Editor's Note: Below is an institutional research note written by Hedgeye Retail analysts Brian McGough and Alec Richards. To read more of our Retail team's research ping sales@hedgeye.com.

It's so easy to succumb to the 'water torture' of Chapter 11 press releases in retail coming from the likes of Sports Authority, Vestis Retail Group (Eastern Mountain Sports, Bob's, and Sports Chalet), and Pacific Sunwear. But it's important to take a step back. Then another. And another. Then, and only then, does the big picture come into focus about the broader economic cycle.

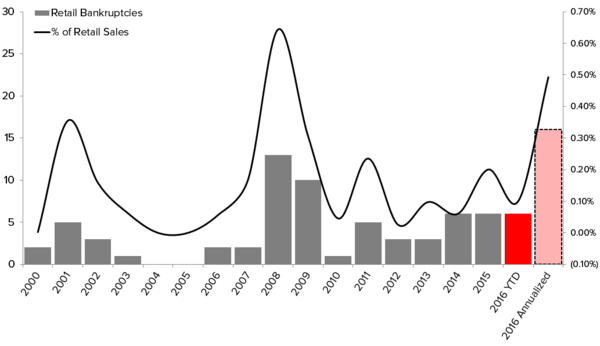

Consider this...over the average economic cycle, we see 15 to 25 retail chains go under. Those represent roughly 1% of Retail Sales. Naturally, the filings are not even by year. Sometimes (like when the economy is ripping) there are none. Plenty of profits to go around for even the worst retailers. But some years there's upwards of 15 (Great Recession).

In just a little more than three months, we've already seen 4 parent bankruptcies (6 chains) in US Retail. Annualized, that's about 16, or 0.5% of retail.

After an extremely tough winter selling season for shoes and apparel, it's only natural that we'd see this year push the 2016 tallies to a level close to what we saw in the Great Recession.

Sears, anyone?