Yes, but not a happy one. It’s mostly about managing decline.

Editor's Note: In this complimentary edition of About Everything below, Hedgeye Demography Sector Head Neil Howe writes about why the cable and satellite TV industry's glory days are behind it. In it, Howe dissects the underlying demographic drivers and explains the broader implications for investors.

***After reading the written piece, join Neil LIVE on HedgeyeTV (see video player below) at 2:30pm ET Tuesday to discuss. It's free.

WHAT’S HAPPENING?

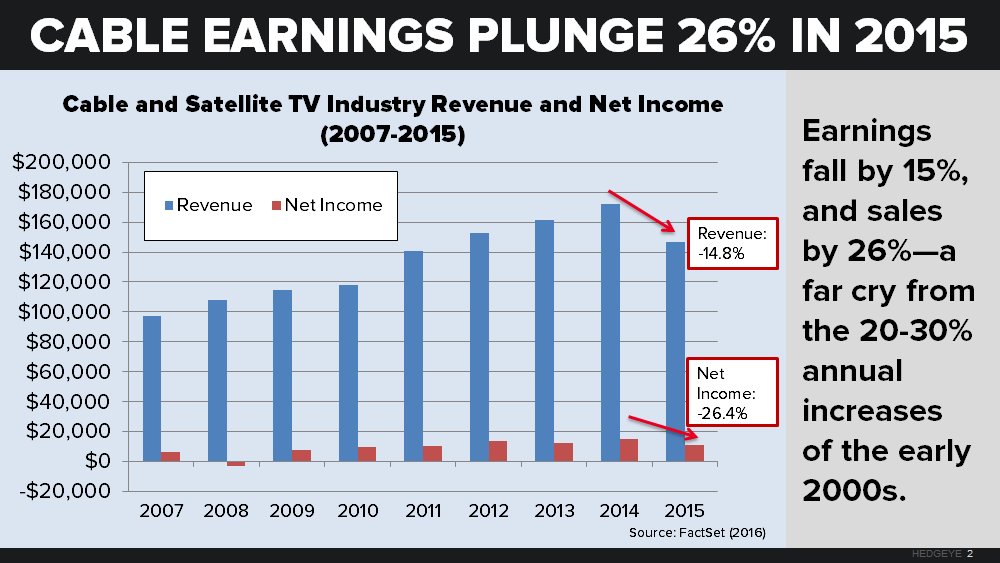

The cable and satellite TV industry is ailing. Gone are the glory days of the early 2000s, when company revenues soared 20 to 30 percent annually.

Last year, industry revenues fell 15 percent. Net incomes among giants like Comcast, Time Warner Cable (TWC), DirecTV, and Dish also tanked—while smaller players like Charter Communications and Liberty Global actually saw theirs turn negative.

You wouldn’t know the severity of the situation by looking at the market. Though share prices of most cable companies took a dive last year, many of these stocks have recovered and are now doing better than ever. Comcast (also home of NBCUniversal) has all but regained its peak 2015 value, while Verizon and AT&T continue to post new highs (no thanks to their cable businesses).

While industry P/E ratios are a far cry of what they were a decade ago, they’re still just marginally beneath the S&P 500 at large. So what would you rather bet on: the entire American economy or a moribund industry with no easy path to profitability? OK, “neither” is an acceptable answer. But “number two” is certainly the wrong answer.

WHY IT’S HAPPENING: DRIVERS

Cord-cutting. The top nine cable companies lost about 340,000 video subscribers in 2015. The year before, the industry at large lost 1.2 million subscribers. By comparison, Netflix added more than 1.5 million subscribers last quarter alone. Thanks to Netflix and the myriad other cheap (or free) ways consumers can get content today, you no longer need a cable subscription to see your favorite shows.

Even when cable firms do gain subscribers, they’re often feasting on the scraps of shrinking satellite providers. (Dish and DirecTV lost over 135,000 subscribers each last year.)

