“You don’t want to negotiate the price of simple things you buy every day.”

-Jeff Bezos

Maybe Bezos should become the national spokesperson for stocks. Why haggle over things like the rate of change in the economy and profits when you can simply buy stocks (with other people’s money) at every price, every day?

Back to the Global Macro Grind…

As Darius Dale and I head into Day 2 of Institutional Investor meetings in Boston, MA I’m going to proactively predict that we get hammered on one question that kept coming up yesterday: “what’s priced in?”

This is, of course, one of the most important questions that an objective investor would start asking you AFTER you’ve convinced them that the causal factor in things like the Long Bond (TLT), Gold (GLD), and Utilities (XLU) winning 2016 = #GrowthSlowing.

When the rate of change in growth slows from its cycle peak…

Drumroll… long-term bond yields fall alongside the collective economic expectation of consensus… and Low-Beta “quality” beats High Beta “leverage” to hopes like “reflation.”

On the latter, look at what Alcoa (High Beta Leverage) had to say as they kicked off Earnings Season last night:

- We missed revenues (again)

- We’re guiding down revenues

- We’re guiding down margins and earnings (and firing people)

Stock drops -5% on that. So what was priced in?

A) Alcoa crashing -60% from $17 to $7 from #TheCycle peak of 2014 to the FEB 2016 low?

B) Alcoa ramping +40% from $7 to $10 “off the lows” on the “bottom is in” view?

As 10th grade math majors know, if you lose -60% of your money in a stock “pick”, you need to be up +150% from that price (I’m using $7, but the stock obviously traded lower than that) just to get back to breakeven.

Moreover, if you don’t get anywhere near break-even, at some point (before and after Earnings Reports) you have to ask yourself:

A) If the underlying business, cash flow, balance sheet, etc. risks are improving or deteriorating and …

B) What’s priced in?

People who bought Alcoa in March of 2011 (with a $17 in front of it) were selling it into year-end 2011 with an $8 in front of it. For those of you who remember 2011, that’s when Bernanke had to save all natural buyers of “stocks” with unprecedented QE.

But Ben wasn’t able to save the performance spread between Utilities (XLU) and Financials (XLF) in 2011 (record high for Utes). He wasn’t able to stop Gold and Long Bond Bulls from having an awesome year either.

For Gold, 2011 was the top. For the Purchasing Power of Americans (US Dollar) that was Bernanke’s bottom.

With that historical context in mind, what if Janet Yellen is NOT able to go to Qe4 by Jackson Hole 2016? What if the US Dollar is about to lock in its YTD low and ramp back up from here? What is priced in under that probable scenario?

Or is it more probable at this point that we’re much more right on the economy than we’ve ever been, US GDP goes negative in Q2, profits continue to slow against #TheCycle peak, and Yellen goes all heli-ski-easy-money-drop on Trump for Hillary?

Lots of questions, but not a lot of time. Between now and when these cyclical realities take hold, that is…

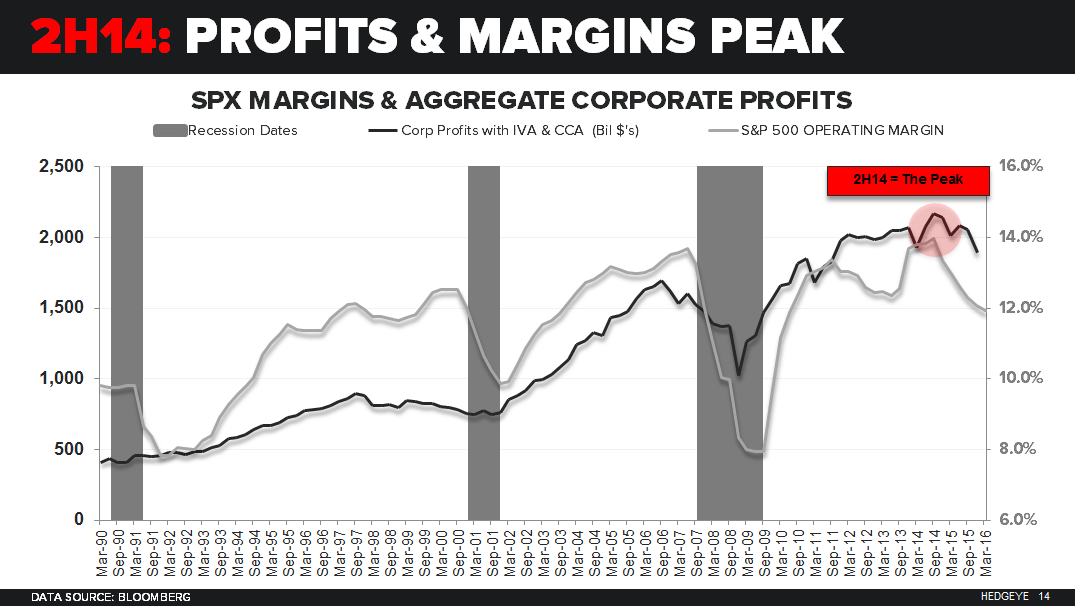

As you can see in today’s Chart of The Day (slide 14 of the recently published Q2 Macro Themes Deck), Aggregate US Corporate Profits put in the mother of all peaks (all-time high) in the 2nd half of 2014. In this chart you can also see where:

- SP500 Operating Margin PEAKED and rolled

- US #Recessions typically appear AFTER profits and margins PEAK

For long-term investors who have modern day risk management overlays to their stock “picks”, the relationship between profits, margins, and stock prices is very obvious.

Less-obvious at the March 2016 highs for the SP500? Yes. More obvious at the February 2016 lows? Absolutely.

Fully loaded with Premier Li’s comments that China continues to see “downward pressure on the economy” overnight, what’s “priced in” from today’s price (vs. February’s)? I’m looking forward to analyzing what’s left of the free-market negotiation.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.68-1.82%

SPX 2026-2058

RUT 1081-1105

VIX 14.07-19.11

USD 93.74-94.99

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer