Below are our analysts’ new updates on our fourteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Note that we removed General Mills (GIS) from the long side of Investing Ideas. Please see below Hedgeye CEO Keith McCullough's refreshed levels for our high-conviction Investing Ideas.

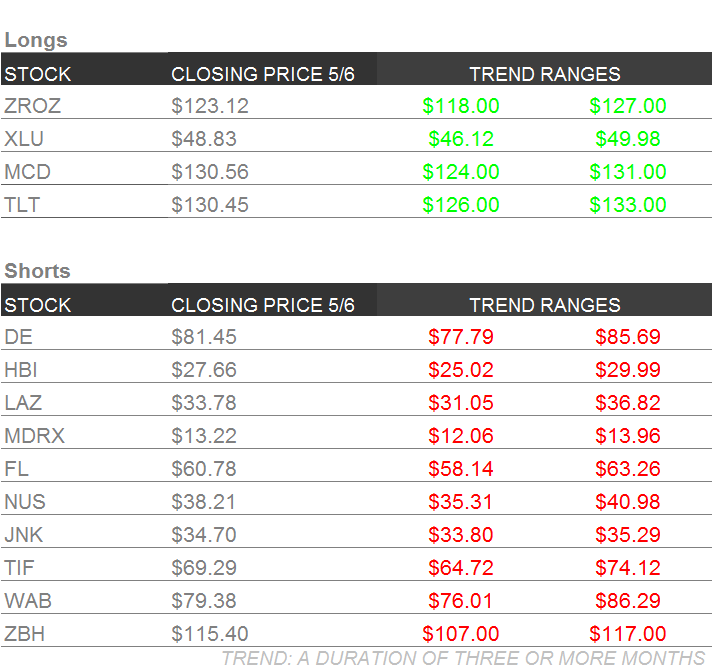

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

As our Growth, Inflation, Policy model is oscillating between tracking in quad 3 and 4 for the second quarter, we’re sticking to core positions that perform well when growth is slowing and the yield curve is flattening:

- QUAD3: Growth Slowing, Inflation Accelerating

- QUAD4: Growth Slowing, Inflation Decelerating

The model signals that growth is slowing either way, and we expect a continuation of bond market discounting late cycle, growth-slowing. An allocation to Long Bonds (TLT, ZROZ) and Utilities (XLU) keeps investors out of the way of guessing which way assets levered to inflation will move next. The yield spread 10s-2s moved this week like it is headed toward taking out YTD lows. To be clear, this is NOT an indication that growth is back.

How do we know growth is slowing (ex. being validated by Treasury bond market and XLU outperformance)?

We look at every relevant data series on a rate-of-change basis to analyze a sine curve. Taking a look at our analysis of Y/Y Non-Farm Payroll growth, a clear cyclical picture develops. Mainstream media and other sell-side sources who talk about guessing the sequential NFP number are pursuing a fool’s errand (a confidence interval that is very wide) in terms of positioning into a number. We call this “open the envelope risk."

Rather, constructing a sine curve of the rate of change in NFP growth gives us a clear visual that employment growth peaked (in Feb. 2015), and it’s not recapturing that growth rate in this cycle. So whatever the sequential number is M/M, we know where this series is headed. And, when considered with every other relevant data series, we have a clear empirical view on where the U.S. economy is positioned in the economic cycle.

MCD

To view our analyst's original report on McDonald's click here.

McDonald's (MCD) reported 1Q16 earnings on April 22nd that beat consensus estimates. The quarter serves as continued proof that the comeback story is in full swing.

The big question is where MCD is headed in terms of their national value platform. They had the McPick 2 for $2, then 2 for $5, now they have shifted to the monopoly promotion. McDonalds regaining a consistent value message is key to their success, and they know this. Additionally, we have another two quarters of tailwind from All Day Breakfast before we begin to lap it.

McDonalds’ recovery has been nothing short of extraordinary and has been a great source of alpha for all of its holders. We continue to like the name on the LONG side given the strong fundamental turnaround and the style factors that we love, big cap, low beta and liquidity.

WAB

To view our analyst's original report on Wabtec click here.

Wabtech's (WAB) 1Q 16 earnings release and call were notable because of what they did not contain: a clear explanation the favorable decremental margin (materials are likely to prove mean reverting) and a disclosure that Faiveley was under significant scrutiny by antitrust regulators. Given those omissions, we are interested to hear more about the Siemens PTC suit.

A failure to be forthcoming is deceptive, in our view. We have met with several larger longs in WAB that place significant faith in this management team, and we wonder if those holders noticed those omissions. We continue to see WAB as a promising short, and expect 2016 EPS ex-Faiveley below $4/share as the company’s core freight market enters a multi-year downturn.

HBI

To view our analyst's original report on Hanesbrands click here.

Hanesbrands' (HBI) recent actions give us even greater confidence in our short call.

The recent acquisitions at HBI bothers us. At this point late in the cycle, the deals are getting more and more expensive. HBI bought DB Apparel for 7.5x in 2014, Knights Apparel for 8x in 2015, and now both Champion Europe and Pacific Brands cost 10x EBITDA (Pacific Brands was actually 10x on the company's adjusted NTM number, using the proper measure its actually closer to 12x). Basically, though still expensive, HBI is trading at a 20% lower multiple, but it’s deal multiples are 20% higher. Why?

Also, if HBI was interested in buying Pacific, why didn’t they do it a year ago at half the price? That’s kind of a rhetorical question. It is a public company … so it’s not like it ‘wasn’t for sale,’ and it’s also not like ‘HBI wasn’t a buyer.’ Just strange to pay nearly $400mm more for the same asset.

When a company behaves this badly, no one wins.

NUS

To view our analyst's original report on Nu Skin click here.

As we reported last week Nu Skin (NUS) reported earnings that beat expectations (which were deflated by prior guidance). An important thing to note is the YoY decline in VitaMeal sales, which fell -8% YoY. We are under the impression that a big driver of distributor growth is provided by contributing to charity. As VitaMeal sales have eroded so have the number of sales leaders.

We continue to like NUS on the SHORT side, as the company boasts inconsequential market share in the global personal care landscape, and operates a business model that will likely not be sustainable in the long-run.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

Zimmer-Biomet (ZBH) is now priced for the recovery, with the EV/EBITDA multiple moving back over 10X after touching 8.75X, a multi-year low, in February 2016. ZBH had a good quarter in the US, although we think the leap day, a mild winter, and weak flu season all played positive rolls. The weak flu season helps because patient surgeries are often delayed if a patient is sick and running a fever, or can’t get to the OR because of deep snow. An extra day of surgeries helps as well.

As the multiple has recovered, however, estimates have remained consistent. We still believe there are far more risks to the stock from here compared to the upside fundamentally. The price certainly disagrees with us, and we hate to be as wrong on the price as we have been recently. But we still like the short.

We’ll keep digging, talking to surgeons and our policy team, and watching our #ACATaper data. On the ACA, the employment update for healthcare showed that trends continue to slow for healthcare. We think the pent-up demand created by millions of newly insured (and a 6.2-fold increase in knee replacement surgery) is beginning to unwind to the downside.

MDRX

To view our analyst's original report on Allscripts click here. Below is an research note on Allscripts (MDRX) written by our Healthcare analysts Tom Tobin and Andrew Freedman.

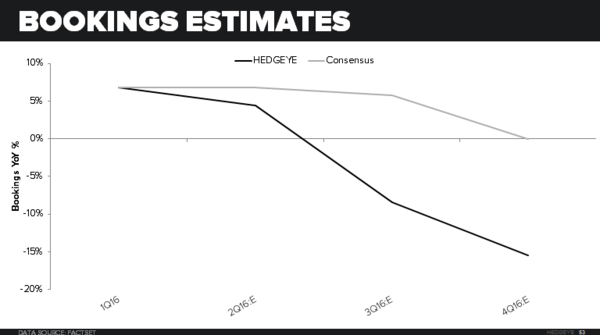

MDRX | IT ONLY GETS WORSE FROM HERE...

inline sales and eps; software delivery bookings plunge -25.7%

Allscripts reported a lackluster 1Q16 with sales of $345.6 million and Non-GAAP EPS of $0.13 coming inline with consensus and our expectations. Recurring software delivery, support and maintenance revenue declined -1.5% YoY, while recurring managed services grew +22.3% YoY. Total bookings were up +7% YoY to $252 million, but missed consensus estimates of $257 million. While we were expecting Software Delivery bookings to slow YoY, we were surprised by the -25.7% YoY decline. To provide "context", this was the weakest Software Delivery bookings quarter since 1Q13, and the third consecutive quarter where the 2-year average growth rate has been negative. We also view this as confirmation that the incremental revenue from the University Hospitals contract expansion was mostly maintenance, and therefore had little impact on reported bookings. Allscripts also did not close any new Sunrise deals in 1Q16 despite positive reported deal flow at competing vendors, which supports our negative view of Allscripts weak position in the market.

growing client services at the cost of profitability

Offsetting the -25.7% decline in software delivery, Allscripts reported a large mix shift toward Client Services bookings in 1Q16, which were up +61.4% YoY and represents a continuation of a trend that began in 3Q15. While we acknowledge that Allscripts has been able to execute on their strategy to cross-sell hosting and outsourcing solutions to current customers, we don't view this as a sustainable growth alternative to new system software sales. We expect the downside of this strategy to become more evident as we head into the 2H16 and begin to run up against the large hosting and outsourcing agreements Allscripts signed with some of their largest customers. Additionally, it is important to note that Client Services (34% of sales; 14.8% GM 1Q16) at full potential (20% GM) has only a third of the gross margin of software and maintenance (66% of sales; 63% GM 1Q16). 2H16 and 2017 profitability will be challenged as the mix shift results in lower gross margins while at the same time Allscripts anniversaries the cost cutting and restructuring that occurred in 2015.

another year, another reclassifcation...

