Below are our analysts’ new updates on our sixteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this.

Please note that we added Deere & Company (DE) to the short side of Investing Ideas this week. Industrials Sector head Jay Van Sciver will send out a full stock report next week. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

MCD

To view our analyst's original report on McDonald's click here.

McDonald's (MCD) released earnings Friday reporting strong numbers across every important metric. Consider, for example, Q1 EPS $1.23 versus FactSet's consensus estimate of $1.16.

Here's the breakdown from the earnings report:

Same-store sales by region:

- US +5.4% vs consensus +4.4%

- International Lead Markets +5.2% vs consensus +3.9%

- High Growth Markets +3.6% vs consensus +3.1%

- Foundation Markets +11% vs consensus +5.3%

Revenue by region:

- US $2.02B vs consensus $1.98B

- International Lead Markets $1.73B vs consensus $1.72B

- High Growth Markets $1.44B vs consensus $1.44B

- Foundation Markets $713.3M vs consensus $705.7M

Margins:

- Company-operating margin 15.4% vs consensus 14.9% and year-ago 14.3%

- Franchise margin 80.7% vs consensus 80.7% and year-ago 80.3%

- SG&A 9.8% vs consensus 9.6% and year-ago 9.8%

Though there wasn't much additional commentary about current trends, we see this momentum continuing into 2Q16.

Bottom Line: We are sticking with our $150 target and believe that $7.00 in EPS for 2017 is not out of the question.

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

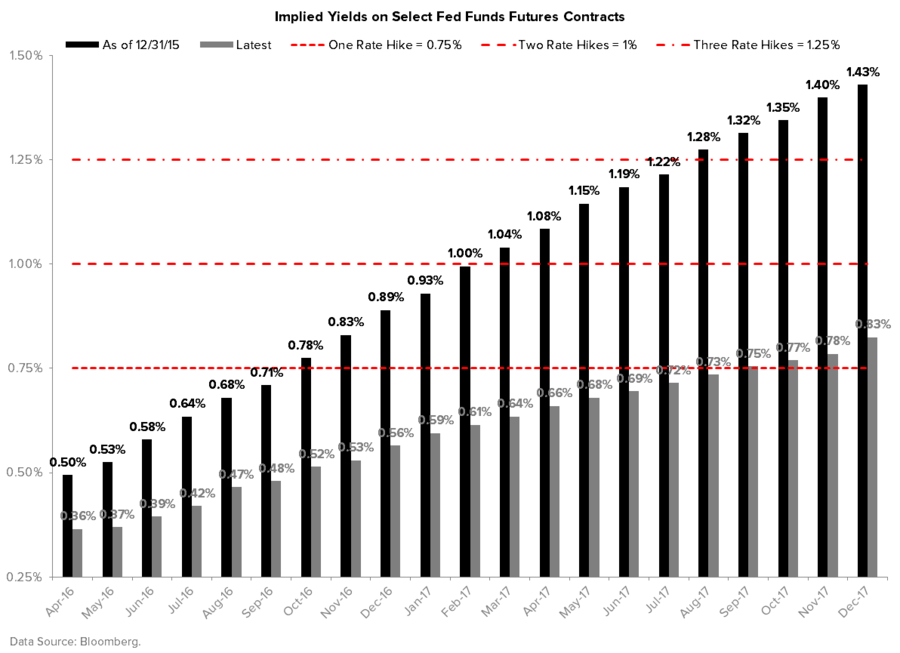

Coming into the year, the Fed had the market convinced that 2016 would bring at least one more rate hike. Four months later, however, market expectations have been turned upside down. In the chart below, we outline current expectations (gray bars) relative to expectations on December 31st 2015 (black bars).

The market is currently pricing in a rate hike but not until … late 2017. So if you’re looking for reasons to buy the market at all-time highs, don't expect a boost from incremental Fed policy.

