Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

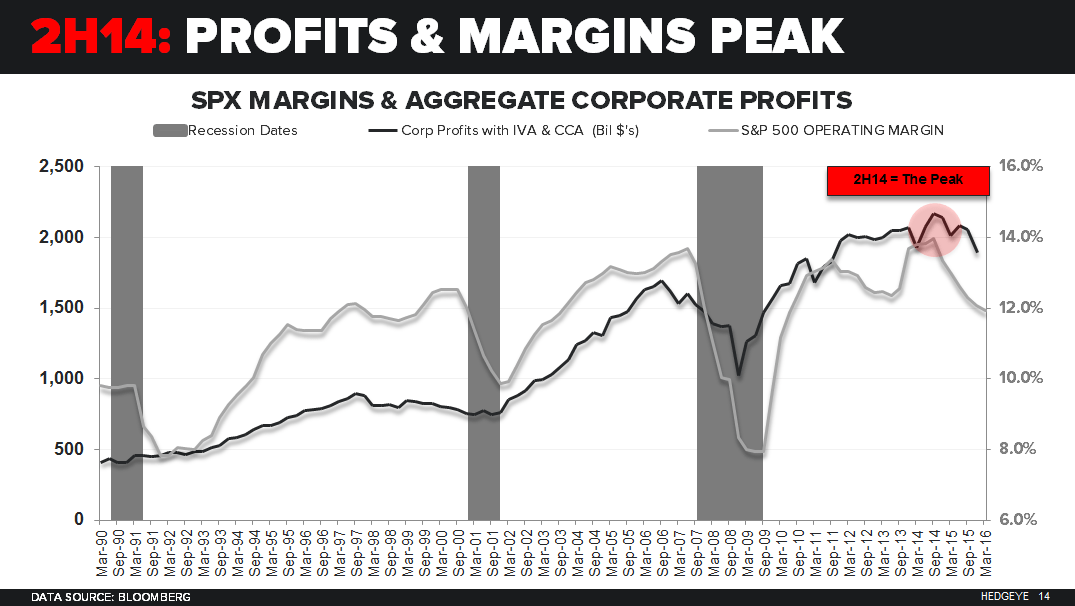

"... As you can see in today’s Chart of The Day (slide 14 of the recently published Q2 Macro Themes Deck), Aggregate US Corporate Profits put in the mother of all peaks (all-time high) in the 2nd half of 2014. In this chart you can also see where:

- SP500 Operating Margin PEAKED and rolled

- US #Recessions typically appear AFTER profits and margins PEAK"