While the permabull marketing machine keeps churning, macro market internals are crumbling. Whether you're looking at performance of small cap stocks, declining bond yields, or the ongoing corporate profit recession, deteriorating economic data appears to be largely lost on Wall Street consensus.

Meanwhile, forecasts of our omnipotent Fed central planners remain disconnected from economic reality. As Hedgeye CEO Keith McCullough writes in a note to subscribers this morning:

"Treasury Yields stopped going down last week as Fed Heads jawboned about a rate hike (Dollar Up); immediate-term risk range on the UST 10YR is 1.84-1.98%; that’s a tight range – let’s see if they’re serious this time or just S&P 500 dependent (tightening into this Profit #Recession would be deflationary, again)."

More on the corporate profit recession reported friday...

It's getting pretty ugly. Corporate profits declined -10.5% year-over-year, slowing an additional -540 basis points versus Q3 when the data first went negative. We've been warning about declining corporate profits since January, with the release of our 1Q16 Quarterly Macro Themes.

Declining profits have been hammering stocks since the data peaked in Q2, McCullough writes.

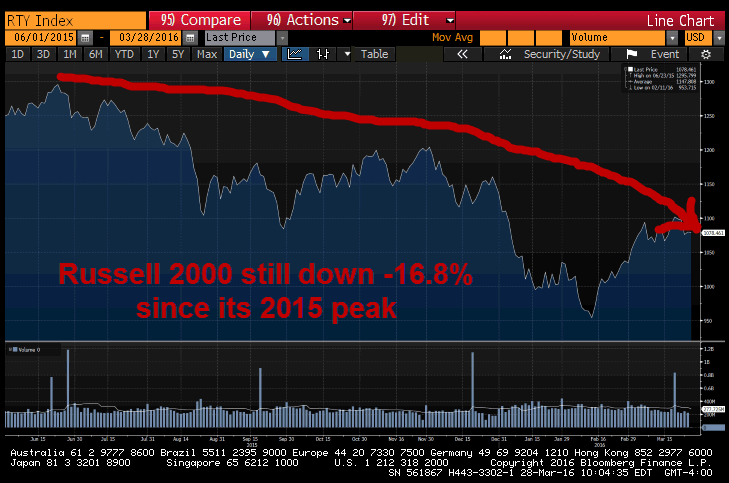

"The Russell 2000 lagged (again) last week, dropping -2.0% on the week (vs. -0.7% for the S&P 500); at -16.8% from its all-time high in July. The RUT is back to within 330 basis points of being in crash mode (> 20% decline from the July peak); Russell 2000 peaked when U.S. corporate profits peaked (Q2 of 2015)."

Where do we go from here?

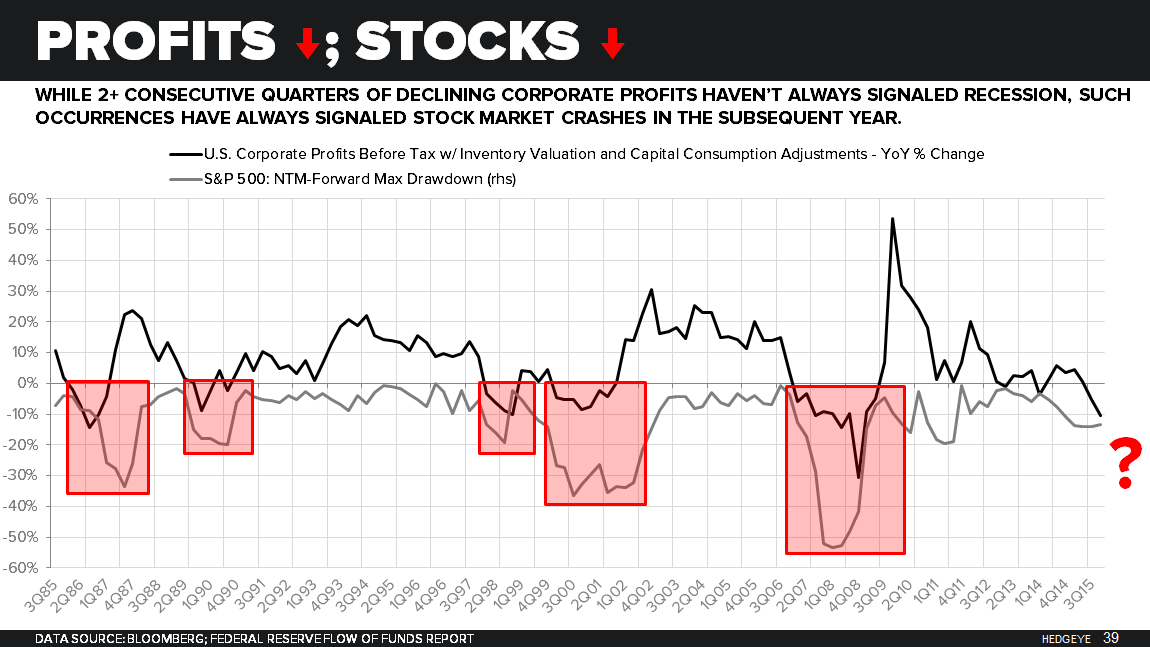

Here's another callout from our 73-page 1Q Macro Themes deck. In the past 30 years, two consecutive quarters of declining corporate profits always precedes a stock market crash: