Investors are slowly starting to acknowledge that the central planning #BeliefSystem has failed. Despite ECB head honcho Mario Draghi's best efforts, there's more evidence out of Europe's muddling economy this morning.

Here's the latest data dump out of Europe:

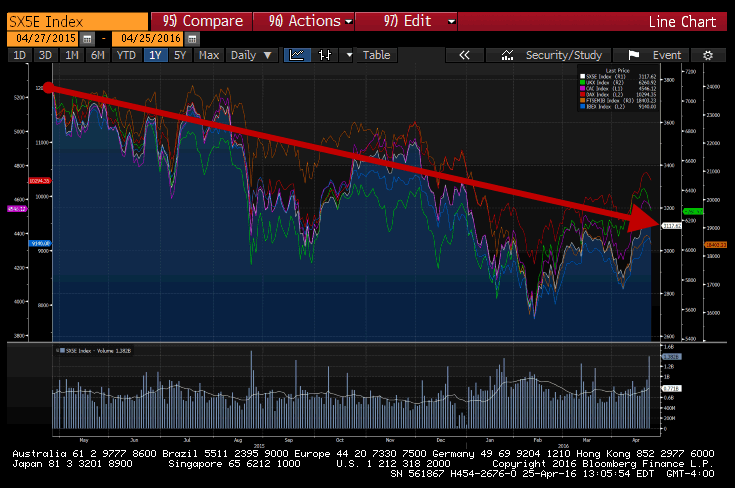

No surprise ... it's been a rough year for European equities.

Here's a smattering of performance data across the Eurozone (1-year change):

- EuroStoxx 50: -16.1%

- UK, FTSE 100: -11.5%

- France, CAC 40: -12.6%

- Germany, DAX: -12.8%

- Italy, FTSE MIB: -21.4%

- Spain, IBEX: -20.6%

Last week, Draghi did his best to instill confidence. European equities bounced. Today, it's back to what actually matters. The data.