“These ideas are entirely imaginary, but if everyone shares them, we can all play the game.”

-Yuval Noah Harari

Imagine US GDP wasn’t tracking towards 1% with most of the cyclical/industrial sectors of the economy in #recession and corporate profits running down -11% year-over-year? Wow. Mind blowing. How would we play the “she’s dovish” game then?

Janet, with 2 trading days left until we send out our quarterly performance reports, we’re up, baby! Oh yeah – you go girl! Forget SP500 +0.5%, if we’re long the Long Bond (TLT +9% YTD), Utilities (XLU +14.3% YTD), and Gold (GLD +16.9% YTD), we’re really up!

Fascinating and brilliant, this complex market system is, isn’t it? As Harari astutely points out in Sapiens, “in order to establish such complex organizations it is necessary to convince many strangers to cooperate with one another…” (pg 118)

Back to the Global Macro Grind…

It’s almost like 1987 out there right now. Heck, if you asked a perma bull what the US stock market did that year – “it was flat.” After the worst 6-week start to the SP500 ever (which is still, in the non-imagined-world, a very long time), it’s back to “flat”, baby!

If only every portfolio manager’s performance was flat.

As one of the best performing long-only PM’s we work with pinged me yesterday, “bad is good and good is good, but it all sucks.” And since he’s not heartless about how a +1% US “growth” (heading toward 0% in Q2) economy ends for a lot of Americans, he’s right about the sucking part. Once we get through the last of this no-volume-month-end markup, I think bad is going to be bad again.

If you’re long something that is in line with both the Fed and Consensus Macro’s forecast of +3% US GDP growth (some of them used to be at 4%) like say, The Financials, yesterday really sucked too (XLF was only +0.18% on the day to -5.92% YTD).

But, if you were long the real Slower (GDP) and Lower (rates) for Longer stuff, like:

- Utilities (XLU) +1.5% on the day

- Gold (GLD) +3.0% on the day

Wow, did you have an awesome day. Those returns were 2-4 baggers versus the SPY, bros!

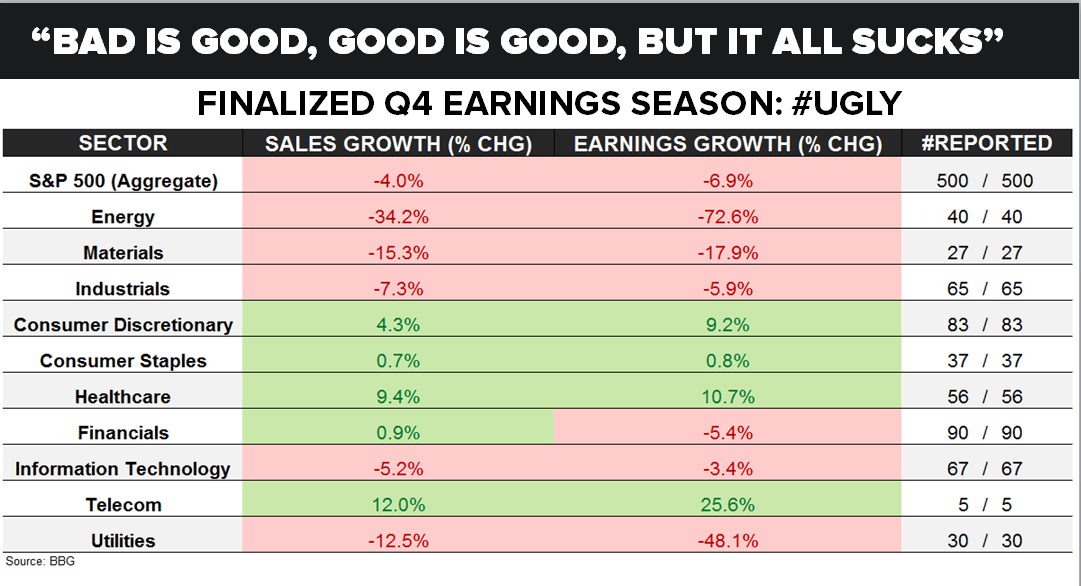

Shifting gears, not that profit or credit cycles matter when the Janet waives her “dovish” day-trader wand, but Earnings Season officially ended yesterday and here’s the summary:

- SP500 (500 of 500 companies have reported) aggregate SALES down -4.0%

- SP500 aggregate EPS down -6.9%

- SP500 Sectors saw 6 of 10 report NEGATIVE earnings growth

- “Ex-Energy” (i.e. 40 of the 500 companies), there are still 460 companies!

- Industrials (65 companies) and Financials (90) companies had EPS of -5.9% and -5.4%, respectively

To give Janet her “fair share” of air time, some of this weakness in the Financials (XLF) “reflected Financial developments since December”, like:

- The Fed hiking into a slow-down = December Policy Mistake

- The BOJ going for “negative yields” and ECB “buying corporate bonds”

- Then the Fed un-hiking the hikes, in their latest attempt to “ease” their SP500 dependent view

You know what all of this did for the credit cycle?

High Yield Spreads (up for 5 of the last 6 days btw) simply made another higher-low within a nasty cyclical breakout (well above the AUG-SEP level). And the rates move all but ensured that bank earnings are going to get hammered in the next Earnings Season.

Yep. Roll out the Old Wall’s “Ex-Financials, Buy Stocks On Rising Gas Prices” bull case for the US Economy in Q2!

Admittedly, we’re all trying hard to play this imaginary game of trying to find the next chart to chase (before the machines do). But it is getting harder to keep track of how the rules of the game go.

Following the Fed’s “transparent communication process” can really trip up a Fed follower:

- Two weeks ago, Yellen cuts via taking out the rate hikes = #Dovish

- Then, for all of last week, her Regional Talking Fed Heads talked up “April and June” rate hikes = #Hawkish

- Then she pivots incrementally dovish vs. her teammates’ hawkishness yesterday?

To be fair, I guess A) the SP500 was down last week (on their hawkishness!) and B) the Atlanta Fed GDP forecast dropped to 0.6% for Q1, so I guess she just had to start moving the goal posts a little faster.

Imagined or not, we all have to keep trying to play this game until the #BeliefSystem breaks down. Since it’s already breaking down in Japan and Europe, I think we’re closer to the beginning of the end of the game than we’ve ever been.

Our immediate-term Global Macro Risk Ranges are now:

UST 10yr Yield 1.79-1.91%

SPX 1

RUT 1066-1115

VIX 13.24-19.95

USD 94.54-96.50

YEN 111.02-113.88

Gold 1

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer