Below are our analysts’ new updates on our fifteen current high conviction long and short ideas. As a reminder, if nothing material has changed in the past week which would affect a particular idea, our analyst has noted this. Hedgeye CEO Keith McCullough’s updated levels for each ticker are below.

LEVELS

Trade :: Trend :: Tail Process - These are three durations over which we analyze investment ideas and themes. Hedgeye has created a process as a way of characterizing our investment ideas and their risk profiles, to fit the investing strategies and preferences of our subscribers.

- "Trade" is a duration of 3 weeks or less

- "Trend" is a duration of 3 months or more

- "Tail" is a duration of 3 years or less

IDEAS UPDATES

TLT | XLU | ZROZ | JNK

To view our analyst's original report on Junk Bonds click here, here for Utilities and here for Pimco 25+ Year Zero Coupon US Treasury ETF.

In the video below, Hedgeye Senior Macro analyst Darius Dale provides critical context on our high-conviction Macro ideas, with insights on #CorporateProfits, #CreditCycle, and #GrowthSlowing:

Here's a brief summary discussing the implications of Dale's presentation for Investing Ideas subscribers:

- #GrowthSlowing: We remain the bears on the U.S. economy and the corporate profit and credit cycles - we’re long growth slowing via Long Bonds (TLT) and Pimco 25+ Year Zero Coupon US Treasury ETF (ZROZ) and short risky corporate credit via Junk Bonds (JNK) as the profit cycle rolls over;

- #CreditCycle: High yield bonds have experienced meaningful relief in price terms with the move in reflationary assets. Again, we reiterate that once credit spreads move off their cycle lows, they don’t typically revert in the same cycle, which is why we are sticking with our sell recommendation on junk bonds (JNK);

- #CorporateProfits: Any time corporate profits decline for two consecutive quarters, the S&P drawdown has had a peak to trough decline of at least 20%. Dissecting the likely direction of earnings in Q1 and Q2 of this year, we could be facing 4 consecutive quarters of declining corporate profits, and we question the market's ability to slap higher earnings multiples on the S&P 500.

MDRX

To view our analyst's original report on Allscripts click here. Below is an excerpt from an institutional research note further dissecting Allscripts' (MDRX) Netsmart acquisition, as we highlighted in last week's Investing Ideas newsletter.

Netsmart DEAL OVERVIEW

Total consideration for the deal per the 8-k filing is $950 million, with Allscripts paying $70 million in cash and contributing its Homecare business (~$15-20 mill annual sales). GL Partners has committed to an unspecified cash contribution, with the remaining coming from non-recourse, third-party debt financing.

While we still have more questions than answers at this point, it appears the Joint Venture is actually structured as a VIE that is subject to a scope exception under GAAP, thus allowing Allscripts to consolidate the financials. This also allows Allscripts to recognize a greater financial impact from the JV with a minimal equity stake and liability as compared to a traditional merger or joint venture.

Other notable deal characteristics include:

- Combined organization $250 million ($150 mill 2016 incremental revenue to Allscripts) and $60 million operating income; accretive to 2016 Adjusted EBITDA, but not Non-GAAP EPS.

- JV debt non-recourse to Allscripts and wholly-owned subsidiaries; JV leverage assuming complete debt financing 10x operating income (no terms disclosed on financing facility).

- UBS loan commitment upwards of $612 million or 64% of the total consideration.

- Formation of 4 new legal entities: Nathan Holding (JV), Andrews Henderson LLC (Homecare Operating Sub), Nathan Intermediate LLC (Homecare Equity Vehicle) and Nathan Merger Co. (Merger Sub)

- Allscripts to receive 51% JV stake in Class A Common shares in JV equal to one vote per share.

- GI Members to receive 49% JV stake in Class A Preferred Units that are convertible to an equal number of common and carry one vote per share.

- Preferred Units entitles GI members in certain liquidation events (including sale of JV), to the greater of 1) a return of the original issue price plus an 11% preferred return (compounded annually) or 2) the as-converted value of Class A Common Units, and to cause the JV to redeem the GI Members equity upon the earlier of the fifth anniversary or a change in control of Allscripts.

- Management option pool that could result in up to 14% dilution in Allscripts' stake.

- First two years Allscripts and GL not permitted to transfer their equity to a third party without the other party's consent.

- Allscripts and JV agree to certain non-competition obligations to prevent Allscripts from engaging in the JV's core line of business and visa versa.

- Termination fee of $71.3 million paid by the Parent to the Company.

WAB

To view our analyst's original report on Wabtec click here.

With locomotives and railcars going into storage & rail capital budgets declining, Wabtec's (WAB) highest margin business, Freight, is indicating its worst book-to-bill in nearly a decade. For cyclical equipment companies, orders lead sales and this represents a major inflection downward for WAB. We still expect Wabtec (WAB) to earn well less than $4 per share in 2016, with weak 2H15 implied order rates as one of several supporting data points for that view. The company reports 1Q2016 results on April 26th.

HBI

To view our analyst's original report on Hanesbrands click here.

Hanesbrands (HBI) announced late last week that it is acquiring Champion Europe. Upon closing the deal, HBI will own the Champion brand globally. The company is paying 10x 2016 EBITDA or ~ $230mm which will be financed with debt.

Champion Europe's 2016 revenue is estimated at $220mm, which would contribute about 4 points of growth to HBI. In terms of scale, this is similar to the Knights Apparel acquisition which the company closed just over a year ago. The deal is expected to close in the middle of the year, around the end of Q2, at which time management will update guidance.

This has been the playbook of HBI for several years now, buying new 'accretive' businesses that will be followed by restructuring charges which cloak the slowdown in the underlying core business.

One interesting aspect of this deal is that the projected IRR is low to mid teens, which is lower than the Knight Apparel (High Teens) and Maidenform (mid-teens) acquisitions. We think the return profile for deals will continue to trend downward. HBI is paying up for this deal at 10x EBITDA vs 8x for Knights last year and 7.5x for DB Apparel in 2014. Most importantly, acquired growth is coming at a higher cost.

NUS

To view our analyst's original report on Nu Skin click here.

No change to our Nu Skin (NUS) thesis. For a company with ~20% SI, it has been a heavy participant in the recent rally, as some shorts are getting out. As the SEC investigation continues to unfold, NUS has provided documents pursuant to subpoena and they have also made available certain employees in the U.S. and China to provide testimony and respond to SEC questions. As this investigation unfolds, there is no telling what the SEC may find under the hood.

NUS is a structural SHORT for us, sporting miniscule market share globally, providing the majority of distributors with little to no profits, while operating a business model that is not sustainable over the long-term.

We continue to like NUS on the SHORT side going into the quarterly results on April 28th.

ZBH

To view our analyst's original report on Zimmer Biomet click here.

We spoke to an orthopedic surgeon Friday morning and continue to hear more details across several of our negative thesis points on Zimmer Biomet (ZBH).

- Generic devices are gaining momentum, bringing significant price pressure well above the -2% to -3% the companies and the market expect

- Large joint surgery in an Ambulatory Surgical Center is increasingly likely, adding to price pressure to the downside

- The #ACATaper is emerging and likely be a headwind to volume in 2016 and 2017

On the first point, we heard for the second time, that “brand name manufacturers” are circulating quotes for very low cost devices. These “generic” devices are falling in the range of $1,200 to $1,300 compared to the $6,000 to $8,000 device price range we have seen for much of the last several years. In some cases, these devices are being offered at such discounted prices as a strategy to take market share from smaller manufacturers.

For other larger players, the surgeon was spoke with believed these companies “saw the writing on the wall” regarding their “hyper-inflated pricing” for a device that “costs $300 to make.” We expect these cheap implants, offered by brand name US companies, will not have the same stigma or risk as using implants imported from overseas.

On the ASC front, where we expect lower implant prices versus the inpatient hospital since the sales rep is out of the OR and the ASCs are surgeon owned and operated for-profit ventures, it appears more likely that Medicare will approve and reimburse for large joint surgery in ASCs within the next 1 to 2 years. The pressure is building from commercial insurance companies who are now considering reimbursing for their Medicare Advantage patients as well as continued pressure from the Ambulatory Surgical Centers of America (ASCA) which continues to lobby for the change in strategic ways.

