Key Takeaway:

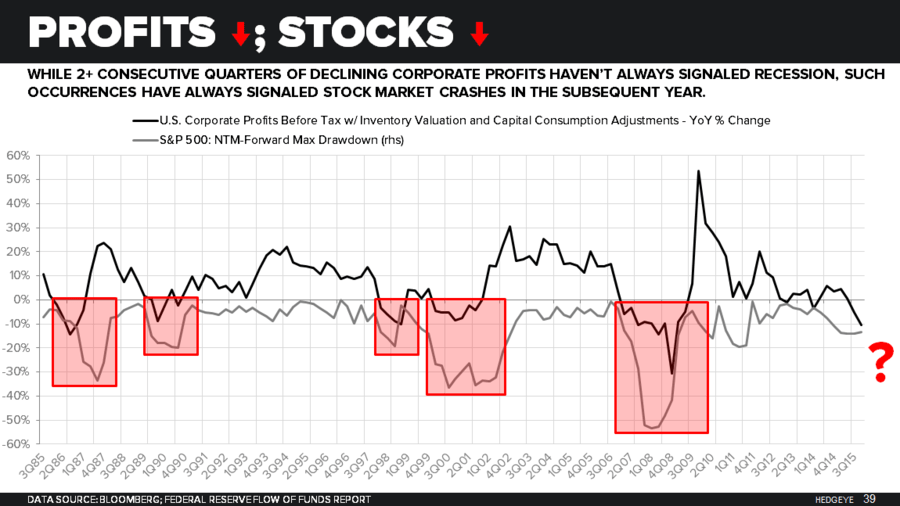

Our Macro team published an interesting note late last week showing that in 4Q15 corporate profits posted their worst growth (Y/Y) since 4Q08. While U.S. 4Q GDP was revised up to +1.4%, the corporate profit component showed a -10.5% Y/Y contraction. Moreover, that marks the second consecutive quarter in which corporate profit growth was down Y/Y. Meanwhile, global uncertainty rose on the heels of the Brussels terror attacks. CDS spreads widened globally at both the sovereign and bank level, and high yield rose +22 bps to 7.89%. The chart below illustrates that in the 30 years since 1985, two consecutive quarters of shrinking corporate profits have preceded a material stock market downturn over the next twelve months in all five occurrences.

Current Ideas:

Financial Risk Monitor Summary

• Short-term(WoW): Negative / 2 of 13 improved / 5 out of 13 worsened / 6 of 13 unchanged

• Intermediate-term(WoW): Positive / 8 of 13 improved / 3 out of 13 worsened / 2 of 13 unchanged

• Long-term(WoW): Negative / 1 of 13 improved / 4 out of 13 worsened / 8 of 13 unchanged

1. U.S. Financial CDS – Swaps widened for most domestic financial institutions as data showed the worst rate of Y/Y corporate profit contraction since 4Q08.

Widened the least/ tightened the most WoW: LNC, ACE, AGO

Widened the most WoW: MET, PRU, ALL

Tightened the most WoW: AIG, AXP, HIG

Widened the most MoM: JPM, RDN, MMC

2. European Financial CDS – Swaps mostly widened across European financials last week following the tragic terrorist attack in Brussels and poor corporate profit data out of the U.S.

3. Asian Financial CDS – Swaps mostly widened for Asian financials following the global reaction to the Brussels terrorist attack and poor U.S. corporate profits. China Development Bank Corp CDS widened the most, by 33 bps to 149. Meanwhile, Mizuho Corporate Bank in Japan tightened the most, by -14 bps to 97.

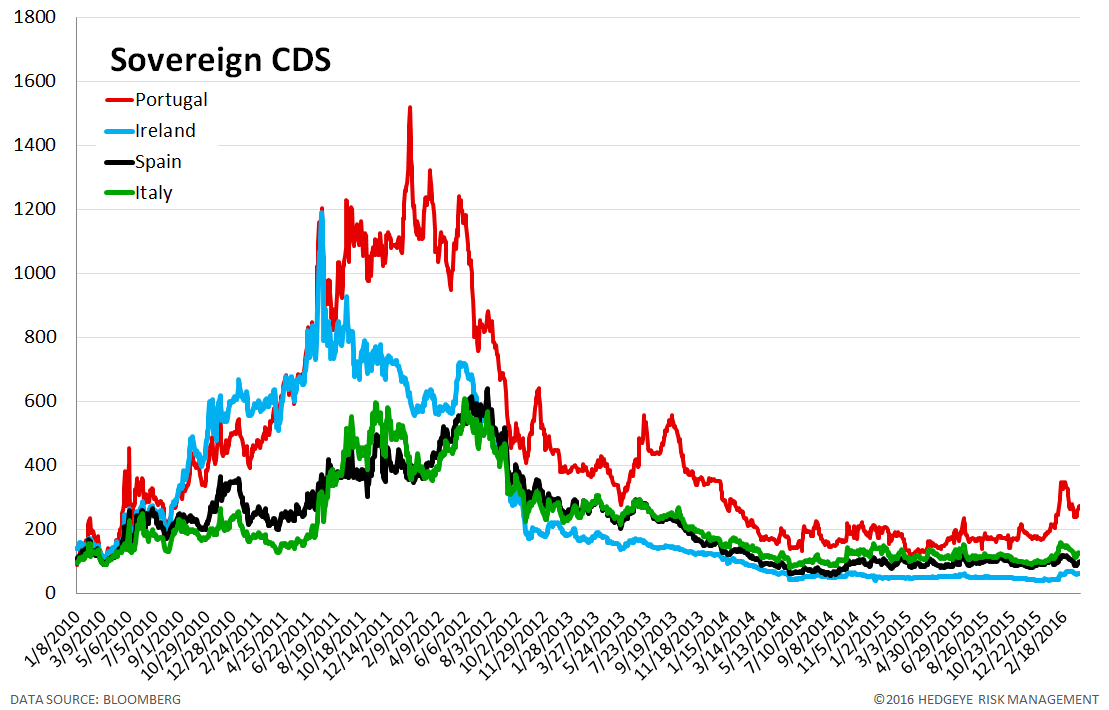

4. Sovereign CDS – Sovereign Swaps mostly widened over last week. Portuguese swaps widened the most, by 30 bps to 273.

5. Emerging Market Sovereign CDS – Emerging market swaps widened across the board last week. Brazilian sovereign swaps widened the most, by 29 bps to 395.

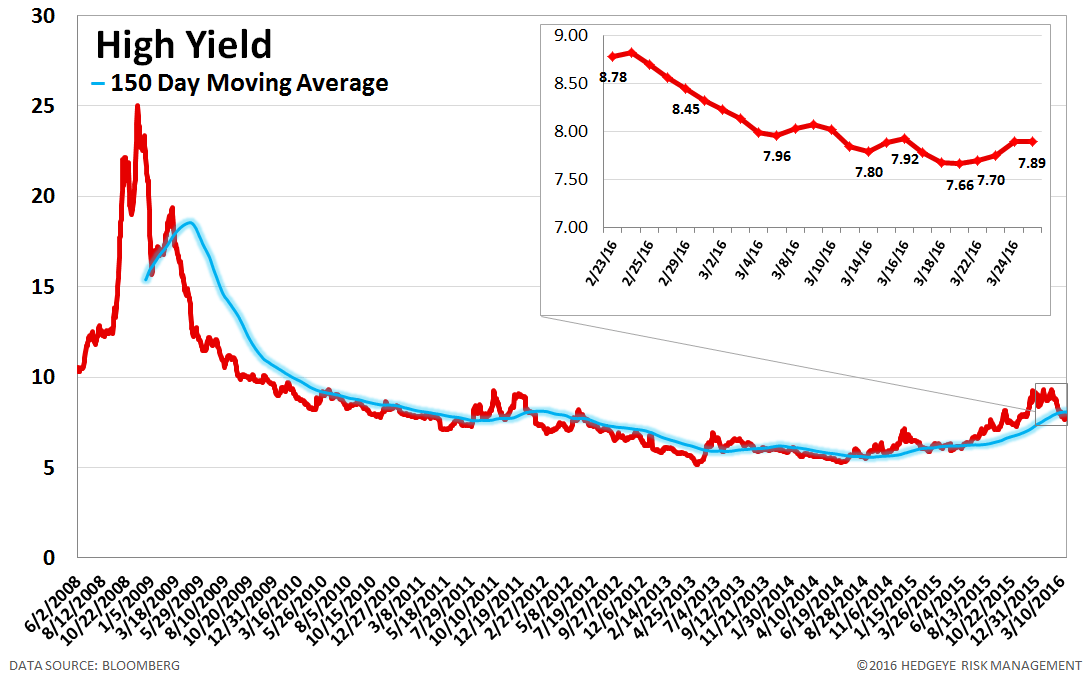

6. High Yield (YTM) Monitor – High Yield rates rose 22 bps last week, ending the week at 7.89% versus 7.67% the prior week.

7. Leveraged Loan Index Monitor – The Leveraged Loan Index rose 4.0 points last week, ending at 1852.

8. TED Spread Monitor – The TED spread rose 1 basis point last week, ending the week at 35 bps this week versus last week’s print of 33 bps.