To be clear, the dovish Fed commentary of late is a direct result of U.S. growth slowing. More evidence of that this week. Friday’s manufacturing PMI continued its downward trend (it peaked in rate of change terms in August 2014). Clearly, the market gets decelerating growth, which is why Utilities (XLU) are leading equity sector divergences YTD (+9.3%) and the U.S. Treasury 10-year yield down 0.35% over that same period. (That translates into TLT +6.5% and ZROZ +10.2% year-to-date.)

With that being said, the alpha on our long utilities and Long Bonds (TLT & ZROZ) vs. short Junk Bonds (JNK) position has gone against us in the last two months. Notably, we have no direct exposure to commodities or commodity-related sectors, but being short of JNK amidst a huge rally in commodities has not been a good position. Much of the beaten down resource-leveraged credit has rallied.

However, we would ask several important questions with regards to the prospective continuation in current market trends:

- Q: Are you buying reflation assets on continued monetary policy accommodation?

A: You can’t because the market’s already priced-in full blown dovishness (the aforementioned chart), and you’ll need something more like 1,800 on the S&P before you’d get QE4.

- Q: Are you buying reflation assets on earnings?

A: No, because S&P 500 earnings reported so far for Q1 are signaling a third consecutive quarter of negative Y/Y earnings growth. S&P 500 earnings are down 8%, thus the market is trading at increasingly peak multiples.

- Q: Are you buying reflation assets because growth has bottomed and is set to pick up?

A: No, the deceleration in growth has not inflected meaningfully with all relevant data considered. Our Growth, Inflation, Policy model has the U.S. economy tracking in the 4th quadrant which is a set-up where both growth and inflation are decelerating. The 4th quad is historically the worst set-up for commodities and commodity leveraged sectors, and there is currently little incremental policy response to this deflationary environment.

MDRX

To view our analyst's original report on Allscripts click here.

We confirmed that Dignity Health and Sacred Heart Health have plans to migrate over to a new EHR system from Allscripts Touchworks EHR. Both of these current Allscripts' (MDRX) clients we flagged as being 'at risk' in our January 2016 Best Idea Short Black Book.

Dignity Health signed a contract with Cerner in February to extend their PowerChart EHR into the ambulatory clinics, displacing Touchworks for +600 docs. Sacred Heart, part of Ascension Health, is in the process of switching from Touchworks over to athenahealth's EHR in 1Q16 for ~200 docs after having already moved over to athenahealth's practice management system in 2015.

Click the image below to watch our Healthcare analysts Tom Tobin and Andrew Freedman providing key earnings previews on Investing Ideas companies like MDRX and ZBH as well as other high-conviction names on their long and short list.

Click here to access the associated slides.

