“Because I and my companions suffer from a disease of the heart which can be cured only with gold.”

-Hernan Cortes

Not to be confused with the disease of begging central-market-planners for more currency devaluation (punishes the many) in exchange for short-term asset inflation (pays the few), that’s how the boys back in the day used to think about pillaging populations for Gold.

“In 1519, Hernan Cortes and his conquistadors invaded Mexico, hitherto an isolated human world. The Aztecs, as the people who lived there called themselves, quickly noticed that the aliens showed an extraordinary interest in a certain yellow metal.”

Since the Aztecs were used to paying for things with cocoa beans and cloth, “the Spanish obsession with gold thus seemed inexplicable” (Sapiens, pg 173). Ah, what idiots those Aztecs must have been. They totally wouldn’t have understood QE either.

Back to the Global Macro Grind…

I believe that our profession is fighting a serious mental disease. I spent all of yesterday going from meeting to meeting in NYC and eventually, most meetings devolved into why stocks can’t go down because the Fed has an extraordinary interest in keeping them up.

‘Yeah Keith, we hear you Brofessor… you say it’s The Cycle… but if you’re right then the Fed is definitely going to bail out markets and go to Qe4, aren’t they? Why not? Seriously, think about everything the Fed can still do – they’re already going dovish…’

Sadly, at that point in the conversation (trust me, I have a lot of reps when it goes that way!), I immediately agree with the client and say, “absolutely – they can do anything they want to do – they can make it really big and super you-ge.”

That is core to the #BeliefSystem.

And, by the way, in going to “negative yields” (after 90-100 TRILLION Yen in money printing, per year, AND buying stocks) in Japan, and QE + buying corporate bonds in Europe, you know what their hoped-for stock market inflations are doing this morning?

- Japanese Stocks (Nikkei) down another -2.4%, taking their #crash since July’s (2015) high to -24.6%

- German Stocks (DAX) down another -2.4% this morning, taking their #crash since April’s high to -22.6%

- Italian Stocks (MIB Index) no bid, -1.8% this morning, taking their #crash from last year’s high to -28.1%

Q: Do you know what the range on the SP500 would be on a -23% to -28% #crash?

A: SPX 1

So, I’m “reducing my price target” (since everyone asks me for one!) to that range, down from a prior target of 1704 (which would be a -20% decline from the all-time closing #Bubble high of July = 2130).

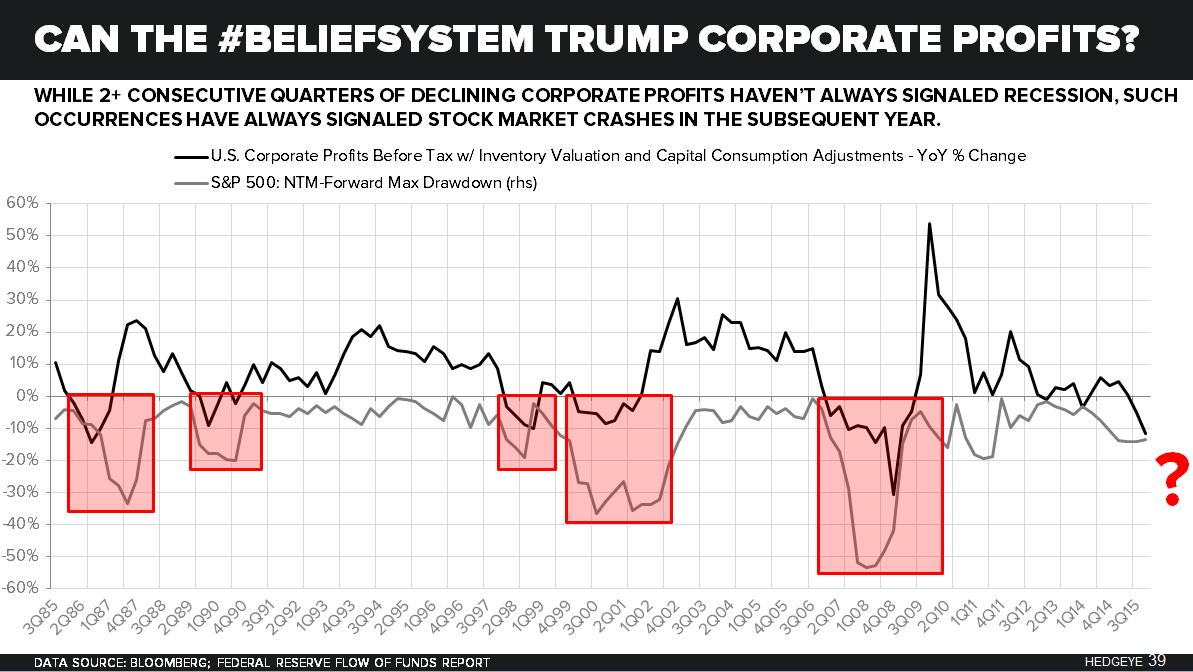

How the heck could that ever happen? It’s impossible that the #BeliefSystem could ever break down, isn’t it? Other than US corporate profits being negative for 2 consecutive quarters (which has always equated to a > 20% decline), what is your catalyst, Keith??”

A: The Cycle

Oh, am I teasing you? Not on the probability of 1704 then 1640 then 1533 rising (SP500). Just a little tickler for you ahead of our Q2 Macro Themes Call that we’ll host at 11AM EST on Thursday (ping for access).

In other news this morning, here’s how our Q1 Macro Ideas are doing (hint: I’m doubling down on them in Q2):

- Long-term US Treasury Yields dropping to 1.73% on the 10yr, only 5 basis points away from the Q1 low

- Utilities (XLU) are +14.6% YTD and primed to outperform Financials (XLF) -5.6% today with rates crashing

- Gold is +1.4% this morning to +16.2% YTD

Why didn’t the masters of the super smart alpha generating universe go all 16th century on their investors and ramp up their Gold holdings? “Believe me”, the spread on GLD vs. Valeant is super huge and really really smart. You need a really big brain for it.

According to the FT, Q1 report cards weren’t as good as yours was. Apparently 19% of mutual funds beat their benchmark in Q1. That was their worst quarter since 1998. Only 6% of “Growth” fund managers beat their bench (worst performance since 1991).

Many are suffering from a disease of expectations (either they’re too bullish on growth and/or always too bullish because they think the Fed can do something to replicate growth via asset inflation when they’re wrong) which can only be cured by performance.

So, instead of whining about where the SP500 is (which you don’t need an active manager to buy for you), I say they better get on board with our Best Long Ideas, Macro Exposures, and Style Factors, before it’s too late.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.71-1.85%

SPX 2018-2077

RUT 1069-1130

Nikkei 151

DAX 9

VIX 13.01-19.45

USD 94.11-96.06

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer