Editor's Note: Below is a brief excerpt and chart from today's Early Look written by Hedgeye CEO Keith McCullough. Click here to learn more.

"... Yep. Wall Street is as long “reflation” (Oil and Gold on an absolute basis, and SPY on a relatively less net short basis) as it has been all year long and still fighting the wall of worry on our Long Bond Bull.

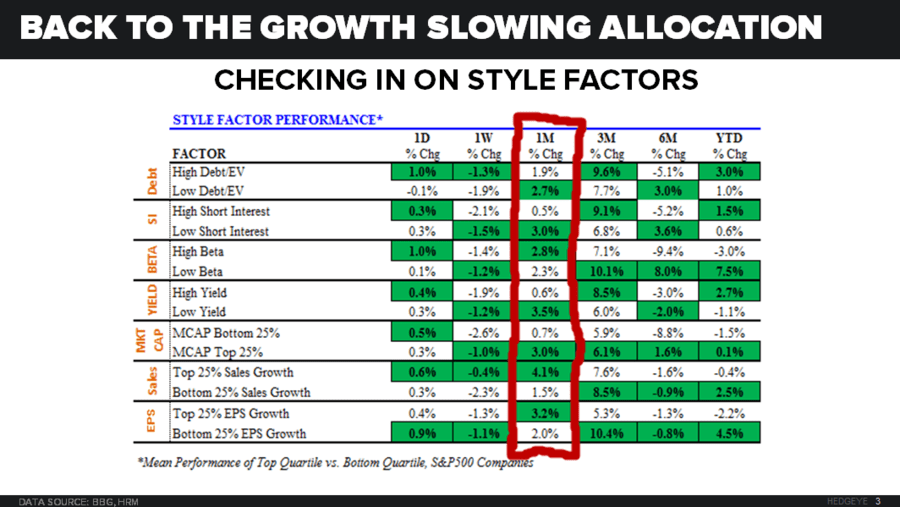

The 10yr US Treasury Yield dropped another 5 basis points (down -55 bps YTD) last week to 1.72% and continues to signal what US Equity’s top performing Style Factor (Low Beta Stocks = +7.5% YTD vs High Beta -3.0%) does…"