What do you believe in? Do you still believe that ECB President Mario Draghi’s policy to do “whatever it takes” to burn the currency can and will spur Eurozone growth and inflation?

As we present in our Q2 2016 Macro Theme of #BeliefSystem (click here for the replay – slides and video – of our second theme starting on page 37 and minute 25:14), not only do Eurozone fundamentals continue to materially slow (witness the progression of slowing data over the last 12 months in the charts of Eurozone Retail Sales, Industrial Production, Exports, Consumer and Business Confidence, and Inflation), but the region is experiencing the perfect storm given the combination of:

Negative interest rate policy (NIRF) + Quantitative (and Qualitative) Easing + Talking Down of Forward Guidance.

According to our Big Bang Theory that we originally discussed ahead of the ECB’s March 10th 2016 interest rate meeting, we’ve underlined our view that after 600 rate cuts globally, there’s a new regime of investors that has given up on the belief that central bankers can artificially produce stimulus and weaken their currency for economic benefit. This policy hasn’t worked in Japan, and it isn’t going to work in the Eurozone.

Not only were we right with our call that more ECB “easing” would equate to EUR/USD strength (versus a bearish consensus view), but we’ve continued to be right forecasting growth and inflation levels below consensus.

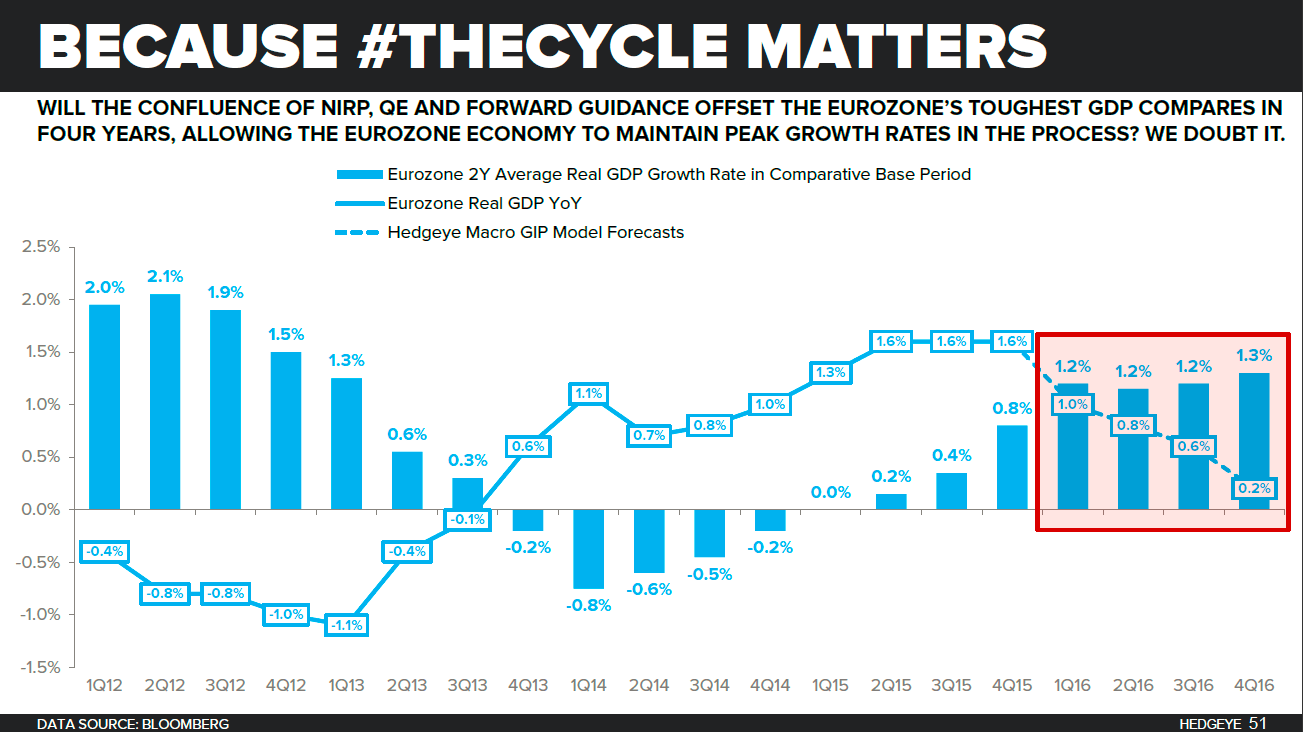

Specifically, we’ve signaled through our GIP (growth, inflation, policy) model that the Eurozone would return to Quad 4 (equating to growth slowing as inflation decelerates). In the second chart below, we show our forward GDP estimates over the next four quarters, declining to +0.2% in Q4 2016. #ouch!

If the deterioration of growth fundamentals and consumer and business confidence weren’t enough, the ECB’s negative interest rate policy is artificially pushing down bond yields, making it harder for banks to lend (while pilfering savers), and the equity market has taken it on the chin – the EuroStoxx 600 has crashed, down -20% Y/Y.

Schäuble Speaks – In related news, German Finance Minister Wolfgang Schäuble blew the horn this weekend echoing our sentiment on the negative impact of the ECB’s quantitative and qualitative policy. Specifically he suggested that the ECB’s loose monetary policy is partly to blame for the rise of the populist Alternative für Deutschland (AfD) party in Germany, and argued:

“I said to [ECB President] Mario Draghi…be very proud: you can attribute 50% of the results of a party that seems to be new and successful in Germany to the design of this policy. There is a growing understanding that excessive liquidity has become more a cause than a solution to the problem.”

We'll continue to bang the boards with our call that the #BeliefSystem in the Eurozone is broken -- that neither Draghi nor other central banker can bend economic gravity. This time is in fact not different, and as the Eurozone experiences the drag from an aging population (see chart directly below), the prospect of a buoyant and sustained economic recovery appears even further out of reach.