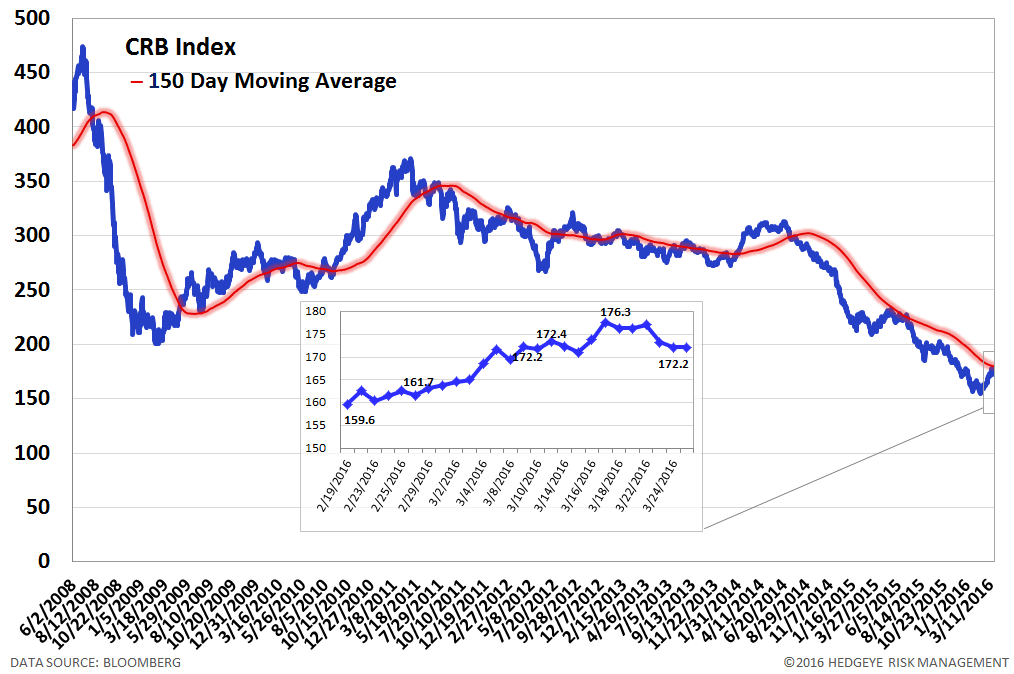

9. CRB Commodity Price Index – The CRB index fell -0.9%, ending the week at 172 versus 174 the prior week. As compared with the prior month, commodity prices have increased 6.5%. We generally regard changes in commodity prices on the margin as having meaningful consumption implications.

