Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we removed CME Group (CME) from the long side and added Deere & Company (DE) to the short side of Investing Ideas. Industrials Sector head Jay Van Sciver will send out a full stock report on Deere & Company next week. We will send CEO Keith McCullough’s updated levels for each ticker in a separate email.

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

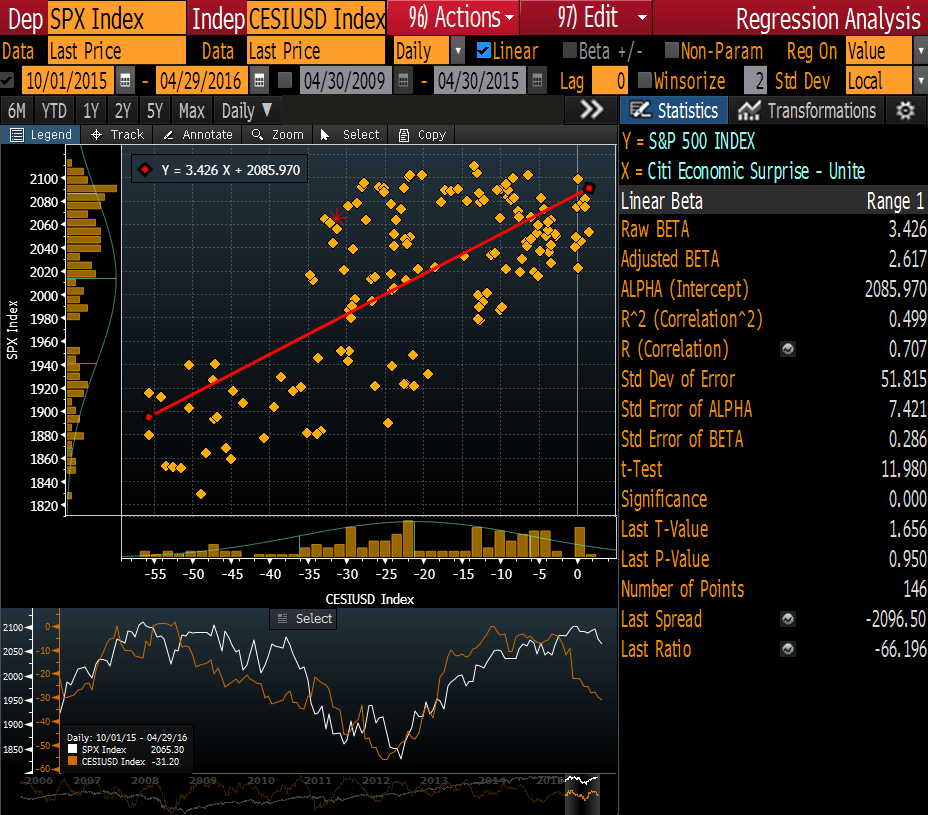

As we penned in a 4/21 research note titled, “Important Thoughts On Market Structure and Sentiment”:

“Since the late-September lows, the S&P 500 has held a reasonably tight positive 0.75 correlation with the Citi U.S. Economic Surprise Index, which itself has rallied hard off its early-February lows as U.S. economic data stabilized in rate-of-change terms and perpetuated a waning of recession fears.

Now, a topping process in the latter index appears to have gotten underway over the past two weeks, as most recently highlighted by big misses in this morning's Philly Fed and Chicago NAI surveys. While our process generally underweights survey data – particularly one-off regional surveys – in lieu of doing the actual rate-of-change calculus on relevant “C” + “I” + “G” + “NX” metrics, we reiterate our view that economic deterioration from here is itself the catalyst for the stock market to reverse course a meaningful manner.

Simply put, because macro consensus doesn’t have our economic outlook, we believe domestic economic data will start to miss by wide margin again as it did in the early part of this year. It’s also worth noting that economist consensus always has a natural upward-sloping bias to their growth estimates, which creates additional downside surprise risk to the extent we're right on where the data is headed over the next couple of quarters.”

Source: Bloomberg L.P.

With the preponderance of key high-frequency data showing sequentially deteriorating economic momentum over the past week and the equity market (SPX) experiencing its largest weekly decline since early-February, that appears to have been a prescient call – for now at least. As always, the confluence of time and price will determine the ultimate winners and losers from here. The key highlights were Wednesday’s MAR Pending Home Sales bomb, Thursday’s paltry Q1 GDP report and Friday’s MAR Consumer Spending data.

The slowdowns highlighted above were in the context of reports earlier in the week that showed New Home Sales and New Orders growth for both Durable Capital Goods all decelerating in MAR.

In the interest of our goal to objective report the data, there were a couple of good economic releases over the previous week – namely the preliminary Markit Services and Composite PMI readings for the month of April. That said, however, the trend of deceleration from the late-2014 highs remains firmly intact.

