We presented the bear case on Agrium last Wednesday at 11:00 a.m. with a blackbook and conference call. To summarize, we believe the retail business is misunderstood and subject to short-termism from an analysis perspective. In our view operating margins in the retail business, which have been stable post-recession, will contract meaningfully as the sector continues its long cyclical downturn. Ping us back directly for the deck or related inquiry.

Aside from our core thesis, below we outline some important catalysts to watch from a global trade perspective that will have implications for the competitiveness and profitability of U.S. farmers:

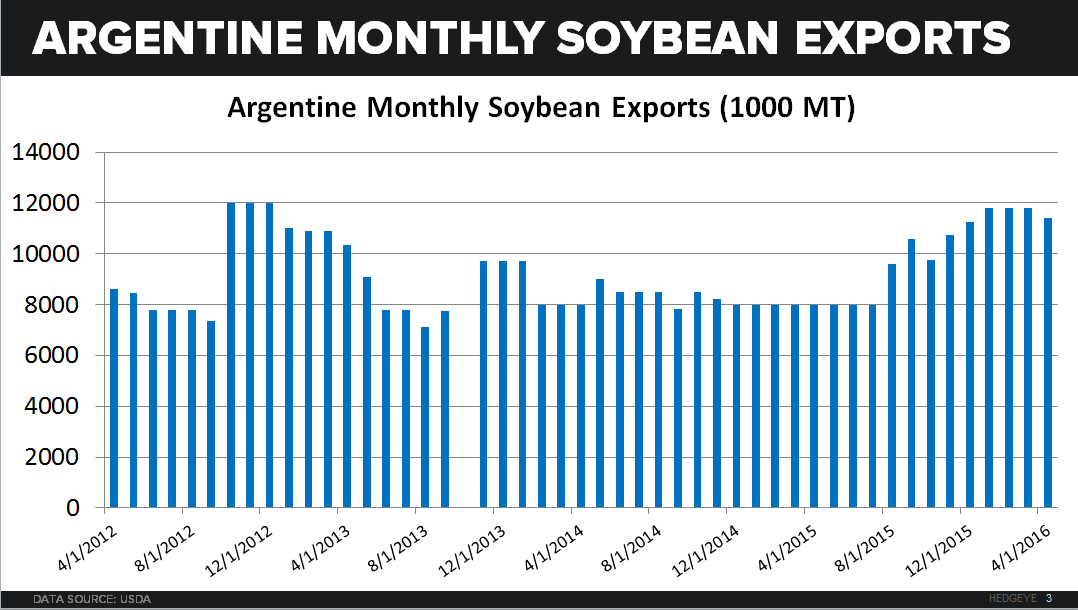

- EM FX Move: After a sharp EM currency move for the Brazilian Real and Argentine Peso, the currencies of the two largest soybean exporting countries have appreciated meaningfully against the USD since Jan-Feb lows, which should have implications for the profitability and competiveness of Argentine exports as they are now selling a record stockpile onto global markets in volumes not seen since 2012. Robust Chinese demand and a bout of rainy weather in Argentina is also helping support prices and bullish speculation on the CME.

- Brazil Factor: In Brazil, there is speculation on the direction of monetary policy and currency in particular should Rouseff be ousted (speculation for more hawkish policy from a new regime). With the lower house of congress voting to move forward with impeachment proceedings over the weekend, this appears more likely. Forward sales of commodities are reportedly being curbed significantly, and for soybeans specifically, this could shift some incremental buying to U.S. Markets: LINK

