BEST IDEAS LIST ADJUSTMENTS / UPDATES

SBUX — Last week we elevated SBUX to our core Best Ideas list as a SHORT. We will be presenting our thesis in a live Black Book presentation tomorrow, April 5th at 11:00AM ET.

Our SBUX SHORT thesis is not an indication that Starbucks is a broken company or that they are in need of a major overhaul. The simple fact is that much of the tailwinds (unit growth, mobile order & pay, daypart expansion) supporting the company right now are already built into the current stock price. So we are left asking, what’s next?

Going forward the increased complexity of the store due to the amplified focus on food sales will hamper growth, and could potentially tarnish the premium brand equity that Starbucks currently possesses. Additionally, the competition in the morning day-part is getting stronger. While beverage sales remain strong, a significant part of future same-store sales is dependent on selling more food. Food is not a core competency of the company and the company’s product offering is less compelling than others in the space. Additionally, the more they broaden the menu to less healthier items the challenges the company faces will intensify.

CALL DETAILS

Toll Free:

Toll:

UK: 0

Confirmation Number: 13633080

Materials: CLICK HERE (materials to be provided approximately 1 hour before the call)

EAT — Last week we also elevated EAT from our SHORT bench to our Best Ideas list as a SHORT. We see EAT as a company in transition and believe that FY2017 could become a year where management makes some incremental investments in the Chili’s brand. While EAT is one of the strongest companies in the Casual Dining space, the Chili’s brand needs to return traffic trends to positive territory again. What is unclear is how the investment will unfold in FY2017, but we will learn more at the upcoming analyst meeting on June 9th in NYC.

As a result of these investments, we see the Street’s estimates for 2017 as aggressive. Currently, FY2017 Street consensus is for Brinker to post EPS of $3.95. We see FY2017 estimates coming in closer to $3.40-$3.45, flat with FY2016 or even lower.

In the intermediate term, EPS for 2H FY2016 are also aggressive. For 3Q16 and 4Q16 estimates are for $1.00 and $1.25, respectively. Our model has estimates closer to $0.95 and $1.10, respectively.

Currently, EAT EV/NTM EBITDA multiple is 7.3x, significantly below its three year average and the Casual Dining group of 8.4x. If we are right about the current trend in EPS, the discounted multiple might not be enough of a discount.

SONC — Lastly, we moved SONC from our SHORT bench to our LONG bench. Please see our brief note HERE. In the coming weeks we will lay out our more detailed LONG thesis.

RECENT NOTES

4/3/16 SONC | ADDING TO THE LONG BENCH

3/31/16 SHAK | SUPPLY CHAIN ISSUES IN THE 10-K

3/30/16 PLAY | THE LAST STAND

3/29/16 EAT | AGGRESSIVE ESTIMATES

3/24/16 PLAY | SHORT| EXPECT VOLATILITY

3/15/16 CMG | DELUSIONAL

3/10/16 KNAPP-TRACK FEBRUARY RESULTS/ISPOT AD ANALYSIS

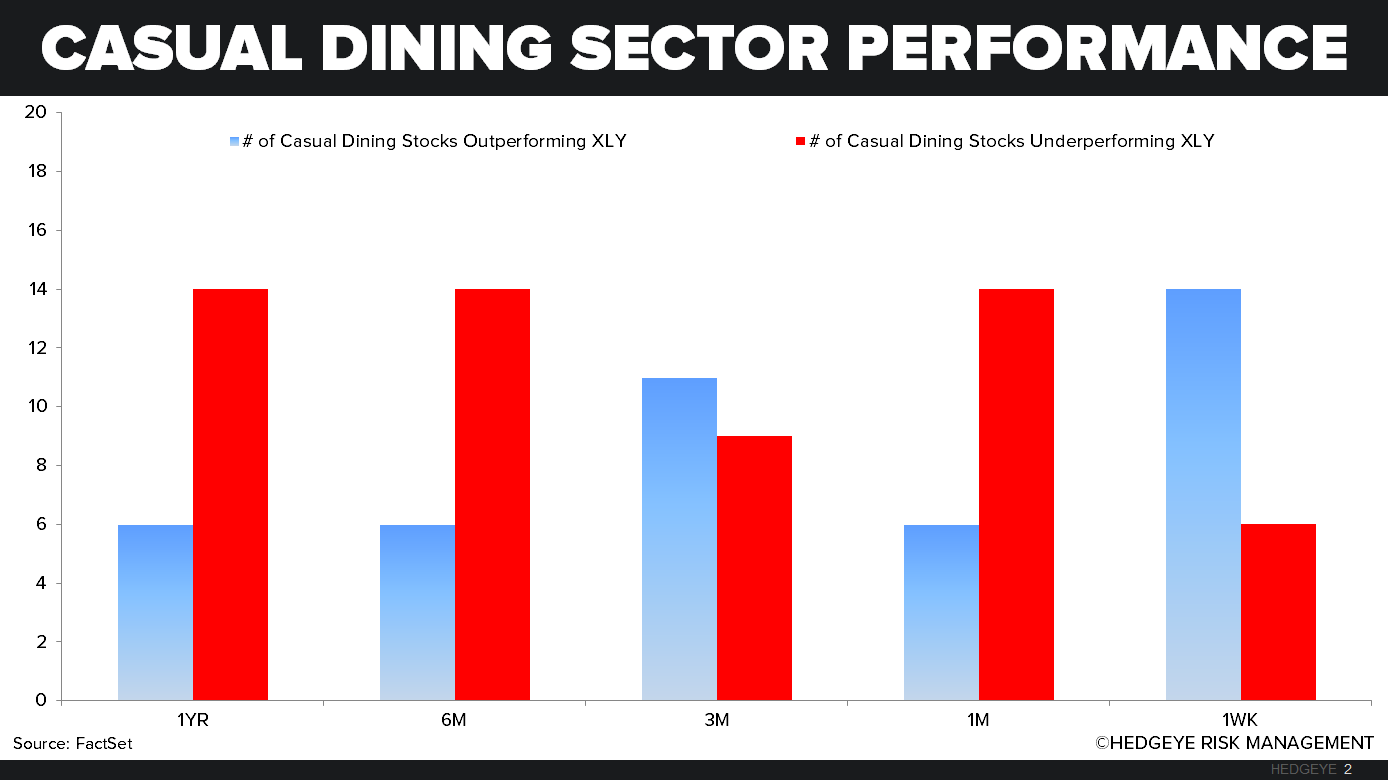

SECTOR PERFORMANCE

Casual Dining and Quick Service stocks that we follow outperformed the XLY last week. The XLY was up +2.4%, top performers on a relative basis from casual dining were KONA and TXRH posting performance of +4.8% and +4.5% respectively, while SHAK and SONC led the quick service group this week up +9.6% and +9.3%, respectively.

CASUAL DINING RESTAURANTS

QUICK SERVICE RESTAURANTS

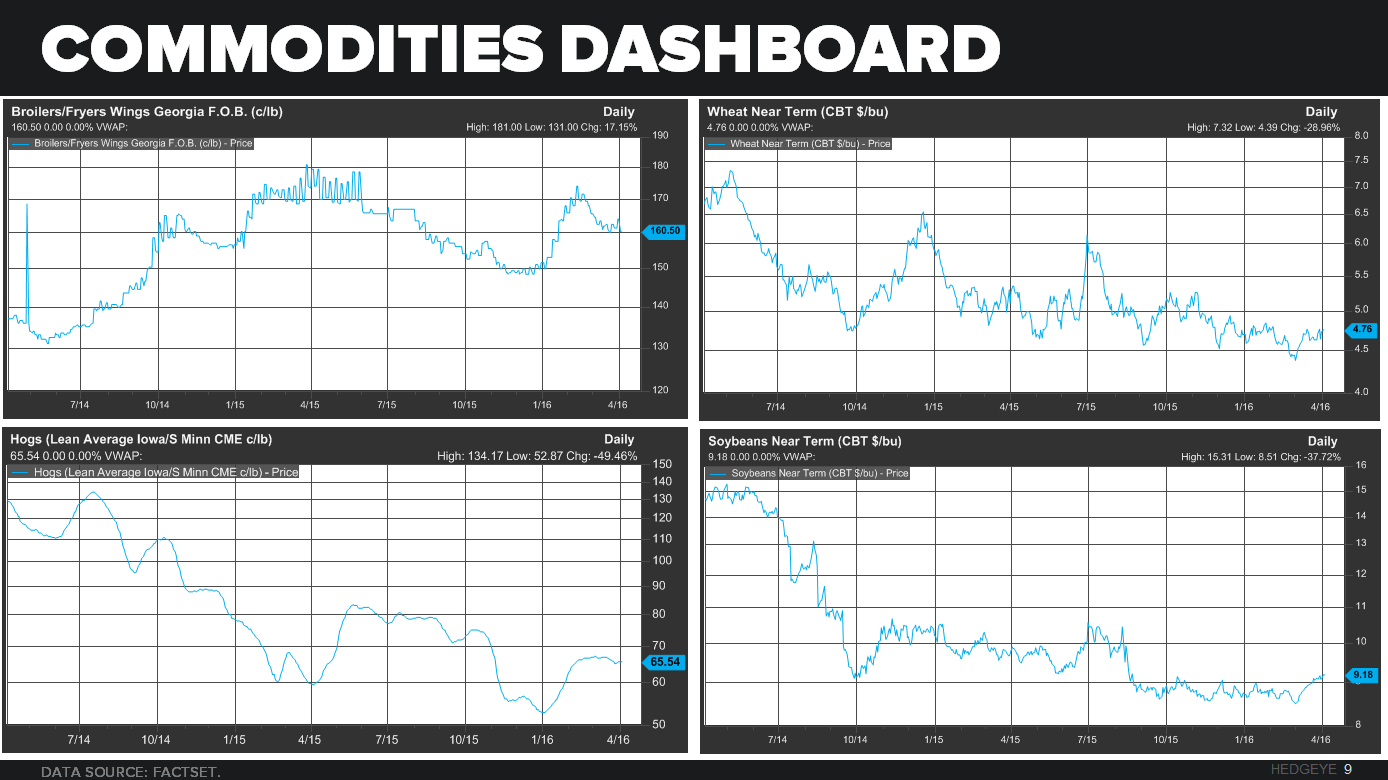

COMMODITIES

Please call or e-mail with any questions.

Howard Penney

Managing Director

Shayne Laidlaw

Analyst