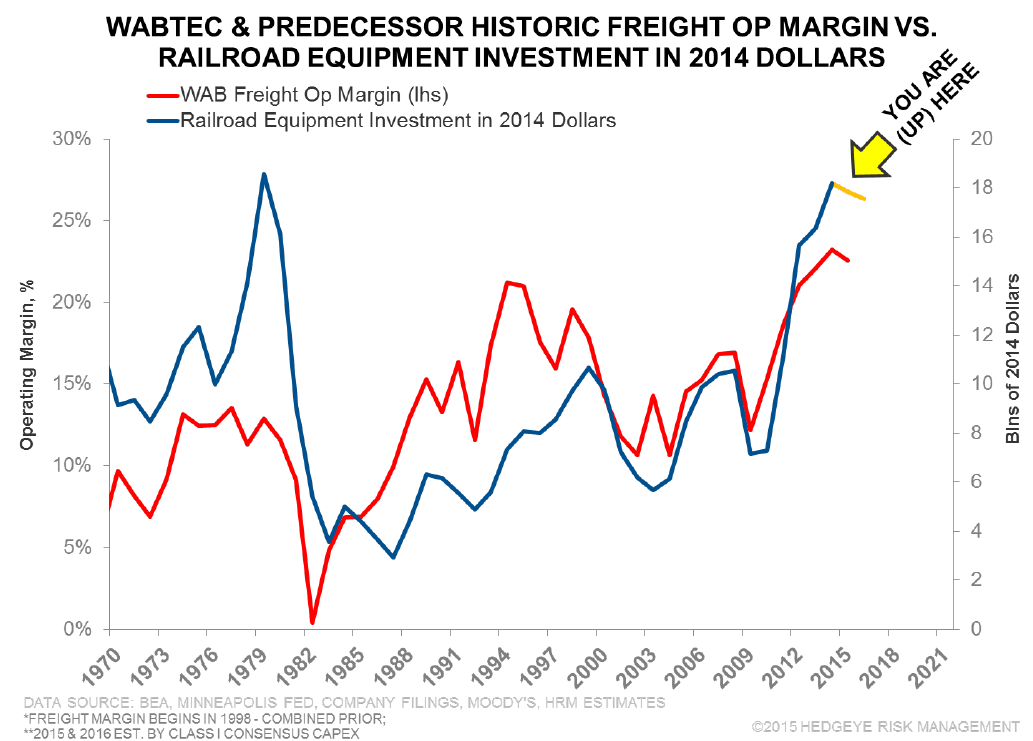

WAB

To view our analyst's original report on Wabtec click here.

U.S. rail volumes continue to deteriorate pressuring Wabtec (WAB) customers to curb rail equipment orders and capex spending. Just the drop in rail volume alone is troublesome for WAB. Management forecasted flat rail traffic for 2016. Based on the relationship of rail traffic to economic growth, GDP would have to come in over 8% to hit flat rail traffic, unlikely given the current economic conditions.

GE, in their earnings release Friday, received zero locomotive orders, while another WAB customer, Trinity Industries (TRN), reported the fewest freight car orders since early 2010. The Trinity and GE news confirms our view that the railroad equipment market is beginning a multi-year downswing. WAB reports this Tuesday, the 26th.

HBI

To view our analyst's original report on Hanesbrands click here.

On Thursday, Hanesbrands (HBI) printed what we think was a very good quarter – by HBI standards. Unfortunately for us, we’re short the stock. By ‘good quarter’ we mean that the company actually managed to grow sales by almost a whole percent. To HBI’s credit, it leveraged $10mm in higher sales into $14mm into higher profit. As a sanity check, that is not mathematically possible even if HBI had absolutely zero cost against its tighty whities this quarter – you know – those little things like labor, cotton, shipping, etc...

In reality what happened is that the company pushed expenses into 2Q. That’s not a sin. Every company moves costs around all the time. But it should be taken into account when evaluating the growth algorithm – particularly when the cash conversion cycle eroded by 43 days like it did in 1Q. We saw a nice little squeeze in the stock on Friday, but we still look at this through a bigger lense.

On the stock, we’re still within a buck of when we put the short on. On the idea, the simple fact remains that this is a company that sells a commodity product that has peak margins – which happen to be greater than Nike, UnderArmour, Ralph Lauren, and any other self-respecting clothing company with brands that are significantly more defendable than Hanesbrands. While at peak margins, the company is acquiring new business with its balance sheet, and we’re seeing the special charges stack up to boot. There is so little to like here.

NUS

To view our analyst's original report on Nu Skin click here.

Nu Skin (NUS) will report earnings Thursday April 28th. We will have a complete update on the company following the release.

ZBH

To view our analyst's original report on Zimmer Biomet click here. Below is an update from Healthcare analyst Tom Tobin:

We continue to hear detailed commentary from surgeons that we are entering an era of generic implants. It may not happen tomorrow, but the breadth and specificity of the comments we hear from the field indicate the trend is accelerating.

We find it hard to believe that Zimmer Biomet (ZBH) or the other manufacturers will do well in the new environment, but based on the commentary from SYK on their earning call earlier this week, they don’t expect generics to hit any time soon.

They also don’t believe the CJR will be an issue for them or the market, but that doesn’t mean they have it right. ZBH reports in the coming week and we’re estimating that the company lost share in US Knees, their most important product line. Assuming JNJ’s estimate of the market growth is correct, and they are correct that they picked up share, as did SYK from the look of the chart below, it implies a sub-par quarter for ZBH.

