Our cartoonist Bob Rich captures the tenor on Wall Street every weekday in Hedgeye's widely-acclaimed Cartoon of the Day. Below are his five latest cartoons. We hope you enjoy his humor and wit as filtered through Hedgeye's market insights. (Click here to receive our daily cartoon for free.)

Enjoy!

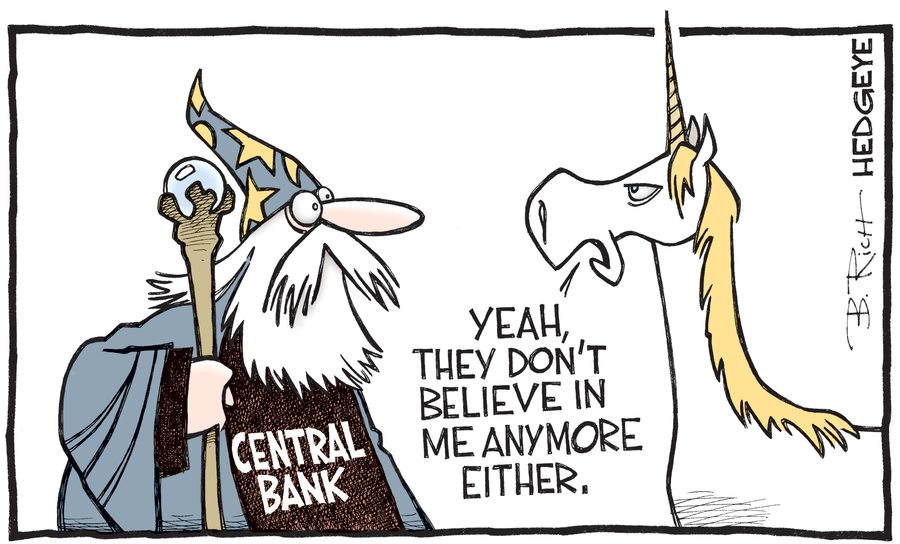

1. Just Believe (4/22/2016)

Central banker credibility is slowly waning.

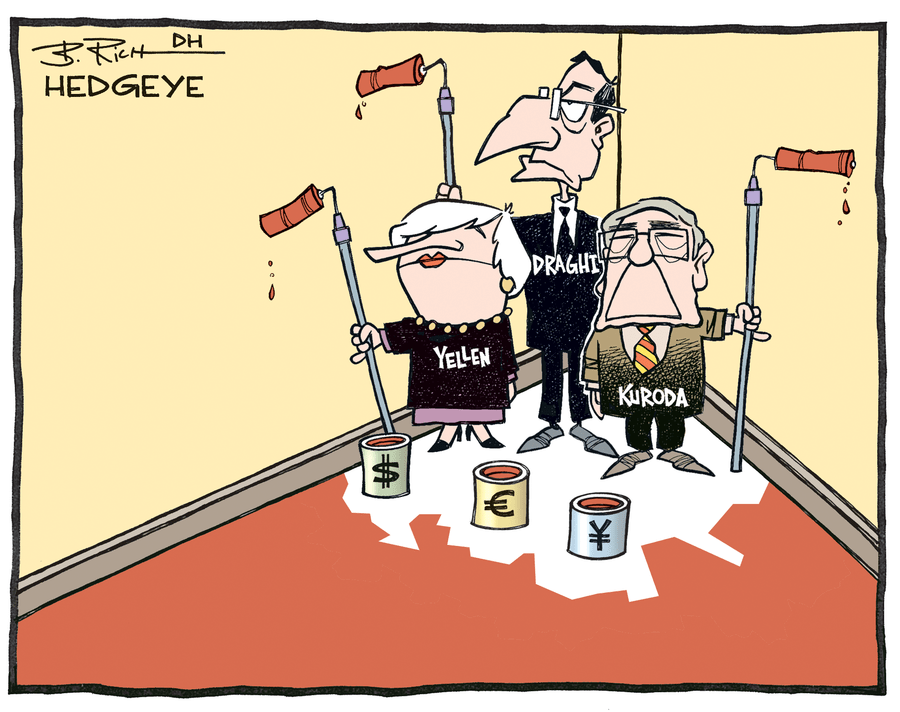

2. A Closer Look At NIRP (4/21/2016)

BOJ governor Haruhiko Kuroda has been defending the central bank's negative interest rate policy recently, even stressing his readiness to expand monetary policy still further. "Good luck with that," Hedgeye CEO Keith McCullough wrote recently. "These guys just don't get it. The #BeliefSystem is breaking down."

3. Painting Themselves Into A Corner (4/20/2016)

The #BeliefSystem that central planners can arrest economic gravity is breaking down.

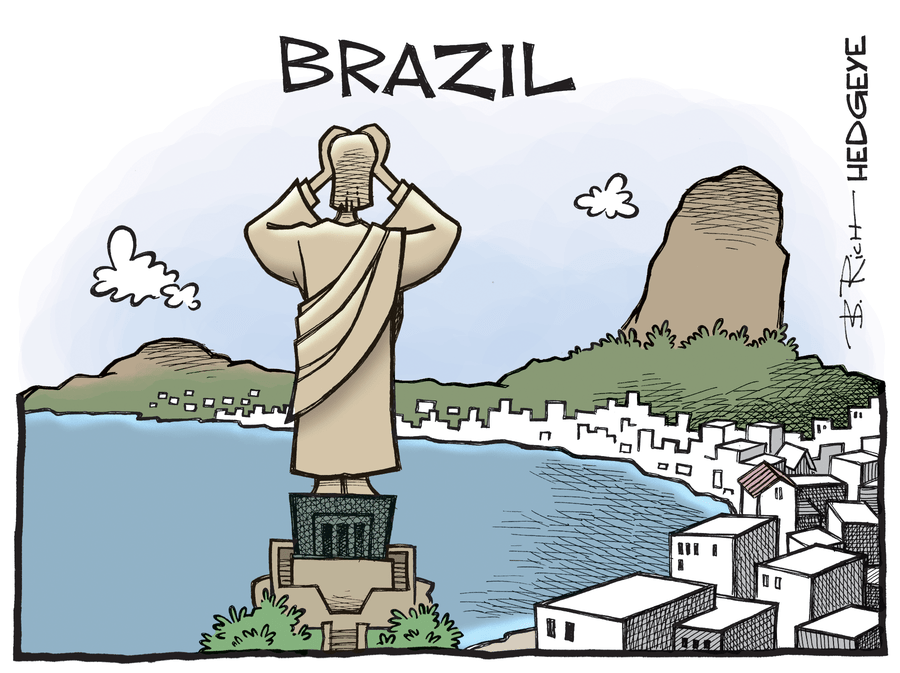

4. A Holy Mess (4/19/2016)

Amid the impeachment process of Brazilian President Rouseff, Brazil's Bovespa Index is up +39.4% over the past 3 months. Setting aside widespread corruption in the country, Hedgeye Senior Macro analyst Darius Dale had this to say about Brazil in this morning's Early Look, "We think Brazilian capital and currency markets are priced to perfection and anticipate another flush down alongside other reflation assets over the intermediate term."

5. No Oil Freeze (4/18/2016)

On Friday, Hedgeye colleague and Potomac Research Group Senior Energy analyst Joe McMonigle wrote, "We believe there is no chance Saudi Arabia reverses its position and agrees to freeze production on Sunday," after Iran announced it would skip the much-hyped oil "freeze" meeting in Doha. That proved prescient. Over the weekend, OPEC members, including Saudi Arabia, and non-OPEC countries, like Russia, failed to reach an agreement to freeze oil production.