The good thing about each of our active Macro positions (i.e. TLT, ZROZ, XLU and JNK) is that each of them typically works on an absolute return basis when growth slows:

And as we penned in a 4/28 research note titled, “Finally, Some Differentiated Thoughts on Q1 GDP…”:

“Despite today's weak print, U.S. GDP growth is very unlikely to rebound here in Q2. Don't get caught up in residual seasonality hopium.

… All told, the confluence of steepening base effects (to cycle-highs I might add) amid the trending deterioration in economic momentum support our GIP Model forecast of a continued deceleration in the YoY growth rate of real GDP from +1.9% in 1Q16 to +1% in 2Q16E. The latter growth rate translates to +0.3% on a QoQ SAAR basis, which is up from our previous forecast of -0.5% (a lower base rate implies a smaller delta to get to the same numbers, all things being equal).

Assuming Q1 isn’t revised in any material way, our forecast for 1H16E is represents the slowest pace of domestic economic growth on a multi-quarter basis since 2H12. Any downside surprises from there will surely translate to renewed recession fears.”

Giddy up for continued #GrowthSlowing!

MDRX

To view our analyst's original report on Allscripts click here.

It was announced last week that Centra Health selected Cerner for an Enterprise wide EHR and Population Health system across the inpatient, ambulatory and post-acute care settings. Driving the replacement decision was McKesson's sunset of their Horizon EHR, which was installed in 4 hospitals (641 beds). On the ambulatory side, we spoke with several facilities and confirmed that Cerner will be replacing Allscripts Professional EHR and Practice Management system for ~180 docs. This amounts to ~$1.1 million in lost revenue assuming $529 per doc per month.

We continue to view Allscripts (MDRX) as a share donor in the ambulatory market, driven by health system consolidation and implementation of integrated systems.

Allscripts is scheduled to report earnings after the close on 5/5. We like the short setup into the print given the run up in the stock since the February lows as we believe bookings and sales disappoint.

MCD

To view our analyst's original report on McDonald's click here.

On Monday, in a note to Real-Time Alerts subscribers, Hedgeye CEO Keith McCullough asked rhetorically, "What to buy?"

"On pull backs to the low-end of my immediate-term risk range, I'd be buying more:

1. Long-duration Bond Exposures (TLT, ZROZ, EDV, etc)

2. Low-Beta Big Cap Stocks With Safe Yields (MCD, GIS, NKE, etc.)

3. Gold (GLD)"

McDonald's (MCD) has all the style factors we like for these turbulent markets, which explains why it's up 27% since we added it to Investing Ideas in August.

Stick with it here.

WAB

To view our analyst's original report on Wabtec click here.

“The biggest piece of that is rail. Looks like it's going to be a tougher year for our customers in rail. They have a lot of locomotives idled and we think some of the orders on hand are going to get moved out to a later than this year.” – DeWalt, CAT Earnings Call 4/22/16

Without draining the Freight backlog, WAB would have missed estimates by a sizeable margin. The decline in WAB’s freight backlog corresponds to about ~90 million in revenue above orders (i.e. demand) in the quarter. At a mid-20s margin, that adds perhaps $22 million in operating income. That operating income is from orders received in a different demand environment, and will likely prove unsustainable. That is about 15% of earnings.

Another important aspect of the release is simply that sales growth is now negative for the first time since the financial crisis. Sales are still elevated due to the lagged impact of revenue recognition from orders received by both Wabtec and the company’s OEM customers. We have visibility into further declines across North American rail equipment deliveries – locomotive & railcar deliveries have not really budged yet – so it is just a matter of time, we think.

HBI

To view our analyst's original report on Hanesbrands click here.

This week Hanesbrands (HBI) announced another acquisition. The target is Australian underwear brand owner Pacific Brands. This is a big deal, both in size and importance. With a price tag of $800mm, it is bigger than the Maidenform and DBA Apparel acquisitions ($575mm and $530mm respectively). The company is paying a high 10x EV/EBITDA multiple for an asset at the peak of the economic cycle.

We'll be back with some more details on the acquisition and any impact to our short thesis resulting from our research process.

NUS

To view our analyst's original report on Nu Skin click here.

There was nothing in the 1Q16 numbers that would leave us pondering the SHORT thesis we have on Nu Skin (NUS). The company is still under investigation by the SEC, because of questionable business practices, but they were unable to provide an update on the progress at this point.

NUS reported 1Q16 results which beat the “guidance” provided by management and the consensus estimates that the Street was tracking to. NUS reported revenues of $471.8 million versus consensus estimates of $466.4 million, and EPS of $0.42 versus consensus of $0.37. In addition to the beat, they raised full-year guidance due to an improved outlook on exchange rates and, to a lesser extent, better than expected early results on LTO’s.