CME

To view our analyst's original report on CME Group click here.

Hedgeye Financials analyst Jonathan Casteleyn has no update on CME Group (CME) this week but reiterates his long call.

TIF

To view our analyst's original report on Tiffany click here.

Outside of the structural issues at Tiffany (TIF) we are seeing increased competition for traffic in key US markets as competitors both consolidate and expand. That equals greater competition for market share.

On the consolidation front, Signet (Jared/KAY) acquired Zales in May of 2014. That’s not new news, but we think it’s more relevant now that we are approaching the 2nd anniversary of the deal. That’s when we should start to see the benefit of company-wide synergies, especially on the sourcing side which, if passed through to the consumer, would make the environment more competitive.

On the expansion front, previously pure play only jewelry retailer, Blue Nile, will be opening its first brick and mortar location at the Westchester Mall in White Plains, New York early this summer. It’s the first of 4 test ‘webroom’ locations the company will open in 2016. That’s meaningful given the value proposition of the brand and customization options, and will compete directly with TIF for customer eyeballs.

LAZ

To view our analyst's original report on Lazard click here. Below is an analyst from Financials analyst Jonathan Casteleyn.

Lazard (LAZ) put up first quarter numbers that prove out our thesis:

- The M&A market is facing substantial headwinds; and

- The boutique advisory stocks are value traps;

We don't put much credence in "low" earnings multiples, as the entire group continues to over-earn with M&A coming off of its new 2015 high water mark. Yes, the pipelines are still fairly solid as the residual from an exuberant '15 hasn't been completely recognized.

However, forward activity, as measured by new announcements, is just starting to comp negatively in our view. Global M&A announcements were down -11% in the first quarter, with the all important U.S. region down -18%. While Europe held onto a positive year-over-year comp in 1Q16, BREXIT fears have the region on hold currently which raises the risk that Euro Land will not be a stabilizer going forward (the region makes up over 30% of revenues for LAZ’s advisory business).

What does it all mean for the bottom line? We continue to outline our $3.00 EPS estimate for 2017, which is about -20% below the Street before even touching the earnings multiple. We think that multiple should contract on forthcoming negative growth. It could be even worse, with $3 proving too generous. Our bear case estimate continues to be $2.20, in an environment in which M&A declines across the board and emerging markets retest new lows, a key product for the firm's asset management division. Did we mention the firm reported $0.50 in earnings yesterday?

Below is the BREXIT index of U.K. companies most exposed to E.U. revenues and the corresponding rollover in BREXIT stocks with a slough off in European weekly M&A announcements (green line).

FL

To view our analyst's original report on Foot Locker click here.

Shares of Foot Locker (FL) are down 7% over the past 90 days vs. the XRT +12%. That’s on the heels of an underwhelming 4Q15 earnings report and what we think will be a multi-year period of...

- A decelerating top-line,

- Eroding margins as the company has to invest to drive incremental top-line growth (see this year’s capital allocation plans as support); and

- Declining returns as margins come in and the growth story changes from asset optimization to international sq. ft. growth.

One of the big parts of our thesis is tethered to how the brands (Nike, UA, AdiBok, Puma, etc.) are changing the distribution paradigm for the first time since Phil Knight created the category. That’s playing out as the brands push beyond traditional wholesale partners to company-owned distribution, meaning that incremental growth is coming directly from the brands, both in stores and online. The balance is more heavily-weighted to online though.

In the case of Nike, we see the brand pushing its core US wholesale distribution to the maximum across nearly every account, TSA, DKS, HIBB, FINL, and most importantly FL. At the same time, NKE was using the cash flow generated from its outsized wholesale distribution growth to fund the systems/infrastructure buildout necessary to support an $11bn e-commerce business (which we think the company will hit by 2020). This means that the wholesale partners unknowingly facilitated this distribution shift.

From here, the NKE tailwind at FL is tapped out.

GIS

No update on General Mills (GIS) this week.