Below is analysis via Hedgeye CEO Keith McCullough in a note sent to subscribers earlier this morning:

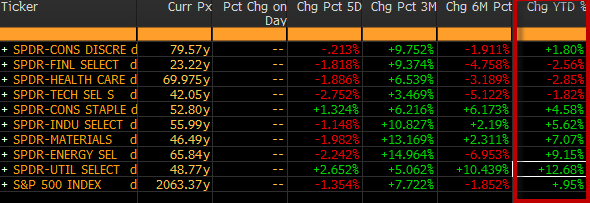

"I’m done apologizing for adding Nasdaq to our bearish US Growth Equity call on March 31; it was a battle, but month-over-month the Composite Index is -3.1% (SP500 is -0.2%, not up, so chart chasers are having some issues on the long side here); Big Cap Tech in a dead heat with Financial (XLF) and Healthcare (XLV) for worst S&P Sector YTD."

Notice the dead heat for last place in the year-to-date performance scorecard below (i.e. XLF, XLV and XLK):