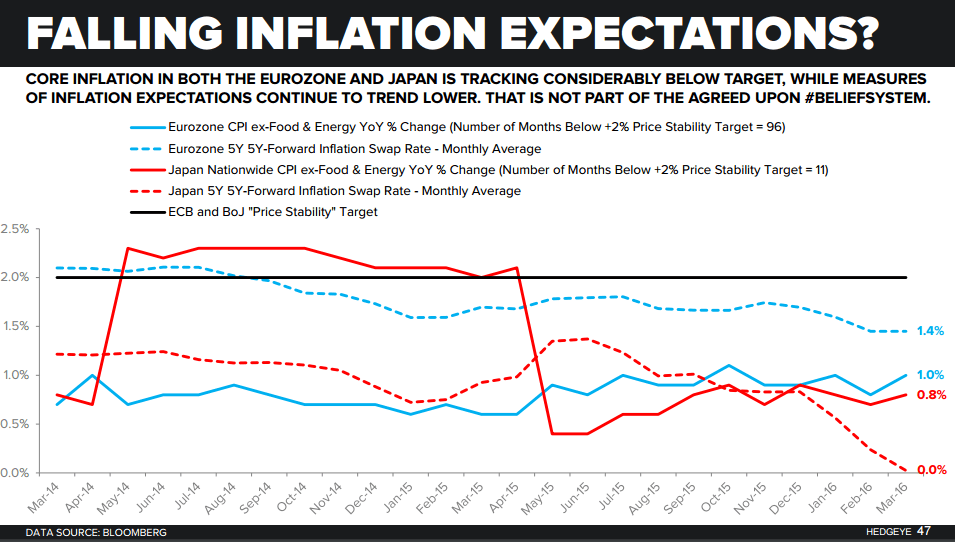

Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye U.S. Macro analyst Christian Drake. Click here to learn more.

"... As the Chart of the Day below illustrates, with swap rates, inflation expectations and growth estimates falling, currencies appreciating and European and Asian equities still in crash mode off their respective highs in the face of the latest quantitative and qualitative easing announcements, investors are believing that conditions are as bad as policy makers suggest but are in increasing disbelief of their ability to do anything about it."