It's been an ugly earnings season.

Some important callouts this morning:

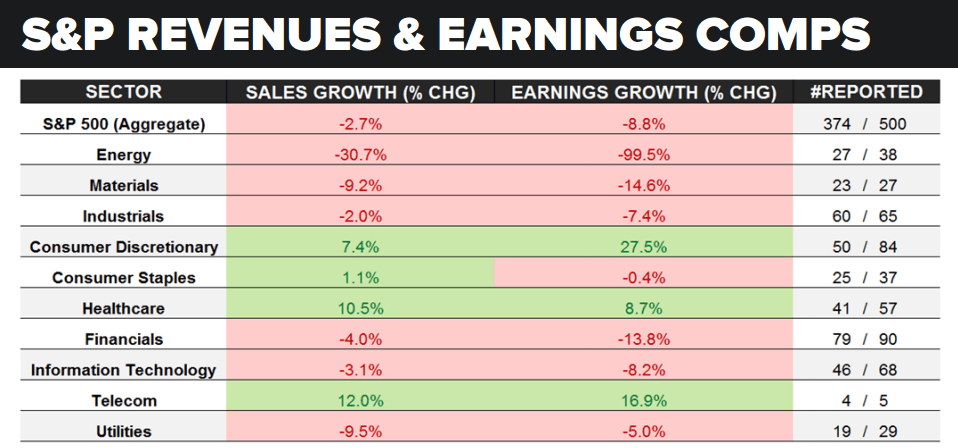

- A grand total of 374 of 500 S&P 500 companies have reported Q1 2016 results, with aggregate sales and earnings growth down -2.7% and -8.8% respectively;

- So far... 7 of 10 sectors have reported negative earnings growth;

- Earnings growth for our favorite sector short call, Financials (XLF), are down -13.8% with sales -4.0%;

- Energy (XLE) earnings growth crushed, down -99.5%, with -30.7% sales growth;

Here's what it looks like right now.