Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

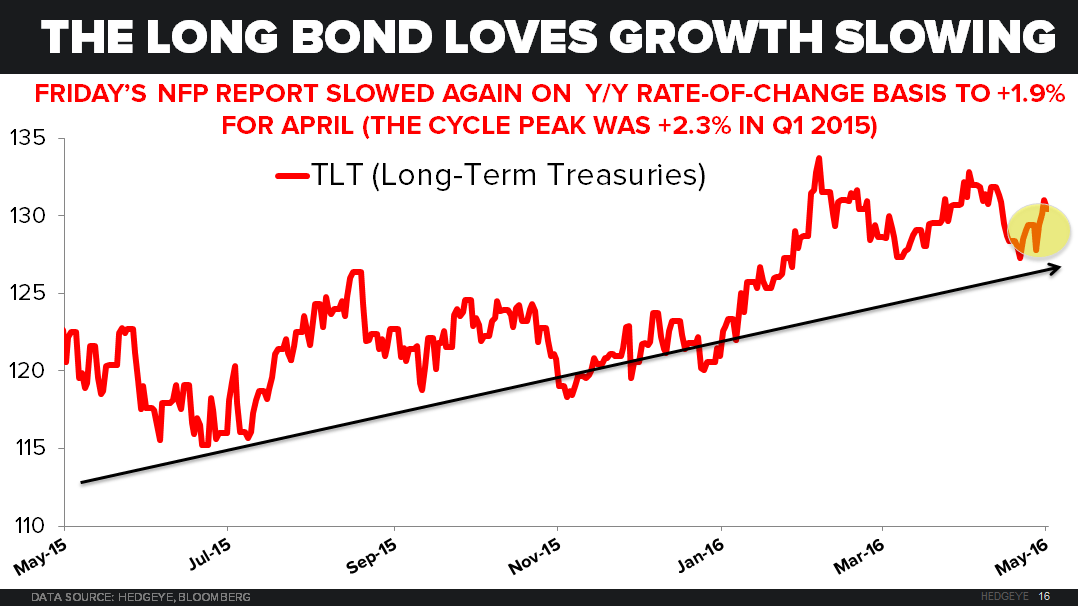

"... With another rate-of-change #slowing in non-farm payroll (NFP) growth for the month of April at +1.9% (vs. #TheCycle peak of +2.3% in Q1 of 2015), the big money in macro that was made last week was right where it’s been made all year long:

- Long Bond (TLT) up another +2.1% last week to +8.2% YTD

- Utilities (XLU) up another +0.8% last week to +12.8% YTD

- Gold up another +0.3% last week to +21.9% YTD"