The first chart below from our Macro team looks at the trend in Challenger job cut announcements. March job cuts ex-energy came in at 40.5k, which, while up 32% year over, is roughly flat with recent trends. Meanwhile, the energy patch also appears to be settling down, at least from a rate of change standpoint. The March energy patch job cut announcements of 7,747 were down from February's high watermark of 25,051, but remain broadly elevated.

Six of the eight states in our "Energy State" basket continue to show rising initial claims on a Y/Y basis - the exceptions being Texas, which is 2% lower Y/Y, and West Virginia (-21%). The sharpest increases in claims remain in North Dakota where claims are running +28% Y/Y.

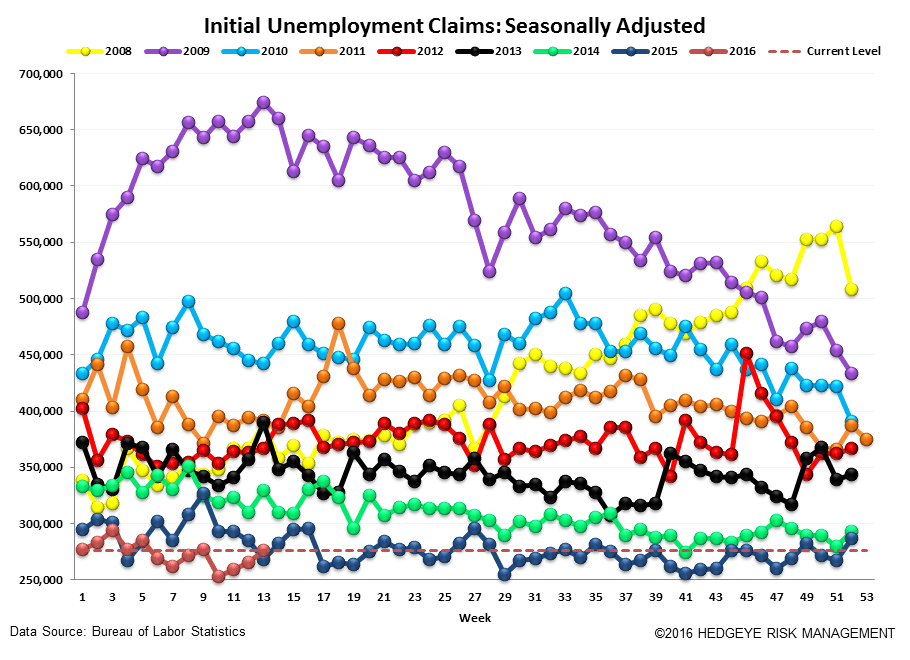

At the national level, claims rose 11k W/W, but remain low at 276k.

The Data

Initial jobless claims rose 11k to 276k from 265k WoW. The prior week's number was not revised. Meanwhile, the 4-week rolling average of seasonally-adjusted claims fell -0.25k WoW to 263.25k.

The 4-week rolling average of NSA claims, another way of evaluating the data, was -7.3% lower YoY, which is a sequential deterioration versus the previous week's YoY change of -10.9%

Yield Spreads

The 2-10 spread rose 5 basis points WoW to 107 bps. 1Q16TD, the 2-10 spread is averaging 108 bps, which is lower by -28 bps relative to 4Q15.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT