Here's some additional context on the NKE/US Wholesale relationship.

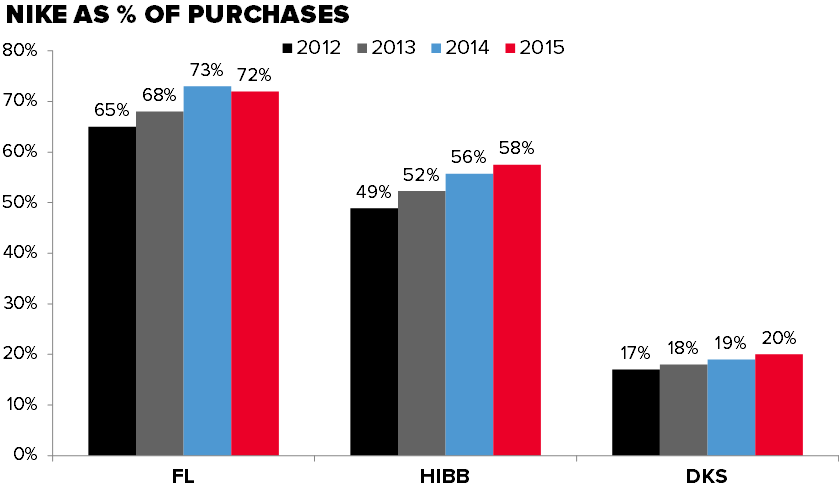

Three of the four biggest public Nike distributors have released 10ks to date, and the Nike growth trends (measured by Nike as a % of purchases) have shown signs of a top. The headline, of course, is the deceleration of Nike sales within Foot Locker from 73% to 72% in 2015 (for a more detailed overview of our thoughts see our full note: FL | Nike Found Its Ceiling). But, just as important is the measured Nike growth within HIBB, up 180bps YY vs. 340bps in both 2014 and 2013, and DKS up just 100bps despite a renewed emphasis on footwear and additional floor space allocated to apparel from underperforming categories like hunt and golf. Nothing that any of these retail partners sells drives more traffic and boosts ASP more than something with a Swoosh on it. Unfortunatley for Nike’s partners, incremental Swoosh growth is coming from Nike direct putting an end to the nine year tailwind experienced by the industry.

The critical point to understand when examining these relationships is how Nike accelerated penetration in its wholesale accounts over the past nine years while it built up its distribution network, on-premise manufacturing capability (i.e. you go to a Nike store, build a shoe and it is made before your eyes), and ability to ship single pairs efficiently to consumers rather than a containerload of 5,000 units to wholesalers. We’d argue that Nike funded growth in the DTC platform by way of outsized (and unsustainable) growth at its wholesalers.

So let’s fast-forward to the present… we’d argue that Nike is largely penetrated in virtually all its wholesale doors in the US. We’re seeing higher price points, which is great. But most of those higher-priced shoes are available only at nike.com or Nike’s ‘snkrs’ app. With those two taken in context, is it any surprise that Nike finally said in public that it will massively accelerate its e-commerce from $1bn to $7bn? Not at all. In fact we think that Nike is understating it’s e-comm growth potential over the next 5 years by as much as $4bn.

Perhaps most important in this discussion is that we are seeing a shifting distribution paradigm in NA (from traditional wholesale to Nike DTC) play out in every quarter that Nike reports. Here are the most notable highlights from the most recent Nike quarter…

1) Lower Lows at Wholesale, Higher Highs for DTC. NKE NA biz grew 13% during the 3Q16. The incremental $429mm in revenue was essential evenly split between wholesale and retail, with DTC growing 25% fueled by e-comm, and wholesale up 9% against the easiest comp in the past 5 years (3% wholesale growth in 3Q15). If we look at it on a 2yr basis, eliminating all of the quarterly noise, we’ve seen a meaningful bifurcation in the underlying growth trend – not over the past three quarters, but past three years.

2) Channel Growth Spread at New Peak. The growth spread (calculated by taking DTC growth minus Wholesale growth) accelerated to 16% in 3Q16. The chart itself paints a pretty clear picture on how Nike is turning the distribution paradigm on its head, but what we think is most important to point out is that we are seeing higher highs in the DTC growth rates as the business approaches $4bn in sales. Over the course of the next five years we expect Nike to blow away its $7bn e-commerce target with the majority of that growth coming in its home market. That means an incremental $5bn-$6bn in NA e-commerce off a base of ~$750mm today. That translates to a continued widening in the growth spread over the near and long term.

3) DTC Penetration is Accelerating – Off a Higher Base. DTC Penetration as a % of total sales accelerated meaningfully in the quarter on a TTM basis, up 75bps representing the largest growth rate we’ve ever seen sequentially at Nike NA. To add a little context, over the past five years NKE NA DTC has grown its penetration by 450bps. This one quarter amounted for nearly 20% of that growth. If we look at where Nike direct competes online, its at the top end of the distribution chain. Put another way it’s at the product level which drives ASP and traffic to the likes of Foot Locker, Finish Line, and Dick’s Sporting Goods. As Nike continues to push its DTC agenda, those dollars come directly from that tier of the market, while the mid-tier channel stays more or less isolated.