Management’s guidance for the full year is revenue of $2.16 to $2.20 billion; 2Q16 revenue is projected to be $560 to $580 million. Full year 2016 EPS is expected to be in the range of $2.65 to $2.85, excluding a $0.36 per share non-cash Japan customs charge, and 2Q16 EPS is expected to be $0.75 to $0.79.

Now, that all sounds good on the face for a NUS bull. But digging deeper the business clearly continues to deteriorate. In addition to VitaMeal sales declines, NUS Sales Leaders numbers declined as well. This is a major problem for them because as you can see below, as sales leader numbers have declined, we have also seen a massive decline in revenue per sales leader. This business is not as lucrative as it is painted to be, and people are starting to figure that out. To the extent that NUS continues to see sales leader declines their business will continue to deteriorate.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

After a busy week of earnings, our Healthcare analysts Tom Tobin and Andrew Freedman went on HedgeyeTV to provide a recap and key takeaways on Zimmer-Biomet (ZBH) and other high-conviction names like athenahealth (ATHN), MEDNAX (MD), and Hologic (HOLX).

Click here to access the associated slides.

TIF

To view our analyst's original report on Tiffany click here.

Productivity & Remodels

In their most recent analyst day, Tiffany (TIF) management was directly asked about productivity improvements with store remodels. The company could not clearly say there is improvement after the remodels are done. Meanwhile, management has plans for continued renovations/remodels and considers it a cost of doing business. But, if there hasn’t been a consistent sales lift we wonder if they are really necessary.

At the same time, it seems clear that management intends to sacrifice productivity in some store expansions (Japan, Vancouver) believing it will lead to additional leverage, but again without positive historical performance it seems that there is a high risk of 4 wall margin dilution.

Investing capital in assets which will produce same or lower productivity is a quick path to lower asset returns and a lower stock price.

LAZ

To view our analyst's original report on Lazard click here. Below is an analyst from Financials analyst Jonathan Casteleyn.

Lazard (LAZ) released its 10Q filing this week with data that was much worse than estimated. In the company's earnings report, it just outlines its financial results and not volume data. New information in the filing always includes industry M&A volumes, and with both completed, we learned M&A volume is cascading down. Completed M&A deals for the industry fell -10% year-over-year, which is backward looking and explains the very soft results in 1Q. However, announced activity per the 10Q fell even further at -20%, which means that the forward backlog is starting to get eaten away.

Furthermore, Lazard has one of the largest industry exposures to European activity and with the June 23rd BREXIT vote on the docket, there is a dearth of current deal making until corporate boards understand whether Great Britain will remain an EU industrial member. Both the M&A business and the firm’s asset management business continue to operate near peak margins which means there will be plenty of downside compression as activity continues to dry up. The stock is still highly recommended by most analysts that cover the stock and we are one of the only firms with a cautious view on shares.

FL

To view our analyst's original report on Foot Locker click here.

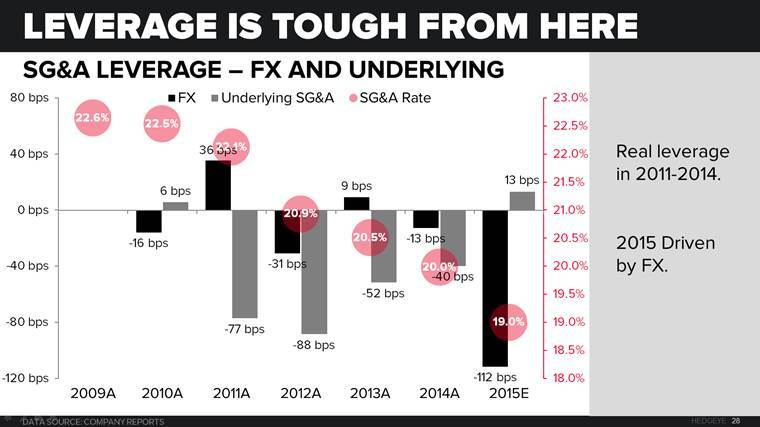

Foot Locker's (FL) SG&A rate stands at an all-time low 19% of sales, the lowest we have seen in mall based retail. From 2010 to 2014, FL saw growth with minimal investment in SG&A, as traffic was driven by increased allocations of Nike product rather than Foot Locker spending on ads and customer experience.

In 2015, FL continued to leverage SG&A on the reported P&L, however, much of this was driven by FX rates causing lower SG&A costs internationally and not real underlying expense management. Now the SG&A rate is at trough, real leverage is tough from here, and FX is going from tailwind to headwind. As the SG&A rate goes up and comp growth slows, FL earnings will be going nowhere but down.

GIS

No update on General Mills (GIS) but we continue to like the company as one of the best large cap names in the packaged food space.