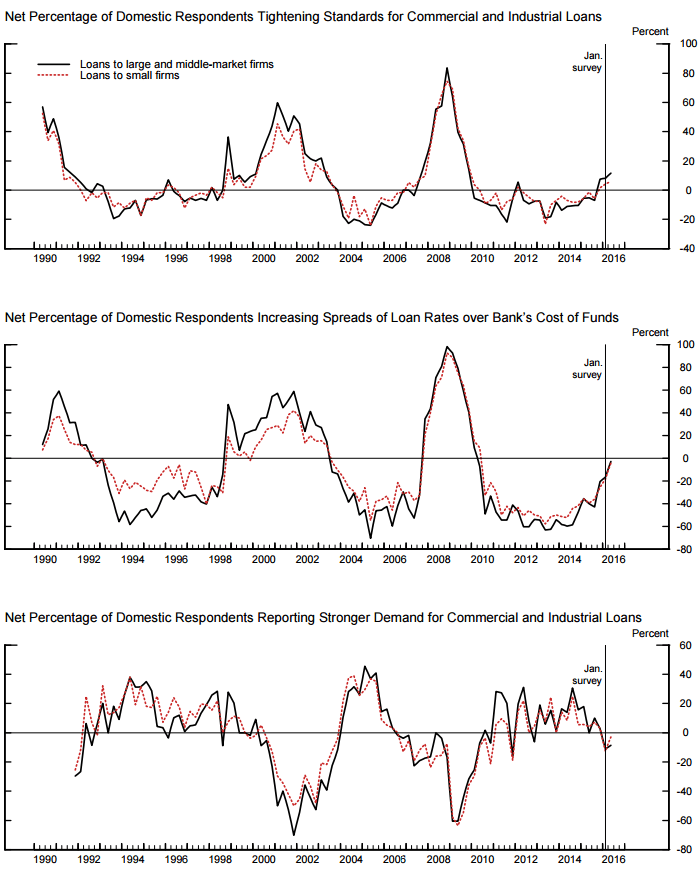

The Fed Senior Loan officer survey for 2Q16 released today showed a further tightening in corporate & commercial credit.

Specifically, a net percentage of banks tightened C&I lending standards for the third quarter in a row (11.6% in 2Q, up from 8.2% in 1Q) while C&I loan demand was negative (-8.7% net) for a 2nd consecutive quarter.

Dynamics were similar on the CRE side as the net percentage of domestic respondents tightening standards for Commercial Real Estate loans increased across all loan categories while the percentage of firms reporting increased demand for CRE loans was largely flat sequentially

From a macro perspective, there are a few notable takeaways:

- Credit is Causal: It’s both virtuous and vicious and just as it can serve to jumpstart or amplify a virtuous cycle on the upside, it can similarly serve to catalyze a negative self-reinforcing downcycle. As is the case currently, banks tightening the screws, increasing the price of money or reporting reduced demand for money all portend a slowing of economic activity.

- Spill Over? This quarter's survey included special questions about lending to firms in the oil and natural gas drilling or extraction sector. Notably, direct exposure to the sector is relatively small with the majority of domestic banks indicating that such lending accounts for less than 5 percent of their outstanding C&I loans. However, as the survey notes, “banks indicated a spillover from the energy sector onto credit quality of loans made to businesses and households located in energy-sector-dependent regions. In particular, a significant net fraction of banks reported that credit quality deteriorated for both auto loans and non-energy-sector C&I loans somewhat over the past year. Furthermore, moderate fractions of banks indicated that CRE loans, consumer credit card loans, and consumer loans other than credit card and auto loans made to businesses and households in these regions also deteriorated somewhat over the past year.”

- Recessionary Harbinger: Historically, a broad and sustained tightening of credit has been a harbinger of recession. As can be seen in the C&I and CRE Survey Charts below the prevailing trend has clearly been one of tighter credit and declining/less-good demand. Concentrated tightening in the commercial sector suggests capex and nonresidential fixed investment will remain underwhelming and a headwind to headline growth, at the least. We expect declining corporate profitability and spending to carry negative flow through to consumer credit trends on a lag.

- The Credit Cycle: The credit cycle is, indeed, a cycle that has, historically, played itself out in autocorrelated fashion in both directions. Our bank credit cycle indicator, which represents an equal weighted composite of the key credit metrics in the Loan Officer Survey, went positive (i.e. a net tightening) for the 1st time this cycle in 2Q.

In short, the Senior Loan Officer data continues to suggest the credit cycle is past peak and in phase with the labor, income, confidence and profit cycles, all of which are traversing their downslopes at present.

Christian B. Drake

@HedgeyeUSA