BREAKING... Believing the Fed's serially optimistic economic forecasts remains the biggest risk to investors.

Today, Fed head Janet Yellen said "caution" about further rate hikes was "especially warranted." While she was speaking, Treasury yields continued their downward descent.

Here's where we're at. The Fed continually dials back rate hike expectations and thereby jawboning Long Bond yields lower. The 10-year Treasury yield currently sits at 1.82%, 45 basis points below where it started at the beginning of the year.

Q: Who warned you?

A: Hedgeye

The dovish Fed commentary confirmed what we have long known. It was a mistake to raise rates in December and interest rates will have to stay #LowerForLonger to prop up an already flimsy economy. (Reminder: Wall Street's "top strategists" predicted the 10-year Treasury yield will end the year between 2.5% and 3.5%. We'll see about that.)

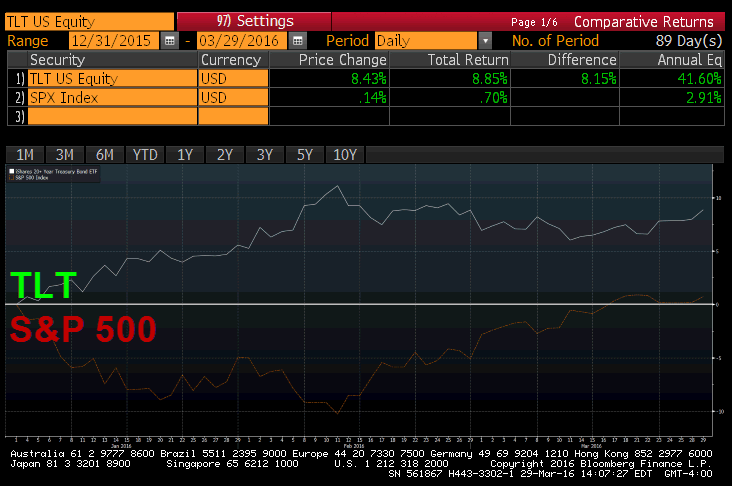

As Hedgeye CEO Keith McCullough likes to say, it still pays to be "the most bullish guy on Wall Street" on Long Bonds (TLT). Take a look at the performance of TLT year-to-date versus the S&P 500:

What else has worked this year? Other Hedgeye Long calls...

- Gold (GLD) up 16.6% year-to-date

- Utilities (XLU) up 13.4% year-to-date

(*Not exactly macro market expressions of confidence in the Fed's "all is good" mantra, huh?)

And if you think things get easier from here for Yellen & Co. don't hold your breath. As McCullough wrote in today's Early Look:

"We’re reiterating that the US economic and profit cycle won’t even have a chance of putting in a rate of change (cycle) bottom until Q2 which, candidly, won’t be reported until Q3."

Let's set aside for a second the fact that the Atlanta Fed's own Q1 2016 GDP forecast released yesterday just plunged 200 bps in the past month to a paltry 0.6%. It's our contention that as the developing corporate profit and industrial recession gets priced into the market (aka economic data continues to roll over), long-only equity investors can expect a lot more pain from here.