarter’s broad deterioration in PRAA’s metrics is only the beginning of the company’s downturn. We continue to see significant downside to PRAA’s stock price.

One Final Note

We normally analyze PRAs' individual vintages to track performance and look for any changes in quality, but we need the 10-Q to do this. Once the Q is out, we'll provide an update with the latest look at vintage performance.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT