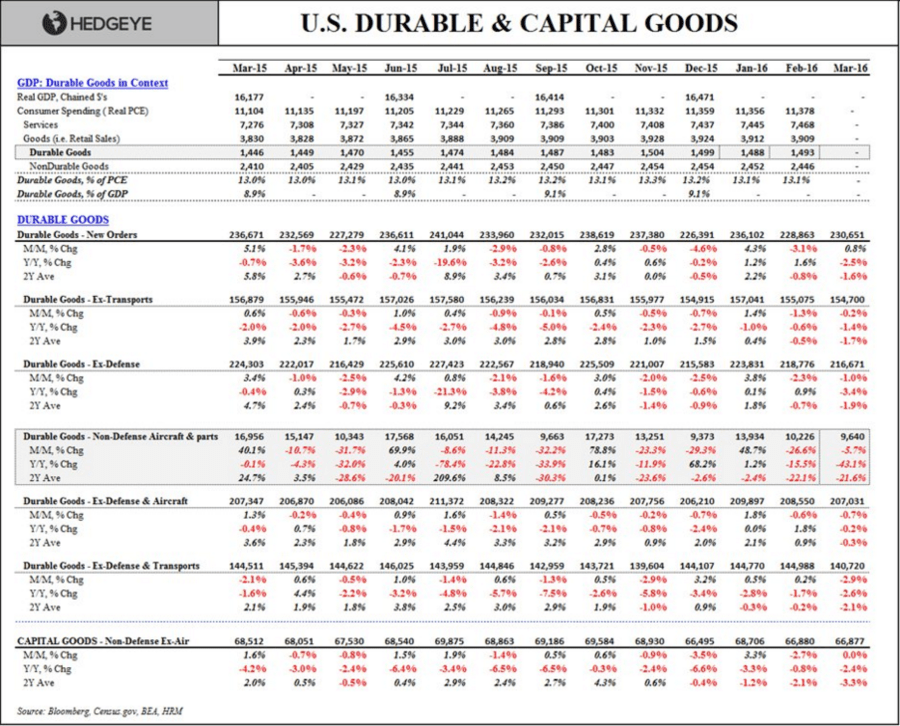

1. Durable goods down -2.5% y-o-y Today.

2. Consumer Confidence Still Off Feb. 2015 peak.

Nothing to see here. Go buy stocks...

Back to the data.

As Hedgeye Senior Macro analyst Darius Dale wrote today: "BREAKING: U.S. Durable and Capital Goods violently puke in March... What recovery?" Here's the Durable Goods table (notice all the nasty-looking red):

Click the image below to enlarge.

A more simplistic (sic "obvious") #GrowthSlowing breakdown looks like this.

Another bitter pill for bulls to swallow...

Consumer confidence continues to decline from its February 2015 peak, dropping to 94.2 in April versus 96.1 in March.

Basically, it boils down to this:

If you're buying stocks on the effervescent hope that U.S. economic data is improving, think again.