10. Euribor-OIS Spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps to 10 bps.

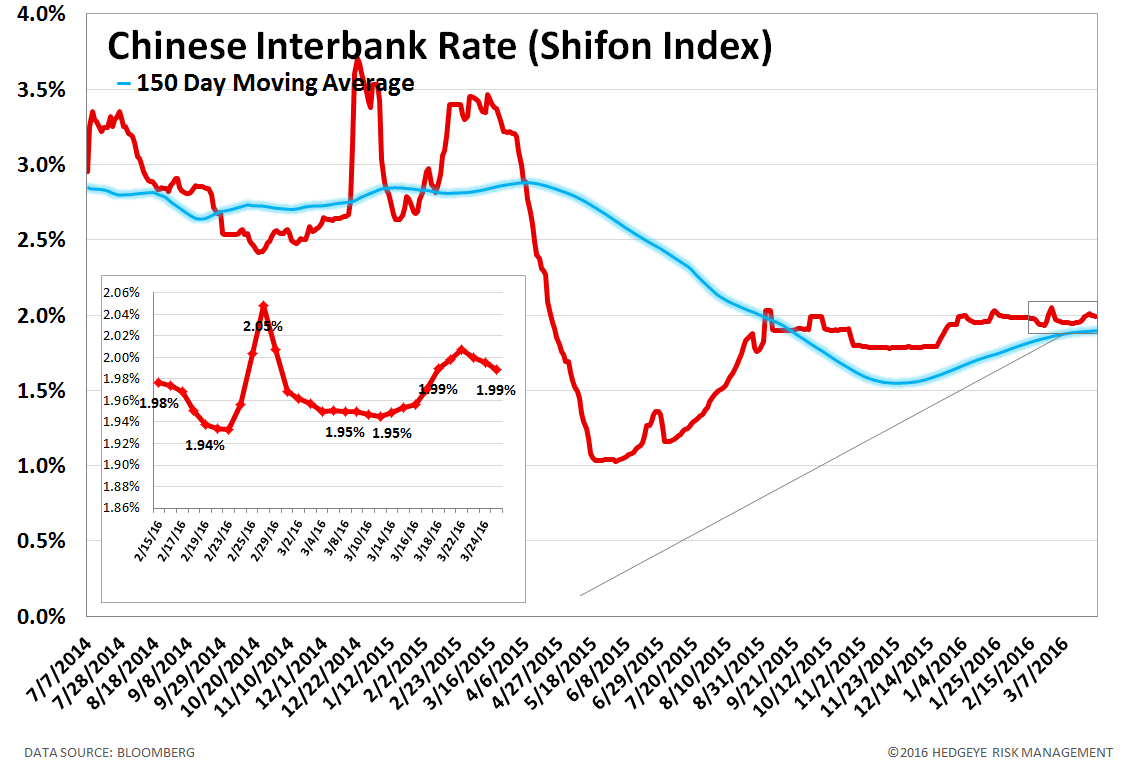

11. Chinese Interbank Rate (Shifon Index) – The Shifon Index was unchanged last week at 1.99%. The Shifon Index measures banks’ overnight lending rates to one another, a gauge of systemic stress in the Chinese banking system.

12. Chinese Steel – Steel prices in China rose 2.3% last week, or 54 yuan/ton, to 2419 yuan/ton. We use Chinese steel rebar prices to gauge Chinese construction activity and, by extension, the health of the Chinese economy.

13. 2-10 Spread – Last week the 2-10 spread tightened to 103 bps, -1 bps tighter than a week ago. We track the 2-10 spread as an indicator of bank margin pressure.

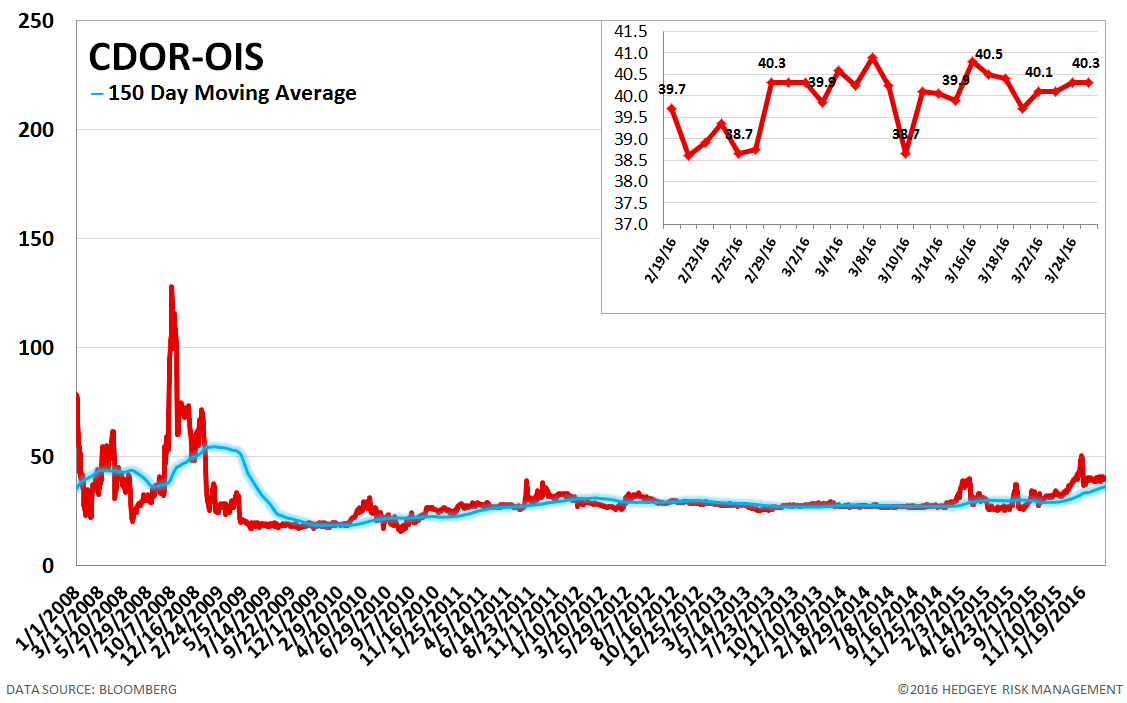

14. CDOR-OIS Spread – The CDOR-OIS spread is the Canadian equivalent of the Euribor-OIS spread. It is the difference between the Canadian interbank lending rate and overnight indexed swaps, and it measures bank counterparty risk in Canada. The CDOR-OIS spread was unchanged at 40 bps.

Joshua Steiner, CFA

Jonathan Casteleyn, CFA, CMT