On the ACATaper, we heard that procedure volume growth accelerated to 20%+ in 2014 and 2015, in communities most directly exposed to the Affordable Care Act. In areas less exposed (more affluent), procedure volume was positive, but not nearly to the same degree. At least indirectly, this comment suggests the benefit of the ACA was real in ZBH’s results in the last several quarters.

It would also suggest that the marginally worse data we see in the JOLTs data and Medicaid per enrollee spending, in the last few months, would indicate much slower growth ahead for the US Ortho market. We are scheduled to speak to another surgeon next week whose surgical volume, we believe, was directly impacted by the ACA.

CME

To view our analyst's original report on CME Group click here.

With the largest Capital Markets operation reporting results this week, JP Morgan's numbers continue to relay the business-to-business (B2B) shift in both bond and equity markets. With capital hamstrung by Financial Crisis era regulation, and fixed income desks running tight as a drum, brokerage activity continues to shift over into the exchange traded derivative markets. JPM's FICC, or fixed income trading, results hit $3.5 billion in revenue in 1Q16, down 13% year-over-year.

Conversely, the daily reporting of CME Group's (CME) bond volumes finished at 8.2 million contracts per day in 1Q, up +9% from last year. On a revenue basis, CME's results are actually a little stronger, with fixed income rate per contract up +2% year-over-year. The shift in equities is more balanced, with JPM's equity trading revenues up +6% y-o-y according to their latest report.

CME's stock volumes, however, still outflank the big brokerage desk with futures and options volume up +9% y-o-y for the forthcoming quarterly report on April 28th. This activity shift is secular in our view and CME Group has a strong upward bias in earnings power which makes its stock one of the few to own in Financial Services.

TIF

To view our analyst's original report on Tiffany click here.

Tiffany (TIF) hosted an Analyst Day this week to update the investment community on its strategic initiatives.

The presentation was underwhelming, and the strategies outlined seemed to be more of the same, which has not worked for the company over the last 24 months. Even more disconcerting to us was management's inability to address some of the key business concerns of investors during the Q&A session.

Specifically...

- The company could not outline how the brand is performing in different age groups, as investors are concerned that the loyal TIF consumer is aging beyond its highest discretionary spending years while the younger consumer has less interest or connection with this legendary brand.

- The company could not point to causes of weakness in the domestic consumer and simply points to declines in tourist traffic.

- The company could not say that store renovations (i.e. Capital intensive projects) improve productivity despite continuing to invest capital in them.

We think earnings for TIF will continue to surprise to the downside until this company creates a new plan, backed with significant capital spending, to realign the Tiffany brand for long-term growth.

LAZ

To view our analyst's original report on Lazard click here.

We hosted an institutional conference call with a leading policy firm in Washington D.C. this week on the state of the mergers and acquisition market. Essentially, the message is that M&A activity, on the margin, WILL be impacted negatively with the release of new Treasury policy rules last week. Essentially, Treasury is clamping down on inversion strategies which will attempt to keep more corporations on U.S. soil. It will prevent them from acquiring foreign entities and then re-incorporating from a tax standpoint abroad (into the lower tax regime).

This new framework makes it harder to “invert” or change your tax jurisdiction, and the rules immediately resulted in the $160 billion Pfizer/Allergan deal to be canceled. This also resulted in over $100 million due to the advisors on the deal being nullified as well as a $400 million breakup fee to be paid from Pfizer to Allergan. Our D.C. policy contacts assigns very little probability of these new rules being overturned and thus all prior inversion strategies will dry up.

We estimate inversion deal flow to be 5% of all announced mergers and that leading advisory firms including JP Morgan, Goldman Sachs, and Lazard (LAZ) will be negatively affected. We continue to focus on Lazard as a pure play on M&A and emerging markets with the highest exposure to negative earnings revisions in the sector.

MCD

To view our analyst's original report on McDonald's click here.

McDonald's (MCD) is reporting 1Q16 results next Friday, and we will have a more thorough update following the release. Current consensus estimates are projecting system-wide same-store sales (SSS) growth to be +4.6%, and +4.6% in the United States. Given another full quarter of All Day Breakfast, and ever evolving value proposition that MCD is providing, we feel confident in their ability to perform at or above expectations.

