Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

"... Do (or did) you believe that growth would slow this fast, from 3% to 2% to 1%?

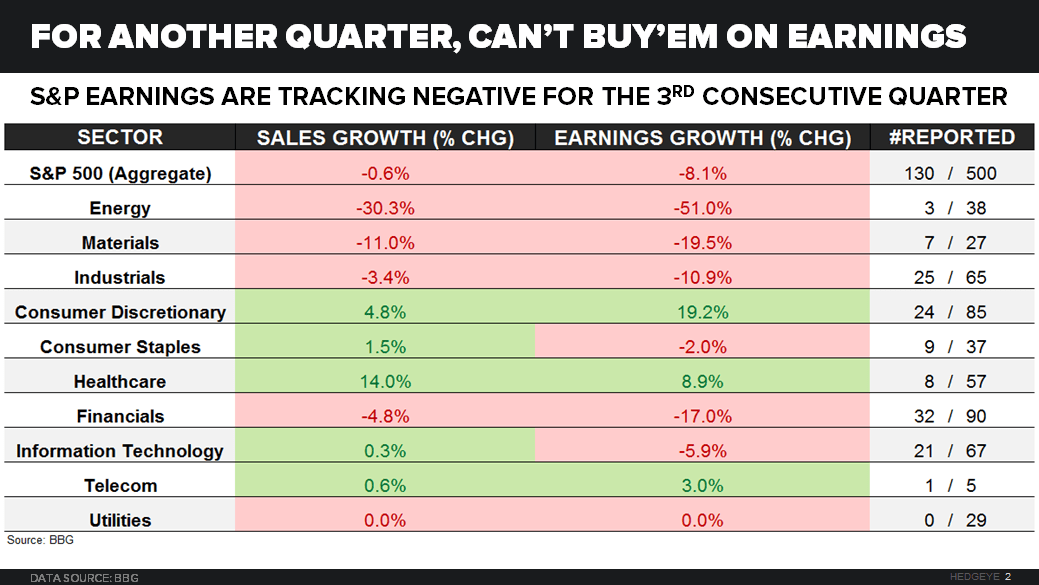

Or did you believe in it so clearly that you knew that the Financials (XLF) would start Earnings Season with the following reality:

- 32 of 90 “Financials” in the SP500 have reported their respective quarter

- Aggregate Earnings (non-GAAP!) are currently -17.0% year-over-year

- Financials (XLF) had their “reflation” rally now too (back to -1.2% YTD)"