Editor's Note: In this complimentary edition of About Everything, Hedgeye Demography Sector Head Neil Howe discusses why manufacturers and retailers should prepare for the possibility that “goods” aren’t coming back anytime soon. And, even when (and if) the industrial sector emerges from its long-term atrophy, the underlying framework of the “old economy” will look entirely different than what we see today.

WHAT’S HAPPENING

Worldwide, the goods-producing sector is in trouble.

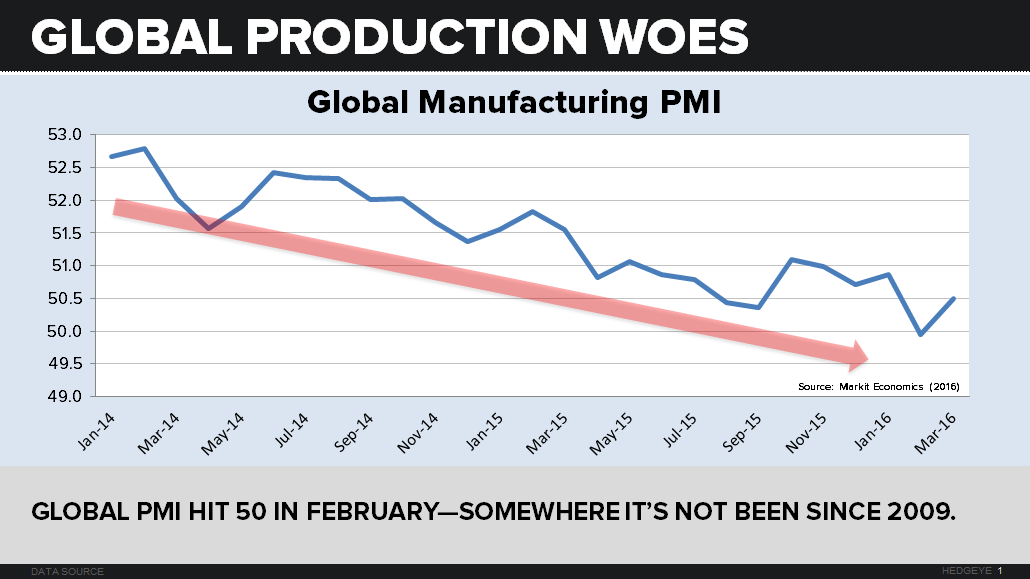

Ever since the Great Recession, global trade has struggled to keep up with GDP—something it used to beat easily. Over the last two years, the global manufacturing PMI has been steadily sinking.

The U.S. PMI has been under 50.0 for five of the last six months. Globally, both output and new orders are decelerating—for example in China, where manufacturing has been contracting for 13 straight months.

And what about commodity and producer prices? They’ve been tanking. Amazingly, the PPI in just about every major economy has been stuck in deflation since the summer of 2014.

Goods are being lapped by services. The services sector—encompassing activities like media, software, health care, and finance—has posted just one month of contraction over the past two years.

The decline of goods and the rise of services, of course, is a long-term trend that began many decades ago in the high-income world. U.S manufacturing employment peaked in 1979 and has mostly been declining ever since. Yet there was a brief respite following the Great Recession, especially here in the United States. Now, however, the goods sector is once again under assault.

Let’s take a look at some of the new forces that may be driving it down.

WHY IT’S HAPPENING: DRIVERS

The China slowdown

Up until 2014, China’s voracious appetite for more industrial capacity, housing, and infrastructure was propping up raw material prices and goods production worldwide. In its heyday, China was consuming roughly half of the world’s supply of just about every industrial input—from steel and copper to cement trucks and construction cranes. No longer.

Urbanization & Extended Familes

Over the last decade, U.S. rural counties have been depopulating and core urban areas have been growing much faster than historical trend. A rising share of Millennials are ditching their cars, flocking to cities, and starting out their careers in cramped apartments with limited space. More than a quarter of 18- to 34-year-olds live in their parents’ homes and don’t need to buy their own household goods.

Growth of the sharing economy

Old computers and furniture no longer get thrown in the trash, but now enjoy a second life thanks to services like Craigslist and eBay. Platforms like Uber and NeighborGoods allow people to find and use items they want without buying them.

“Experiences” as the new form of conspicuous consumption

In the old days, we bought expensive things to affirm their social status. Nowadays, we can buy expensive experiences and curate them on social media. We can thereby define ourselves more by what we do than by what we own. This trend has taken on new meaning with Millennials, who would much rather go out to dinner or attend a music festival than purchase the latest handbag or golf club.

Digital unicorns

Thanks to monumental advances in IT capabilities and infinite returns to scale, entrepreneurs can now start a profitable company without spending much at all on physical capital (or even on employees). Think Google, Uber, and Amazon. The whole concept of “book value” assets is becoming antiquated.

Demographic change

Aging societies (I’m looking at you, Europe and East Asia) no longer require capital-widening investment. A contracting working-age population no longer needs new factories—or even new houses. Moreover, the retired elderly are the least likely to spend on things and the most likely to spend on services (starting with health care and personal care). What’s more, they receive their benefits from taxes on young people—who historically are the most likely to want to buy things.

BROADER IMPLICATIONS

Falling commodity prices are hammering developing countries. Major players in Latin America and Sub-Saharan Africa have entered a “tailspin.” If this decline is indeed the new normal, poor commodity-exporting countries will have to turn to human capital—like India and the Philippines, which are turning their fluency in English to open up new service opportunities for the working class.

U.S. retailers are updating their playbooks. Companies from Urban Outfitters to REI are turning their stores into “experiences” with fun diversions and top-notch customer service. Others, like Home Depot and Lowe’s, are expanding into new markets (home services, in this case). And e-tailers like eBay and Bonobos are going high-touch with new brick-and-mortar outlets.

The U.S. economy is encountering an imbalance between the buying of private things (which is weakening) and the backlog of demand for public things like infrastructure (which is growing). It was the G.I. Generation’s commitment to building a new public infrastructure in the 1930s, ‘40s, and early ‘50s, which enabled the booming “affluent society” in subsequent decades. America may be ready for a reboot.

TAKEAWAY

Manufacturers and retailers should prepare for the possibility that “goods” aren’t coming back anytime soon. Even when (and if) the industrial sector emerges from its long-term atrophy, the underlying framework of the “old economy” will look entirely different than what we see today.