MCD continues to be a great LONG stock to hold during turbulent times in the market given their attributes of being large-cap, low beta, and aligns with our macro teams view of going LONG lower to middle income food providers.

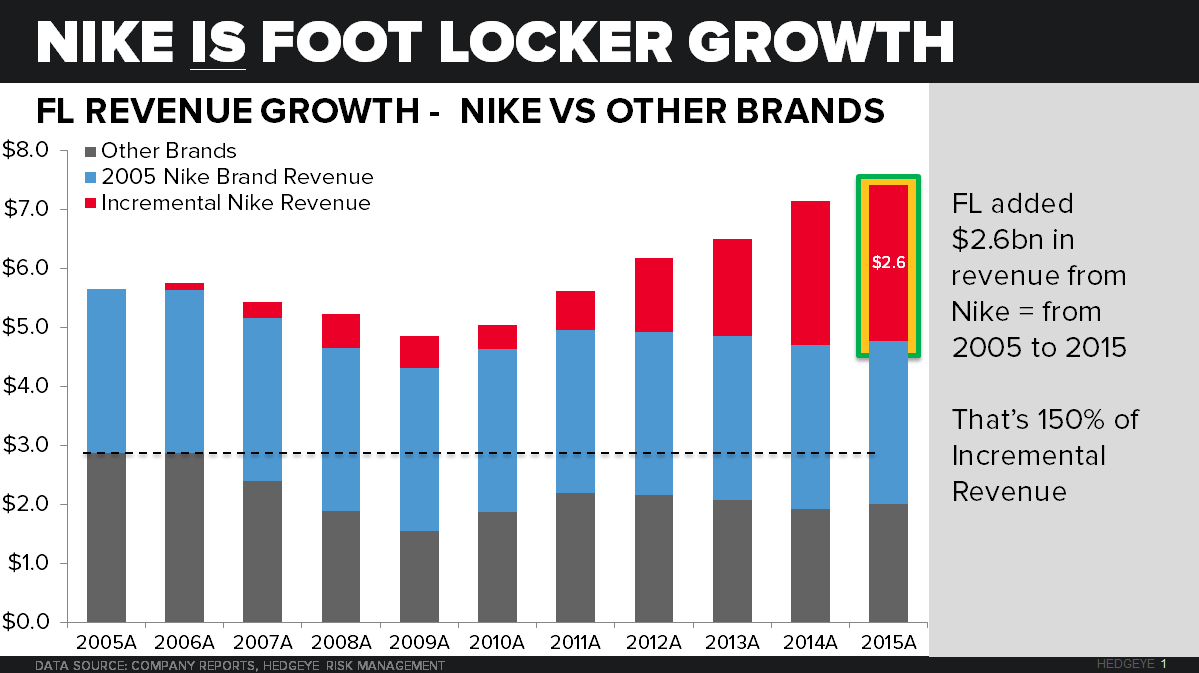

FL

To view our analyst's original report on Foot Locker click here.

Nike as a percent of Foot Locker (FL) sales has found a peak and there is little to no sales upside going forward from increasing Nike penetration. This point is critical to understand how important Nike has been for driving growth at FL. The chart below demonstrates Nike's importance. From 2005 to 2015, Nike contributed 150% of incremental revenue, as key competitors took less shelf space. This growth comes with minimal incremental spending, since the Nike brand power drives the customer traffic rather than FL marketing and store experience.

This tailwind for FL growth is now gone and the company will face competition from Nike scaling its direct-to-consumer distribution.

GIS

No update from our Consumer Staples team on General Mills (GIS) this week. However, Hedgeye CEO Keith McCullough did issue a "buy" GIS signal in Real-Time Alerts Thursday. Here's what he wrote:

"... In Macro, there are exposures (in this case #GrowthSlowing) that other Portfolio Managers (PMs) need to have in order to beat their competition. Another one of those exposures is Low-Beta Safe Yields.

That's why I like the Long Bond (on pullbacks to the low-end of the risk range) inasmuch as I still want to be long General Mills (GIS)."