Allscripts management has made reclassification routine, and 1Q16 was no exception, further reducing transparency for investors. With the addition of the recent Netsmart joint venture, investors will have an increasingly difficult time understanding underlying business trends. After pulling Maintenance backlog last year, management has decided to no longer break out 'Support and Maintenance' and 'System Sales' revenue separately. It was only a year ago that management thought that these were the right metrics to report. Instead, they now believe investors need even less transparency and are grouping everything into two buckets 1) Recurring 2) Non-recurring. Needless to say this is a red flag as we no longer have transparency into support and maintenance, which provided the cleanest read on attrition and accounted for 33% of 2015 revenue and approximately 25% of total backlog.

estimates still too high

We are reducing our estimates for the upcoming quarters to further reflect our expectation for lower software delivery bookings and a faster than anticipated sales mix-shift toward client services. This shift will put increasingly negative pressure on gross margin in 2017. We also increased our R&D expense estimate to reflect additional costs associated with having to bring three EHR solutions in compliance with the new MIPS quality reporting standards by 2017. With respect to bookings, we continue to believe that the consensus estimate for +2.5% bookings growth in 2H16 is too high as the prior year contains deals that we don't view as repeatable. We are modeling 2H16 bookings growth of -12.4% YoY. Note that our estimates do not reflect any impact from Netsmart.

TIF

To view our analyst's original report on Tiffany click here.

During its analyst day, Tiffany (TIF) announced a partnership with Net-a-Porter which would allow the online retailer to sell select Tiffany designs for limited periods of time. Those designs hit the website about a week and a half ago.

We find this partnership to be interesting for several reasons, but ultimately it seems to be a move of desperation on the side of TIF.

- At face value, the partnership makes a lot of sense. Net-A-Porter, from a demographics standpoint, skews younger than TIF and also high income, perhaps bringing the brand to the younger affluent consumer that TIF needs for future growth.

- Despite claiming to have "best in class digital" during the analyst day, Tiffany's online penetration hasn't grown in about 10 years, sitting at 6%. It seems the company is using this partnership as a way to accelerate growth in the online channel (albeit with a lower realized revenue and gross margin), which it has failed to do on its own.

- The timing of the deal is interesting, given that our trackers show 1Q traffic trends have looked very negative at both tiffany.com and net-a-porter.com (charts below). Perhaps both sides felt the need to make a move in hopes of reversing the weak sales trends.

LAZ

To view our analyst's original report on Lazard click here. Below is an analyst from Financials analyst Jonathan Casteleyn.

No update on Lazard (LAZ) this week but Financials analyst Jonathan Castelyn reiterates his short call. Below are a few key takeaways from Castelyn's original stock report:

- Our main contention is that Wall Street is ignoring warnings signs of a high-water mark in M&A, including rising private equity participation levels and also all-time highs in consideration value.

- Street estimates are unbelievably complacent in our view with numbers that completely ignore the hyper-cyclicality of the advisory and asset management businesses.

- For 2016, we think the company will earn under $3 in earnings, some -20% below the Street. Our base case estimate is the stock is worth $30 per share on 10x our $3 EPS estimate for '16.

- Meanwhile, our bear case, if M&A activity rolls over by -20%, is a $22 stock at $2.20 in earnings at a 10x multiple.

FL

To view our analyst's original report on Foot Locker click here.

The first of the athletic retailers reported earnings last night, with the Big Five printing a comp and EPS miss. Sales trends are increasingly negative. After reporting high single digits comps in January, trends slowed to low single digit comps through January and February, and finished 1Q at -1.9%. Comps in 2Q to date are down low to mid single digits.

Foot Locker (FL) points to the highly promotional environment as the driver of comp weakness. Also, in the face of two recent athletic retail bankruptcies (The Sports Authority & Sport Chalet), the company noted that 60% of their stores overlap with these retailers. Investors in the likes of DKS, BGFV, HIBB, and FL are expecting a sales lift from the reduction of competition. But the Big 5 result indicates that there will be more pain before any gain.

So, for FL, it looks doubtful that any TSA bankruptcy benefit will hit in 1Q. We would argue that the upside is minimal. Sales started slowing at BGFV and FL before the bankruptcy liquidation commenced (TSA closures are running March-May). And as it relates to FL, there is only a very small portion of TSA revenue that FL could steal, given the 30% footwear penetration rate at TSA, the closing of only ~30% of the stores, and 30% shopper overlap. That puts the total revenue upside for FL around $85mm, or just over 1% growth assuming they take all of the relevant revenue, which competitors won’t allow.

DE

We added Deere & Company (DE) to the short side of Investing Ideas. Click here to read our Industrials analyst Jay Van Sciver's full stock report.