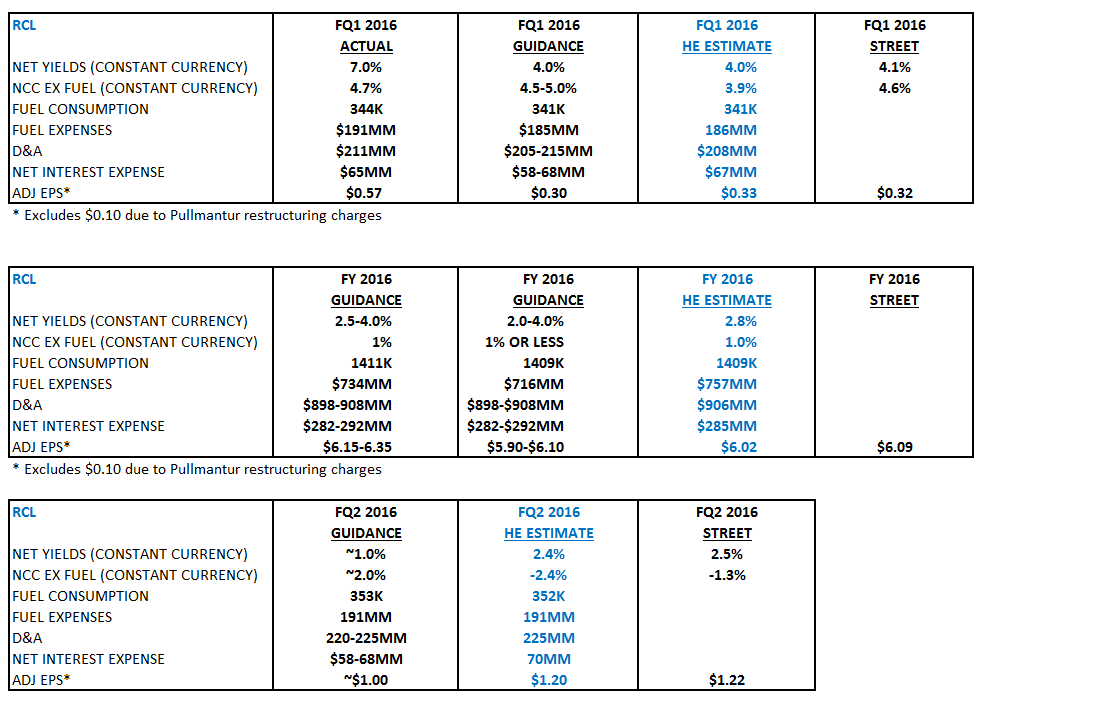

Here are our takeaways from today's release and conf call:

- Thanks to close-in North America business the Q1 yield beat was huge. However, Q2 guidance is much weaker. A simple calculation would suggest 1H yield growth average 4% (it's actually a little less than 4% since Q2 has a higher weighting in terms of revenue contribution than Q1) which is slightly ahead of our expectations and the Street's. This is why only the low end of FY yield guidance was raised by 50bps despite the huge Q1 beat.

- But the Q2 weakness is more concerning

- Additional promotional discounting is needed in the Mediterranean for the close-in bookings to fill the ships. RCL has had to source more guests from Europe than usual (69-70% of European business (usually 2/3)) since North America guests are more hesitant to booking into Europe, a point we emphasized in our recent cruise presentation. As a result, RCL is lowering their yield expectations for Europe. This sourcing shift is also a negative for NCLH's European business which is mostly US-sourced. In addition, European guests spend lower on board the ships than North American guests do.

- The company continues to blame capacity increases in China, particularly in Shanghai. Management's tone has shifted from high optimism to caution regarding China. Capacity in China is 9% this year vs 6% last year.

- Low end of expectations in Shanghai (50-60% of total China business) i.e. Quantum of the Seas and Mariner of the Seas. Everyone knows China is a close-in market. In its release, RCL implicitly suggested that visibility on China's bookings environment is getting murky. RCL certainly feels tenuous about China currently. In our recent cruise presentation, we stressed pricing pressures in China.

- The Easter shift accounts for 20-30bps, shifting from Q1 to Q2 2016.

- Introducing 2 new ships (Harmony of the Seas/Ovation of the Seas) ramps up occupancy but at lower yields - Harmony's inaugural sailings is in a tough European environment and Ovation is in China, which has seen lower yields YoY in 2016.

- Fuel/FX - Midpoint FY 2016 EPS guidance was raised by 25 cents with 15 cents contributing from a FX/fuel tailwind. FX/fuel benefited Q1 by 8 cents, which implies a 7 cent tailwind for the rest of 2016.

- But bunker fuel prices have risen on average ~15% since Q1 which leads us to believe that mgmt's fuel expense guidance could be too low

- Meanwhile, the US dollar has weakened ~5% for RCL's blended currency basket since Q1.

- Hence, so far in Q2, the tremendous rise in oil prices has outpaced that of the US$ weakness which suggests the 7 cent tailwind for the rest of 2016 may come in a little bit lower if current prices persist.

- NCC ex fuel growth guidance was raised slightly for the full year to 1%. It's not that big of a hike but any hike isn't great as China costs have increased.

- Caribbean is less important going forward. For some perspective, Caribbean deployment in Q1 was 63%; it's averaging ~39% for the rest of 2016. For Europe, itineraries accounted for almost 0%; for 2Q and 3Q, Europe accounts for 28% and 40% of RCL's capacity, respectively. China deployment overall, as mentioned above, is also higher YoY due to Ovation's entry into Tianjian into late June 2016.