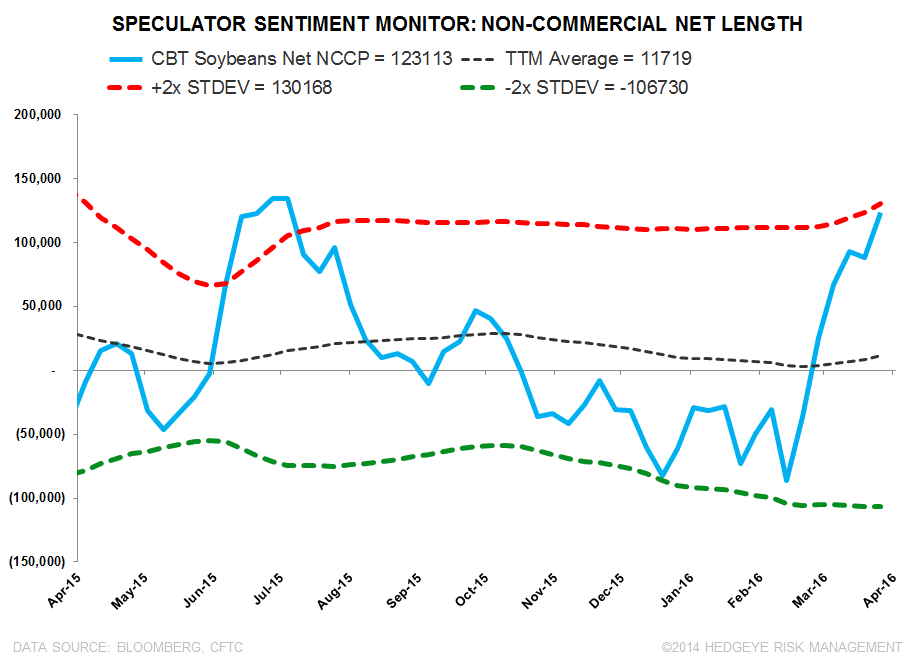

- Long Bias in Soybeans: Aggregating net futures and options positioning from the CFTC shows a soybean market leaning +2.4x and +1.9x on a 6-mth and TTM z-score basis.

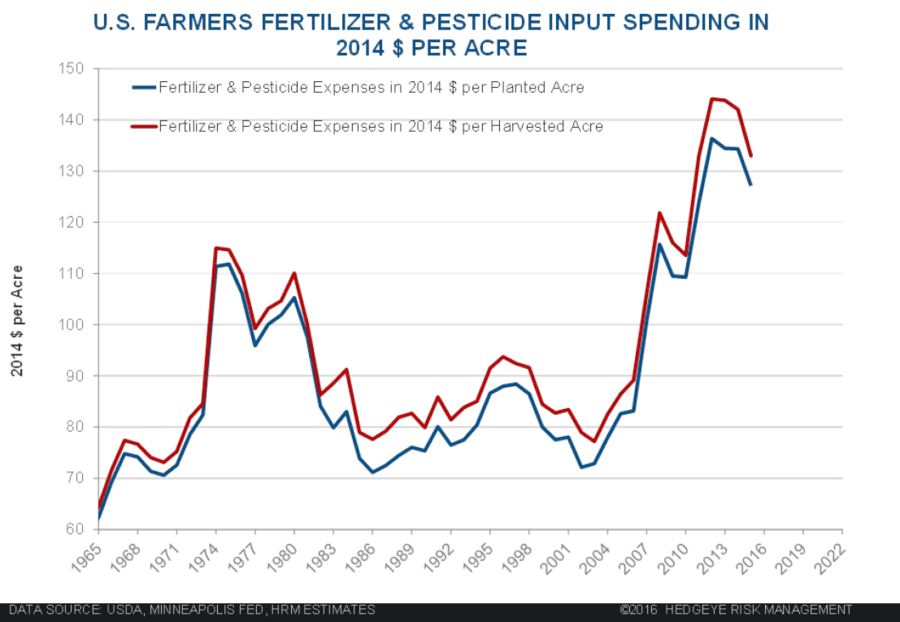

- Fertilizer Rates: With muted application rates in the fall window, fertilizer prices and regional spreads have moved higher off the Jan. lows (urea and ammonia), with a jump in the Cornbelt/NOLA ammonia spread. Although volumes should come in strong Y/Y given the muted fall application season, prices are still down considerably Y/Y. As the last chart shows, we believe there is quite a bit of margin to lose on pricing after an unprecedented increase in money spent on crop input expenditures over the last several years.