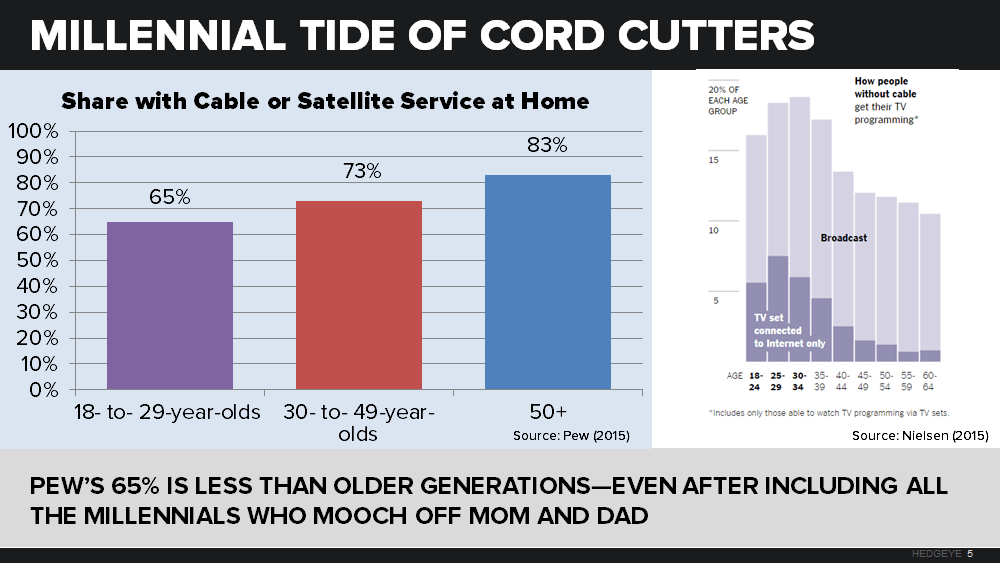

Generational change. Millennials are by far the largest group of cord-cutters and cord-nevers. Whether they can’t afford it or they’re content to find entertainment online, Millennials consider cable an option, not a necessity. In 2015, 19 percent of 18- to- 29-year-olds cut their cable or satellite subscription. Another 16 percent never had cable. (And plenty still live with parents who foot the bill.)

Instead of plunking down on a cable subscription, Millennials would just as soon use an antenna (remember those?) to find broadcast shows. Or they cut out broadcast TV altogether and go broadband-only.

This trend will continue to give cable companies a major headache as Millennials take their new viewing habits with them up the age ladder. Forecasting firm eMarketer predicts that by 2018, one in five households will not subscribe to pay-TV.

Increased regulatory scrutiny. In 2015, just three companies—Comcast, TWC, and Charter—accounted for 77 percent of all cable subscribers. Not only is cable concentrated at the national level, but many of these companies enjoy steel-trap regional monopolies. In many cities, the typical household can only subscribe to one provider. Most of the rest can choose between two duopolists (usually a cable company and a telecom).

From monopoly comes pricing power, and from pricing power comes a boost in profit margins. Yet this too may be ending. The antitrust regulators are catching on. The TWC and Comcast merger was called off—thanks in part to promises by federal regulators to fight the deal. Charter’s newly minted acquisition of TWC includes mandates that are stricter than current industry regulations. Stricter FTC oversight may ultimately deter “defensive” mergers by small cable firms in steep decline. This would further cloud the industry’s outlook.

Even the set-top box is fair game for regulators. Cable giants earn $20 billion annually from forcing their hardware into the hands of subscribers—at least until the FCC drops the hammer and opens up this niche market to third parties.

DO THE CABLE COMPANIES HAVE A WAY OUT?

Broadband. In the absence of a robust pay-TV customer base, the top cable companies are gunning for new broadband revenue. But this transition could be stymied by net neutrality legislation. The FCC wants to regulate broadband like a common carrier—which would prevent cable companies from raising broadband prices to make up for cable losses.

Sure, the industry would get a boost if the American public rapidly upgraded to much higher bandwidth video (like 4K video or perhaps new VR consoles). In time, the FCC would have to allow firms to invest in a whole new broadband infrastructure. But don’t hold your breath. There’s little evidence to date that the public wants to pay for this extra “service,” any more than it wanted to pay for 3D TV. (Gee, what happened to that?)

“Skinny” bundles. Last year, Verizon and Comcast introduced pared-down, cheaper channel bundles—but these options reduce revenue and earnings. Cable companies have no real incentive to offer pay-per-channel plans: There’s no way they would be better off with less content and less revenue in a bundle-less world.

New services. The big cable firms are reaching far beyond mere TV packages. They are dreaming up new products they hope will entice more consumers to stick around. Exhibit A: AT&T, Comcast, TWC and Verizon all offer home security systems, which cost less than traditional home security services when bundled. But long-term, do you think they can possibly compete with cutting-edge IP-based services like Nest? There’s a reason why this software revolution is called the “Internet of Things”: It’s all on the INTERNET.

Comcast and Cablevision are also investing in ways to allow customers to stream content through their set-top boxes. But again, this strategy risks rendering the cable subscription itself obsolete.

Live TV. Can’t-miss live events—like NFL games or local news or presidential debates—may be the last true bastion of cable profitability. It’s easier to maintain an exclusive price for content that has to be watched in real time. Nobody hosts a Super Bowl Party the day after the Super Bowl.

To be sure, generational forces could help live programming. Millennials’ penchant for second-screen viewing gives the cable industry more opportunities to bring back the linear TV experience. Cable could turn the tide by hosting online communities centered on live programs that are available only through cable.

But how long will it be until major sports leagues take a page out of HBO’s playbook and bring their content directly to the fans? Though cable companies hope the answer is “never,” the seeds have already been planted (see: NBA Live, MLB Live, and NHL.tv).

Content aggregation. There may be room enough for one cable company to win out. How? By using the research and consumer data at its disposal to guide consumers through an increasingly fragmented landscape of content. A savvy, streamlined firm (perhaps Comcast?) could have a chance to survive the impending dearth of cable subscribers. So I’ll allow that one healthy survivor may emerge. But only after a prolonged and bloody gladiatorial contest has come to an end.

TAKEAWAYS

- Broad band, cord-cutting, IP-based software, and stricter antitrust enforcement are combining to throttle cable firms. Avoid being long in these firms, and look for opportunities to short those having no line of business (like telecom or content) other than cable.

- Be skeptical when you hear CEOs and analysts say they have a magic formula to stop the bleeding—like doubling down on broadband, repackaging content, or offering new products. There’s no easy fix for a dying paradigm.